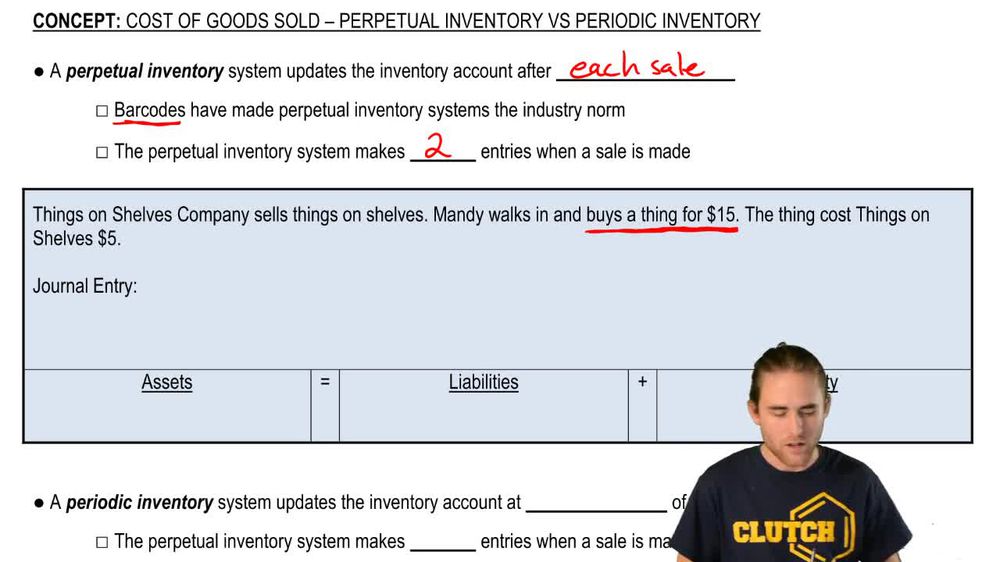

What is the main difference between the perpetual and periodic inventory systems in accounting for inventory?

The perpetual inventory system updates inventory and cost of goods sold (COGS) after each sale, while the periodic system updates inventory and calculates COGS only at the end of the accounting period.

How does the perpetual inventory system record a sale of inventory?

The perpetual system makes two entries: one debiting cash and crediting revenue for the sale amount, and another debiting COGS and crediting inventory for the cost of the item sold.

What journal entries are made in the periodic inventory system at the time of sale?

Only the revenue entry is made: debit cash and credit revenue for the sale amount. No entry is made for COGS or inventory at the time of sale.

How is cost of goods sold (COGS) calculated in the periodic inventory system?

COGS is calculated at the end of the period using the formula: Beginning Inventory + Purchases - Ending Inventory = COGS.

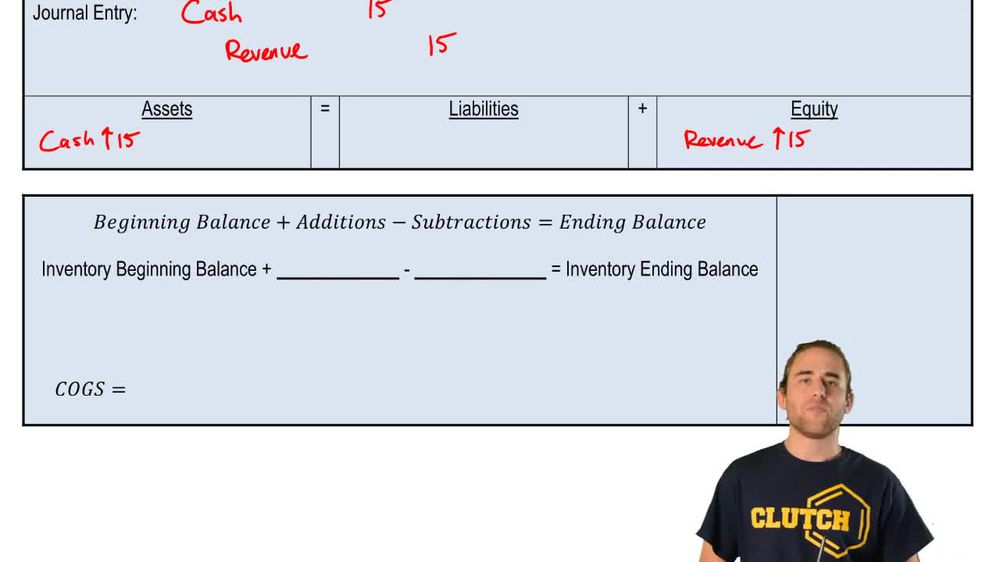

What is the effect on the accounting equation when a sale is made under the perpetual inventory system?

Assets increase by the cash received and decrease by the inventory cost; equity increases by the net of revenue minus COGS, keeping the equation balanced.

Why has the perpetual inventory system become more common in recent years?

The use of barcodes and technology allows for real-time tracking and updating of inventory after each sale.

In the perpetual system, what accounts are affected when inventory is sold for cash?

How does the periodic inventory system determine ending inventory?

Ending inventory is determined by physically counting the inventory at the end of the accounting period.

What is the T-account method used for in the periodic inventory system?

The T-account visually represents inventory activity, showing debits for beginning balance and purchases, credits for COGS, and the resulting ending balance.

What formula is used to solve for cost of goods sold in the periodic inventory system?

When is cost of goods sold recorded in the perpetual inventory system?

COGS is recorded immediately at the time of each sale.

When is cost of goods sold recorded in the periodic inventory system?

COGS is recorded only at the end of the accounting period after calculating it using inventory counts and purchase records.

What is the impact on equity when a sale is made under the perpetual inventory system?

Equity increases by the amount of revenue and decreases by the amount of COGS, resulting in a net increase equal to the gross profit.

How does the periodic inventory system handle purchases of inventory during the period?

Purchases are added to the inventory account, but the account is not adjusted for sales until the end of the period.

What is the main advantage of the perpetual inventory system over the periodic system?

The perpetual system provides real-time inventory and COGS information, allowing for better inventory management and financial reporting.

What is the main advantage of the periodic inventory system?

The periodic system is simpler and less costly to implement, as it does not require continuous tracking of inventory.

How does the perpetual inventory system help maintain the accounting equation?

By recording both the revenue and COGS entries at the time of sale, the perpetual system ensures that assets and equity are updated simultaneously, keeping the equation balanced.

What type of businesses are more likely to use the perpetual inventory system?

Businesses with high sales volume and advanced technology, such as retail stores with barcode scanners, are more likely to use the perpetual system.

What type of businesses might prefer the periodic inventory system?

Small businesses or those with low sales volume and limited resources may prefer the periodic system due to its simplicity.

How does the periodic inventory system ensure that the cost of goods sold is accurate?

By physically counting ending inventory and using records of beginning inventory and purchases, the periodic system accurately calculates COGS for the period.

What does the sum of beginning inventory and the cost of goods purchased represent in inventory accounting?

The sum of beginning inventory and the cost of goods purchased represents the total goods available for sale during the accounting period.

In the periodic inventory system, what does beginning inventory plus net purchases indicate?

Beginning inventory plus net purchases indicates the total goods available for sale before accounting for ending inventory.

What does the cost of goods sold (COGS) reported on the income statement represent?

The cost of goods sold on the income statement represents the expense incurred to purchase or produce the goods that were sold during the period.

How is cost of goods sold (COGS) calculated in the periodic inventory system?

COGS is calculated as: Beginning Inventory + Purchases (or Net Purchases) - Ending Inventory.

How does the perpetual method of accounting for inventory operate?

The perpetual inventory method updates the inventory account after each sale, recording both the revenue from the sale and the cost of goods sold immediately.

What items are typically included in the calculation of cost of goods sold (COGS)?

COGS typically includes the beginning inventory, purchases made during the period, and subtracts the ending inventory to determine the cost of goods sold.

Back

Back

03:41

03:41