Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Depreciation: Summary of Main Methods quiz #1

You can tap to flip the card.

What are the three main methods of calculating depreciation?

You can tap to flip the card.

👆

What are the three main methods of calculating depreciation?

The three main methods are straight line, double declining balance, and units of production.

Track progress

Control buttons has been changed to "navigation" mode.

1/39

Related flashcards

Related practice

Recommended videos

Depreciation: Summary of Main Methods definitions

Depreciation: Summary of Main Methods

15 Terms

Depreciation: Summary of Main Methods

8. Long Lived Assets

10 problems

Topic

8. Long Lived Assets

14 topics

15 problems

Chapter

Guided course

08:31

Depreciation: Summary of Main Methods

844

views

21

rank

Terms in this set (39)

Hide definitions

What are the three main methods of calculating depreciation?

The three main methods are straight line, double declining balance, and units of production.

What are the key variables needed to calculate depreciation?

The key variables are cost, useful life, and residual value.

Is depreciation considered a cash or non-cash expense?

Depreciation is a non-cash expense.

What does net book value represent in depreciation accounting?

Net book value is the asset's cost minus accumulated depreciation; it does not necessarily equal market value.

Do different depreciation methods result in the same total depreciation over an asset's life?

Yes, total depreciation over the asset's life is the same regardless of the method used.

How does the straight line method allocate depreciation expense?

The straight line method allocates an equal amount of depreciation expense each year.

How does the double declining balance method allocate depreciation expense?

The double declining balance method accelerates depreciation, resulting in higher expenses in the early years and lower in later years.

How does the units of production method allocate depreciation expense?

The units of production method bases depreciation expense on actual usage or output of the asset.

Why do most companies prefer the straight line method for depreciation?

Most companies prefer the straight line method because it is simple and easy to apply.

Why might a company choose an accelerated depreciation method for tax purposes?

Accelerated depreciation reduces taxable income in early years, resulting in lower taxes and providing an incentive to invest in fixed assets.

What is the IRS-approved accelerated depreciation method called?

The IRS-approved method is called the Modified Accelerated Cost Recovery System (MACRS).

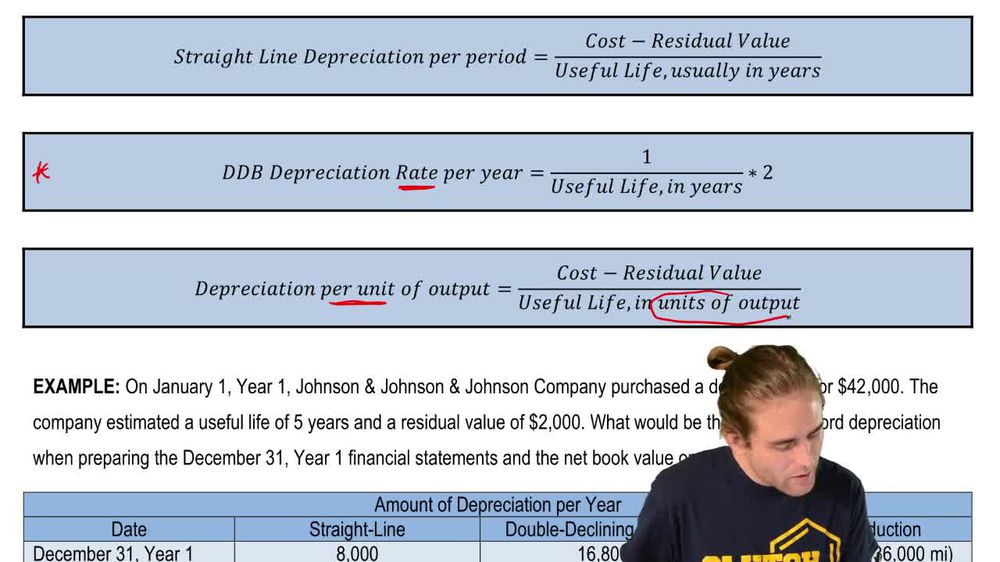

What is the formula for straight line depreciation?

Straight line depreciation = (Cost - Residual Value) / Useful Life.

What is the main difference between straight line and double declining balance methods?

Straight line spreads depreciation evenly, while double declining balance accelerates it, taking more in early years.

How is depreciation calculated under the units of production method?

Depreciation per unit = (Cost - Residual Value) / Total estimated units of output; annual expense = depreciation per unit × units produced that year.

What happens to the net book value of an asset over time as it is depreciated?

The net book value decreases each year as depreciation accumulates.

Does the net book value of an asset always match its market value?

No, net book value does not necessarily match market value.

Why are useful life and residual value considered estimates in depreciation calculations?

They are based on management's judgment and predictions about the asset's future use and value.

What is the main purpose of recording depreciation?

The main purpose is to allocate the cost of a fixed asset over its useful life, matching expense with revenue.

How does accelerated depreciation affect a company's taxable income in the early years of an asset's life?

It increases depreciation expense, reducing taxable income and taxes owed in the early years.

What is the depreciable base of an asset?

The depreciable base is the asset's cost minus its residual value.

How does the double declining balance method determine the depreciation rate?

The double declining balance rate is 2 × (1 / useful life).

What is the main advantage of using the units of production method?

It matches depreciation expense closely to the asset's actual usage.

What is the impact of depreciation on a company's cash flow?

Depreciation does not directly affect cash flow since it is a non-cash expense.

Why might the last year’s depreciation expense in double declining balance be a 'plug' amount?

To ensure the asset’s book value does not fall below its residual value.

What is the main economic reason the IRS allows accelerated depreciation methods?

To incentivize companies to invest in fixed assets and stimulate economic growth.

How does the choice of depreciation method affect financial statements?

It affects the timing of expense recognition and the net book value of assets.

What is the relationship between depreciation expense and net income?

Higher depreciation expense reduces net income.

Can a company change its depreciation method after an asset is in use?

Generally, a company must consistently use the chosen method, but changes can be made with proper justification and disclosure.

What is the main limitation of the straight line method?

It does not account for varying usage or wear and tear over time.

How does the units of production method differ from time-based methods?

It bases depreciation on actual output rather than time.

What is the effect of overestimating an asset’s useful life on annual depreciation expense?

Overestimating useful life lowers annual depreciation expense.

What is the effect of underestimating an asset’s residual value on annual depreciation expense?

Underestimating residual value increases annual depreciation expense.

Why is it important to match depreciation expense with revenue?

It ensures expenses are recognized in the same period as the revenues they help generate, following the matching principle.

What happens if an asset is used more than expected under the units of production method?

Depreciation expense will be higher in years with greater usage.

What is the main reason companies might avoid using accelerated depreciation for financial reporting?

Accelerated depreciation lowers reported net income in early years, which may not be desirable for financial statement users.

How does depreciation benefit companies from a tax perspective?

It reduces taxable income, thereby lowering the amount of taxes owed.

What are the key variables used to calculate depreciation for a fixed asset?

The key variables used to calculate depreciation are the asset's cost, its estimated useful life, and its estimated residual value.

Which depreciation method is most commonly used by businesses, and why?

The straight line depreciation method is most commonly used by businesses because it is simple and provides consistent depreciation expense each year.

What are the two types of physical depreciation that affect fixed assets?

The two types of physical depreciation are wear and tear from usage and deterioration over time.

BackBack

BackBack

08:31

08:31