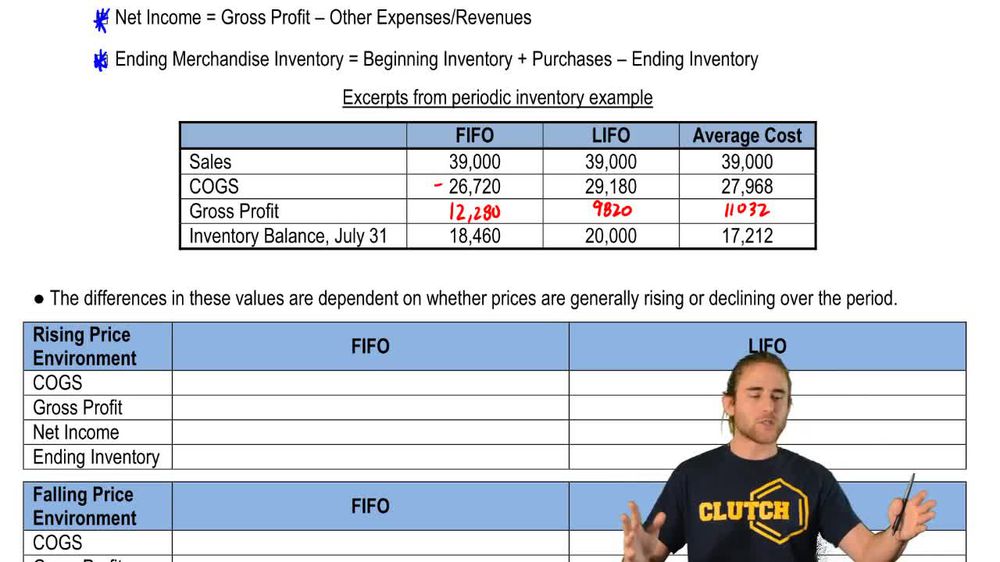

Inventory costing method where oldest units are assigned to cost of goods sold, often resulting in higher ending inventory during rising prices.

LIFO

Inventory costing method where most recent units are assigned to cost of goods sold, typically leading to lower ending inventory in rising price periods.

Average Cost

Inventory method that allocates cost based on the weighted average of all units available, producing results between FIFO and LIFO.

Cost of Goods Sold

Expense representing the cost assigned to inventory items sold during a period, directly affected by the chosen inventory costing method.

Gross Profit

Difference between sales revenue and cost of goods sold, reflecting profitability before operating expenses.

Net Income

Final profit figure after all expenses, including cost of goods sold and operating costs, have been deducted from total revenue.

Ending Inventory

Value of unsold inventory at the end of an accounting period, influenced by the inventory costing method and price trends.

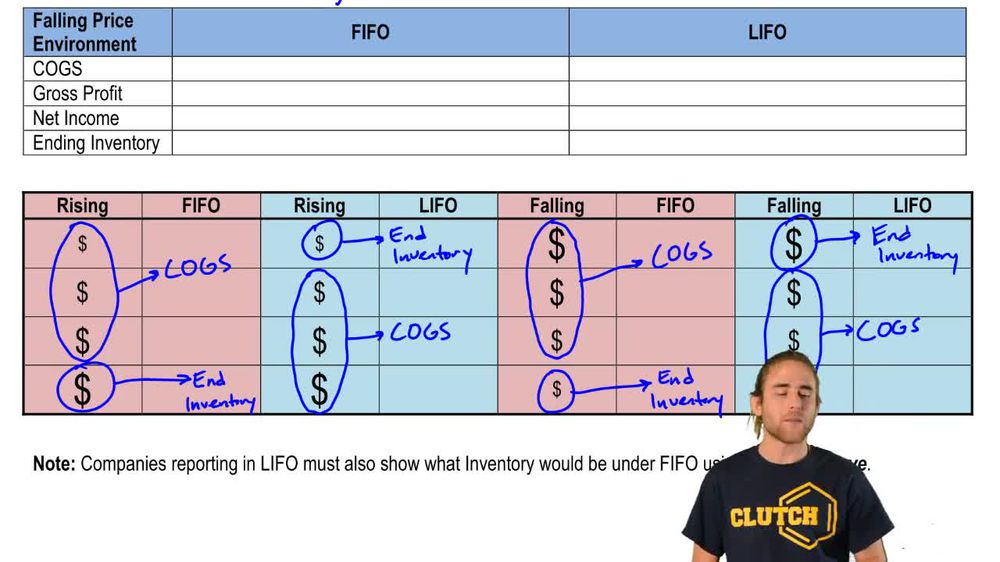

Rising Price Environment

Market condition where inventory purchase costs increase over time, impacting the financial statement effects of costing methods.

Falling Price Environment

Market scenario where inventory purchase costs decrease over time, reversing the typical effects seen in rising price periods.

Cost Flow Assumption

Accounting approach determining the order in which inventory costs are assigned to cost of goods sold and ending inventory.

LIFO Reserve

Disclosure showing the difference in inventory valuation between LIFO and FIFO, enhancing comparability across companies.

Financial Statements

Formal records summarizing a company's financial activities, including the effects of inventory costing choices.

Comparability

Quality enabling users to identify similarities and differences between companies, often improved by LIFO reserve disclosures.

Inventory Valuation

Process of assigning monetary value to inventory, directly influenced by the selected costing method.

Back

Back

07:32

07:32