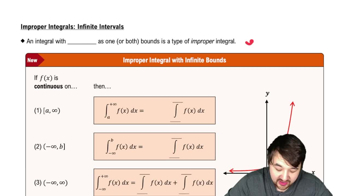

59. Perpetual Annuity Imagine that today you deposit \(B in a savings account that earns interest at a rate of *p*% per year compounded continuously (see Section 7.2). The goal is to draw an income of \)I per year from the account forever. The amount of money that must be deposited is: B = I × ∫(from 0 to ∞) e^(-rt) dt where r = p/100. Suppose you find an account that earns 12% interest annually, and you wish to have an income from the account of \$5000 per year. How much must you deposit today?

Verified step by step guidance

1

Identify the given variables: the interest rate is \(p = 12\%\), so the continuous compounding rate is \(r = \frac{p}{100} = \frac{12}{100} = 0.12\), and the desired income per year is \(I = 5000\) dollars.

Recall the formula for the amount to deposit today to receive a perpetual income \(I\) with continuous compounding interest rate \(r\):

\(B = I \times \int_0^{\infty} e^{-rt} \, dt\)

Evaluate the integral \(\int_0^{\infty} e^{-rt} \, dt\). This is an improper integral of an exponential decay function, which converges because \(r > 0\). The integral evaluates to:

\(\int_0^{\infty} e^{-rt} \, dt = \left[ -\frac{1}{r} e^{-rt} \right]_0^{\infty} = \frac{1}{r}\)

Substitute the value of the integral back into the formula for \(B\):

\(B = I \times \frac{1}{r} = \frac{I}{r}\)

Finally, plug in the known values \(I = 5000\) and \(r = 0.12\) into the formula to find the amount \(B\) that must be deposited today:

\(B = \frac{5000}{0.12}\)

Verified video answer for a similar problem:

This video solution was recommended by our tutors as helpful for the problem above

Video duration:

3m

Play a video:

0 Comments

Key Concepts

Here are the essential concepts you must grasp in order to answer the question correctly.

Continuous Compounding

Continuous compounding means that interest is added to the principal at every instant, modeled mathematically by exponential functions. The formula for the amount after time t is A = P * e^(rt), where r is the interest rate expressed as a decimal. This concept is essential to understand how the account balance grows over time in the problem.

Perpetual Annuity and Present Value of Infinite Cash Flows

A perpetual annuity provides a constant income indefinitely. Its present value is calculated by integrating the discounted cash flows over infinite time, using the formula B = I × ∫₀^∞ e^(-rt) dt. This integral represents the sum of all future payments discounted back to the present.

Improper Integral of an Exponential Decay Function

The integral ∫₀^∞ e^(-rt) dt is an improper integral representing the area under an exponential decay curve from zero to infinity. It converges to 1/r, which simplifies the calculation of the present value of the perpetual income stream. Understanding this integral is key to solving for the initial deposit B.

Verified step by step guidance

Verified step by step guidance

05:34

05:34