A contingent liability is a potential obligation that may arise from an uncertain future event, such as a lawsuit, depending on the outcome of that event.

When should a company accrue a contingent liability on its balance sheet?

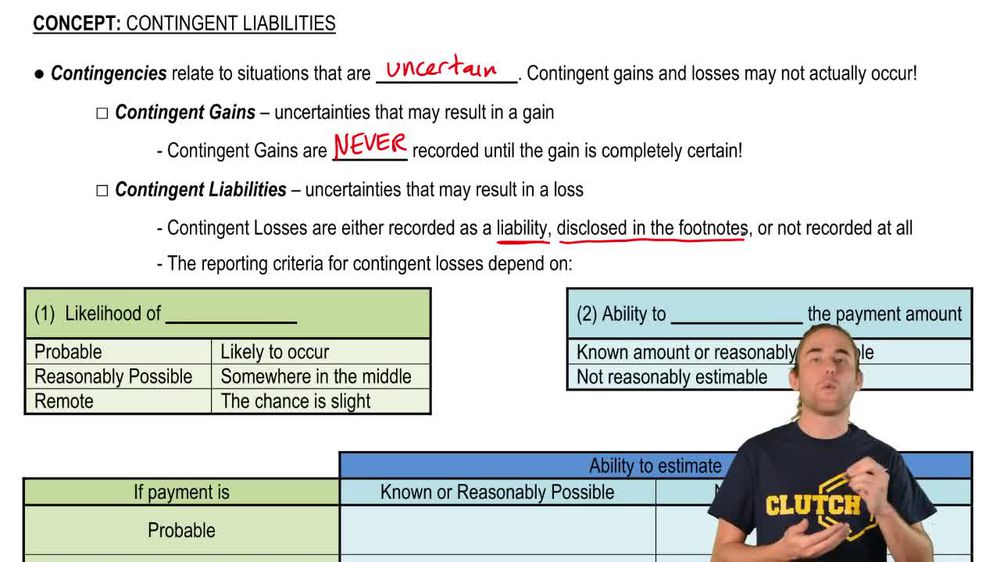

A company should accrue a contingent liability when it is probable that a loss will occur and the amount can be reasonably estimated.

How are contingent gains treated in accounting?

Contingent gains are not recorded until they are realized; they are only recognized when the gain is certain.

What are the three categories used to describe the likelihood of payment for a contingent liability?

The three categories are probable, reasonably possible, and remote.

What action is required if a contingent liability is probable but the amount cannot be reasonably estimated?

If a contingent liability is probable but the amount cannot be reasonably estimated, it should be disclosed in the footnotes of the financial statements.

What should a company do if a contingent liability is reasonably possible, regardless of whether the amount can be estimated?

If a contingent liability is reasonably possible, it should be disclosed in the footnotes, regardless of the ability to estimate the amount.

What is the appropriate accounting treatment if the likelihood of a contingent liability is remote?

If the likelihood is remote, no liability is accrued or disclosed; no action is required.

Why does accounting take a conservative approach to contingent gains and losses?

Accounting is conservative to avoid overstating assets or income; it only recognizes gains when realized but recognizes losses when they are probable and can be estimated.

What information is typically included in the footnotes regarding contingent liabilities?

The footnotes disclose the nature of the contingency, the estimated amount or range of loss if possible, and the likelihood of payment.

How does the ability to estimate the amount of a contingent liability affect its accounting treatment?

If the amount can be reasonably estimated and the loss is probable, the liability is accrued; if not, it is only disclosed in the footnotes.

What is the main difference between the accounting treatment of contingent gains and contingent liabilities?

Contingent gains are not recorded until realized, while contingent liabilities are accrued if probable and estimable, or disclosed if reasonably possible.

Back

Back

07:27

07:27