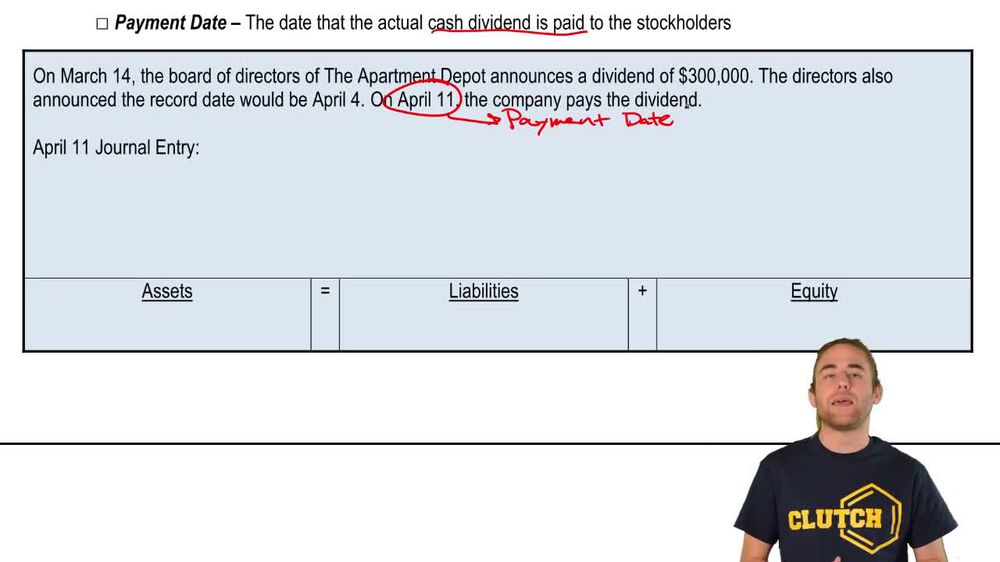

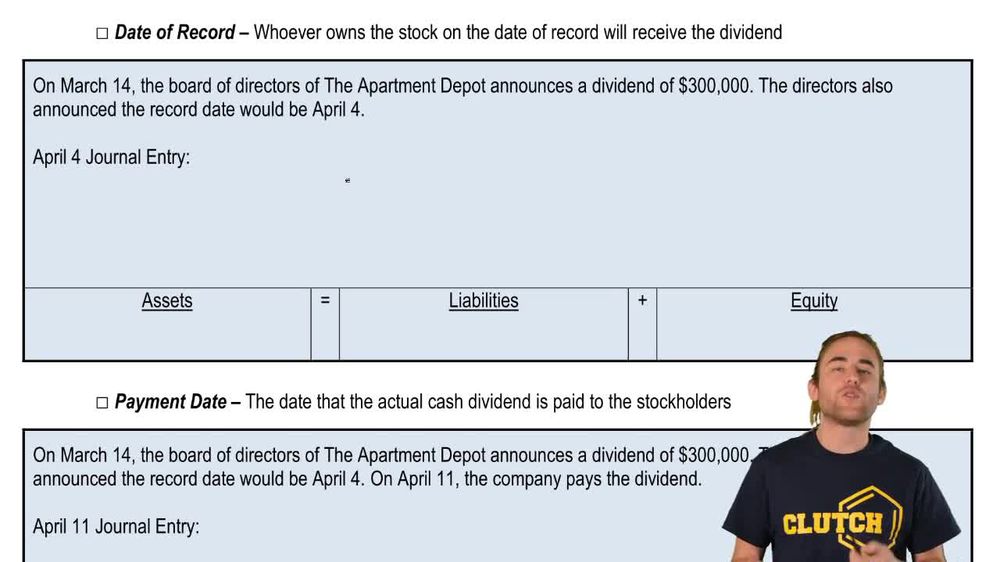

What are the three important dates associated with dividends, and what is the significance of each?

The three important dates are the declaration date (when the company announces and records a liability for the dividend), the record date (which determines who will receive the dividend but requires no journal entry), and the payment date (when the dividend is actually paid and the liability is settled).

Back

Back

05:30

05:30