What are accrued expenses and how are they classified in accounting?

Accrued expenses are costs incurred for benefits received within a period that have not yet been paid, and they are classified as liabilities.

Why does the term 'accrued' in 'accrued expenses' indicate a liability rather than an expense?

The term 'accrued' indicates a liability because it refers to expenses that have been incurred but not yet paid, representing an obligation to pay in the future.

How does the matching principle relate to recording accrued expenses?

The matching principle requires that expenses be recorded in the same period as the revenues they help generate, so accrued expenses must be recorded at the period end even if not yet paid.

Provide a common example of an accrued expense in a business setting.

A common example is employee wages that have been earned but not yet paid by the end of the accounting period.

What is the adjusting journal entry to record \$300 in accrued wages at the end of a period?

Why is it important to record accrued expenses before the period ends?

Recording accrued expenses before the period ends ensures that all expenses incurred are matched with the revenues of the same period, providing accurate financial statements.

How does the use of 'prepaid' differ from 'accrued' in accounting terminology?

'Prepaid' indicates an asset, representing payment made in advance for future benefits, while 'accrued' indicates a liability for benefits already received but not yet paid.

What is the impact on the financial statements if accrued expenses are not recorded at period end?

If accrued expenses are not recorded, expenses will be understated and liabilities will be understated, leading to overstated net income and equity.

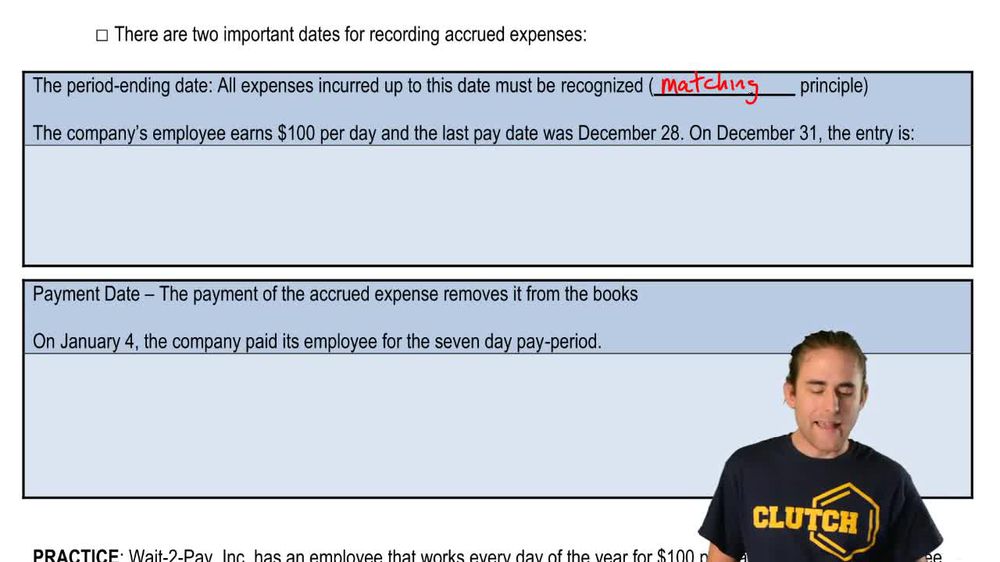

Describe the two important dates involved in recording accrued expenses.

The two important dates are the period ending date (when the expense is accrued) and the payment date (when the liability is settled).

What is the purpose of crediting 'accrued wage expense' when recording an accrued expense?

Crediting 'accrued wage expense' increases the liability, reflecting the company's obligation to pay for services already received.

How does the payment of an accrued expense affect the accounting equation?

Payment of an accrued expense decreases liabilities (by debiting the accrued expense) and decreases assets (by crediting cash).

What is the journal entry to remove an accrued expense liability when it is paid?

Debit the accrued expense liability account; credit cash.

Why might a company have both a debit to wage expense and a debit to accrued wage expense when paying wages?

A company debits wage expense for current period wages and debits accrued wage expense to remove the liability for prior period wages when making a combined payment.

How does the accrual of expenses ensure compliance with generally accepted accounting principles (GAAP)?

Accruing expenses ensures compliance with GAAP by adhering to the matching principle and providing an accurate representation of liabilities and expenses.

What is the effect on net income if accrued expenses are omitted from the adjusting entries?

Net income will be overstated because expenses are understated if accrued expenses are omitted.

Explain the difference between an expense and a liability in the context of accrued expenses.

An expense represents the cost of benefits received, while a liability (such as an accrued expense) represents an obligation to pay for those benefits in the future.

What account is credited when recording an accrued expense, and why?

An accrued expense liability account (such as Accrued Wage Expense) is credited to recognize the company's obligation to pay for incurred but unpaid expenses.

What is the journal entry to record an accrued expense at the end of an accounting period?

To record an accrued expense at the end of an accounting period, debit the relevant expense account (such as Wage Expense) and credit an accrued expense liability account (such as Accrued Wage Expense). This recognizes the expense incurred but not yet paid, adhering to the matching principle.

How do accrued expenses affect the balance sheet?

Accrued expenses appear as liabilities on the balance sheet because they represent obligations for expenses incurred but not yet paid by the end of the accounting period.

Back

Back

07:59

07:59