What is the primary purpose of closing entries in accounting?

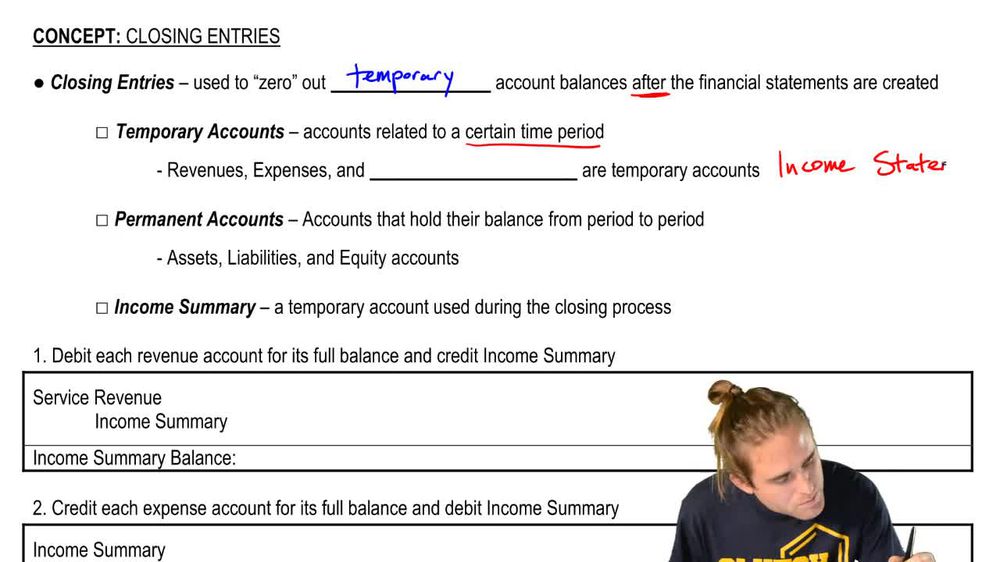

The primary purpose of closing entries is to zero out temporary account balances, such as revenues, expenses, and dividends, after financial statements are prepared, so these accounts are ready for the next accounting period.

Back

Back

02:37

02:37