Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Journal Entries: Business Formation Example definitions

You can tap to flip the card.

Journal Entry

You can tap to flip the card.

👆

Journal Entry

A formal record in accounting that captures the details of a business transaction, specifying accounts affected and amounts debited or credited.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Journal Entries: Business Formation Example quiz #1

Journal Entries: Business Formation Example

10 Terms

Journal Entries: Business Formation Example

2. Transaction Analysis

10 problems

Topic

Trial Balance

2. Transaction Analysis

10 problems

Topic

2. Transaction Analysis

5 topics

15 problems

Chapter

Guided course

02:48

Journal Entries: Business Formation

2861

views

78

rank

Guided course

04:22

Journal Entries: Business Formation

2676

views

86

rank

Guided course

04:06

Journal Entries: Business Formation

3991

views

101

rank

Terms in this set (15)

Hide definitions

Journal Entry

A formal record in accounting that captures the details of a business transaction, specifying accounts affected and amounts debited or credited.

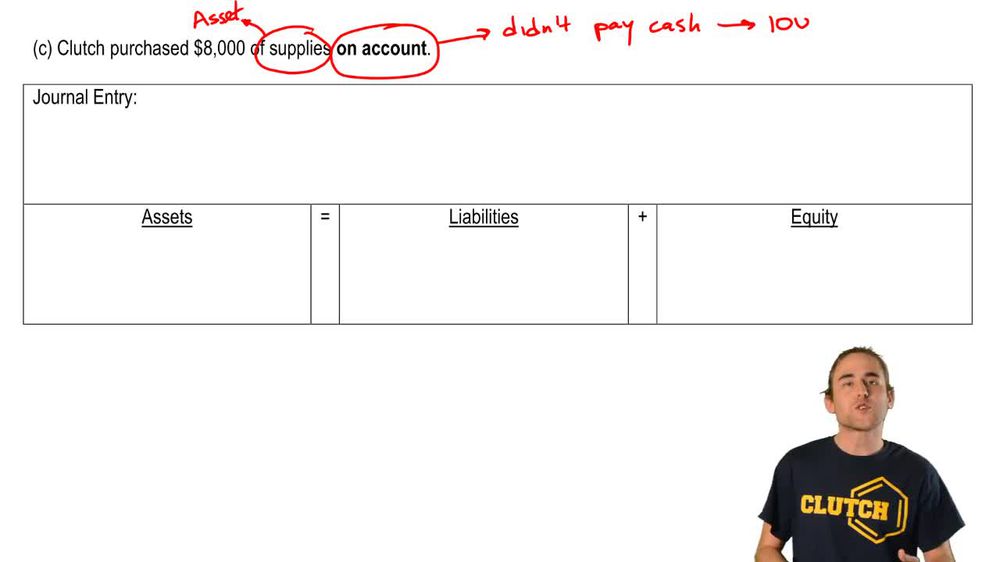

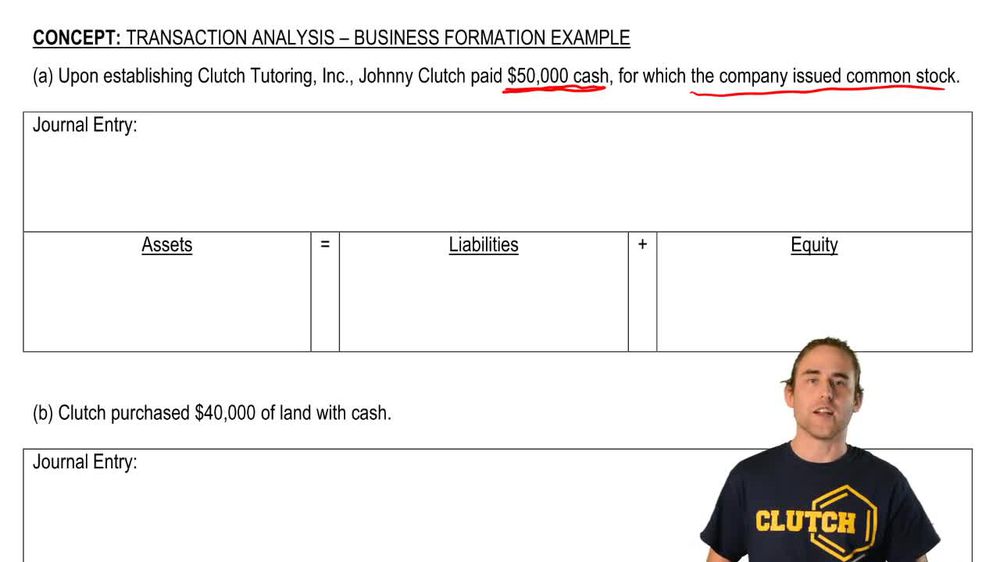

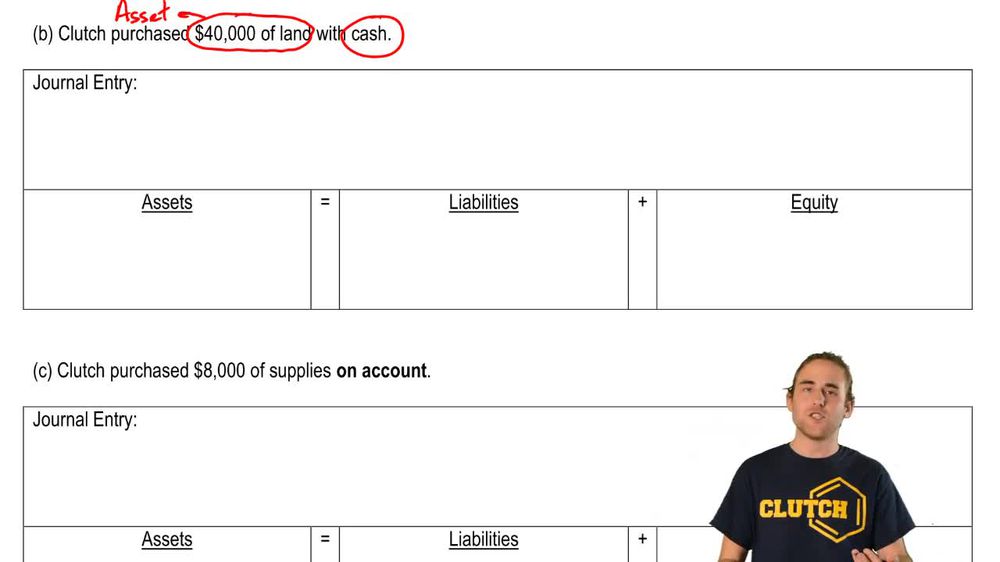

Business Formation

The initial process of legally creating a new company, often involving owner investment and issuance of ownership shares.

Common Stock

An equity account representing ownership in a corporation, typically issued to investors in exchange for capital.

Asset

A resource owned by a company, such as cash, that provides future economic benefit and is increased by debits.

Equity

The residual interest in the assets of a company after deducting liabilities, reflecting ownership value.

Debit

An accounting entry that increases asset or expense accounts and decreases liability or equity accounts.

Credit

An accounting entry that increases liability or equity accounts and decreases asset or expense accounts.

Accounting Equation

A foundational principle stating that assets equal the sum of liabilities and equity, ensuring balance in financial records.

Cash

A liquid asset account representing currency or funds available for immediate use by a business.

Owner Investment

Funds contributed by an individual or group to start or grow a business, typically exchanged for equity.

Liability

An obligation or debt owed by a company to outside parties, not affected in this business formation example.

Transaction

An economic event recorded in the accounting system, impacting at least two accounts to maintain balance.

Accounting Cycle

A series of steps in processing financial transactions, from initial entry to preparation of financial statements.

Financial Balance

The state achieved when total assets equal the sum of liabilities and equity, as required by the accounting equation.

Ownership

The legal right to possess a portion of a business, typically represented by shares or equity accounts.

BackBack

BackBack

02:48

02:48