What is the relationship between net income and retained earnings after closing entries?

Net income increases retained earnings, while a net loss decreases retained earnings after closing entries.

What is the effect of closing entries on the dividends account?

The dividends account is reset to zero after closing entries.

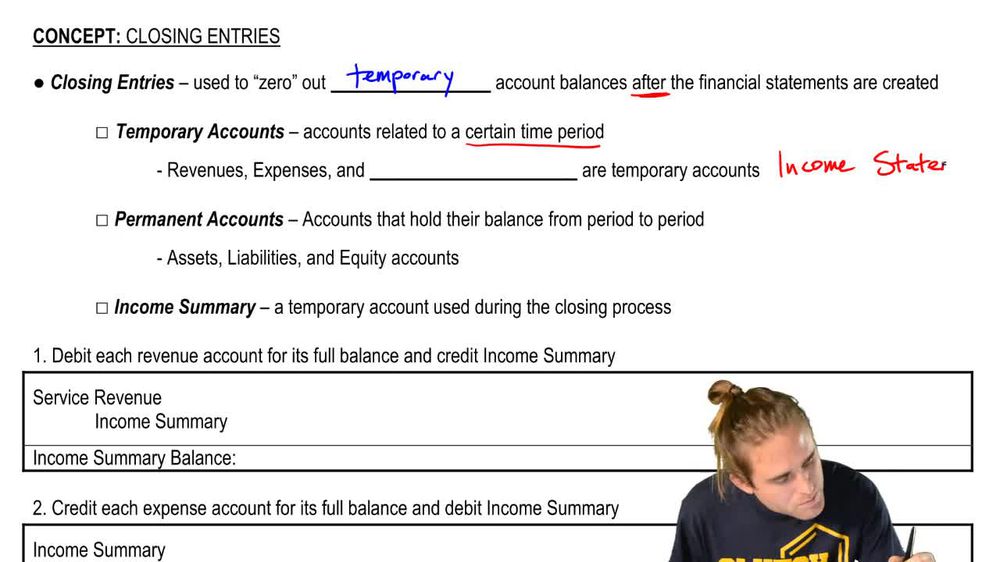

What is the effect of closing entries on the revenue and expense accounts?

Revenue and expense accounts are reset to zero after closing entries.

Why are closing entries made after financial statements are prepared?

Closing entries are made after financial statements to ensure that only current period activity is reported and to prepare accounts for the next period.

What is the purpose of the adjusted trial balance in the closing process?

The adjusted trial balance provides the updated balances of all accounts, which are used to prepare closing entries.

How does the closing process ensure accurate financial reporting?

The closing process ensures that only current period revenues, expenses, and dividends are reported, preventing carryover of prior period amounts.

What is the effect of closing entries on the balance sheet?

Closing entries do not affect the balances of permanent accounts on the balance sheet, except for retained earnings.

What is the effect of closing entries on the income statement?

Closing entries reset all income statement accounts (revenues and expenses) to zero for the new period.

What is the role of retained earnings in the closing process?

Retained earnings accumulates net income or loss and dividends from each period after closing entries are made.

How does the closing process differ for a company with a net loss versus net income?

With net income, income summary is closed with a debit and retained earnings is credited; with a net loss, income summary is closed with a credit and retained earnings is debited.

What is the impact of not closing the dividends account at period-end?

If the dividends account is not closed, its balance would incorrectly carry over to the next period, distorting equity.

What is the impact of not closing revenue and expense accounts at period-end?

If revenue and expense accounts are not closed, their balances would accumulate, distorting future period income statements.

What is the first step in the closing process?

The first step is to close all revenue accounts to the income summary account.

What is the second step in the closing process?

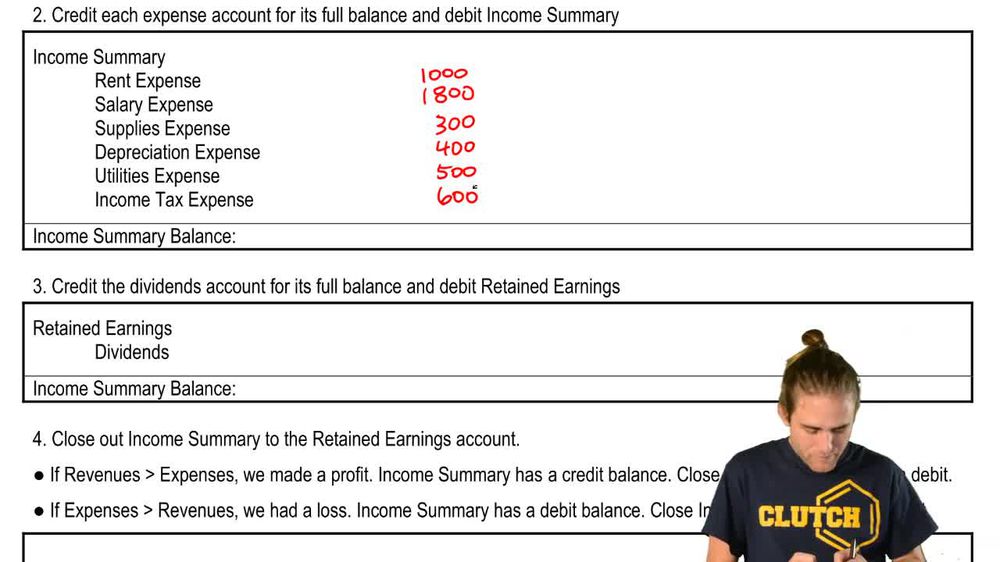

The second step is to close all expense accounts to the income summary account.

What is the third step in the closing process?

The third step is to close the income summary account to retained earnings.

What is the fourth step in the closing process?

The fourth step is to close the dividends account to retained earnings.

How does the closing process affect the beginning balances of temporary accounts in the next period?

The closing process resets temporary accounts to zero, so they start the next period with zero balances.

What is the effect of closing entries on the accounting equation?

Closing entries do not affect the accounting equation; they only reclassify balances within equity.

Why is it important to close the books at the end of each accounting period?

Closing the books ensures accurate reporting of financial performance for each period and prepares accounts for the next period.

What is the purpose of the post-closing trial balance?

The post-closing trial balance verifies that all temporary accounts have been closed and only permanent accounts have balances.

What is the normal balance of retained earnings and how is it affected by closing entries?

Retained earnings normally has a credit balance, which increases with net income and decreases with net loss or dividends after closing entries.

How are closing entries recorded in the general ledger?

Closing entries are recorded as journal entries in the general ledger, transferring balances from temporary to permanent accounts.

What is the effect of closing entries on the statement of retained earnings?

Closing entries update the statement of retained earnings to reflect net income or loss and dividends for the period.

What is the relationship between the income summary account and net income?

The balance in the income summary account after closing revenues and expenses represents net income or net loss for the period.

How does the closing process relate to the accounting cycle?

The closing process is the final step in the accounting cycle, preparing accounts for the next period.

What is the impact of closing entries on the equity section of the balance sheet?

Closing entries update retained earnings in the equity section to reflect the period's net income or loss and dividends.

What is the purpose of using the income summary account during the closing process?

The income summary account temporarily accumulates revenues and expenses to determine net income or loss before closing to retained earnings.

How does the closing process affect the financial statements for the next period?

The closing process ensures that only new period revenues, expenses, and dividends are reported in the next period's financial statements.

What is the effect of closing entries on the owner's equity in a corporation?

Closing entries update retained earnings, which is part of owner's equity, to reflect net income or loss and dividends.

How are closing entries different from adjusting entries?

Adjusting entries update account balances for accruals and deferrals, while closing entries reset temporary accounts to zero at period-end.

What is the impact of closing entries on the company's ability to track performance over time?

Closing entries ensure that each period's performance is tracked separately by resetting temporary accounts.

What is the effect of closing entries on the company's retained earnings balance?

Closing entries increase retained earnings by net income and decrease it by dividends and net loss.

Why is it important to close the income summary account at the end of the period?

Closing the income summary account ensures that net income or loss is transferred to retained earnings and the account is reset for the next period.

What is the result if the income summary account is not closed?

If the income summary account is not closed, it will incorrectly carry a balance into the next period, distorting equity.

How does the closing process help prevent errors in financial reporting?

The closing process prevents errors by ensuring that only current period activity is reported and prior period balances do not carry over.

What is the effect of closing entries on the company's net income for the next period?

Closing entries reset revenue and expense accounts, so net income for the next period is calculated only from new transactions.

How does the closing process relate to the preparation of the next period's financial statements?

The closing process ensures that temporary accounts start at zero, so the next period's financial statements reflect only current period activity.

What is the impact of closing entries on the company's financial position?

Closing entries do not change the company's financial position; they only reclassify balances within equity.

Why is it necessary to close the books even if a company has no dividends for the period?

It is necessary to close the books to reset revenue and expense accounts, even if there are no dividends.

What is the effect of closing entries on the company's ability to analyze trends over multiple periods?

Closing entries allow for accurate period-to-period comparisons by ensuring each period's results are reported separately.

Back

Back

02:37

02:37