How do FIFO, LIFO, and Average Cost inventory costing methods affect the calculation of Cost of Goods Sold (COGS)?

Each method assigns different costs to COGS: FIFO uses the oldest costs, LIFO uses the most recent costs, and Average Cost uses a weighted average, resulting in different COGS amounts.

In a period of rising prices, which inventory costing method results in the lowest Cost of Goods Sold (COGS)?

FIFO results in the lowest COGS during periods of rising prices.

How does the choice of inventory costing method impact gross profit in a rising price environment?

FIFO leads to higher gross profit, while LIFO results in lower gross profit when prices are rising.

What is the effect of using LIFO on net income during periods of increasing prices?

LIFO produces lower net income in periods of rising prices due to higher COGS.

How does ending inventory value differ between FIFO and LIFO in a rising price environment?

FIFO results in a higher ending inventory value, while LIFO results in a lower ending inventory value when prices are rising.

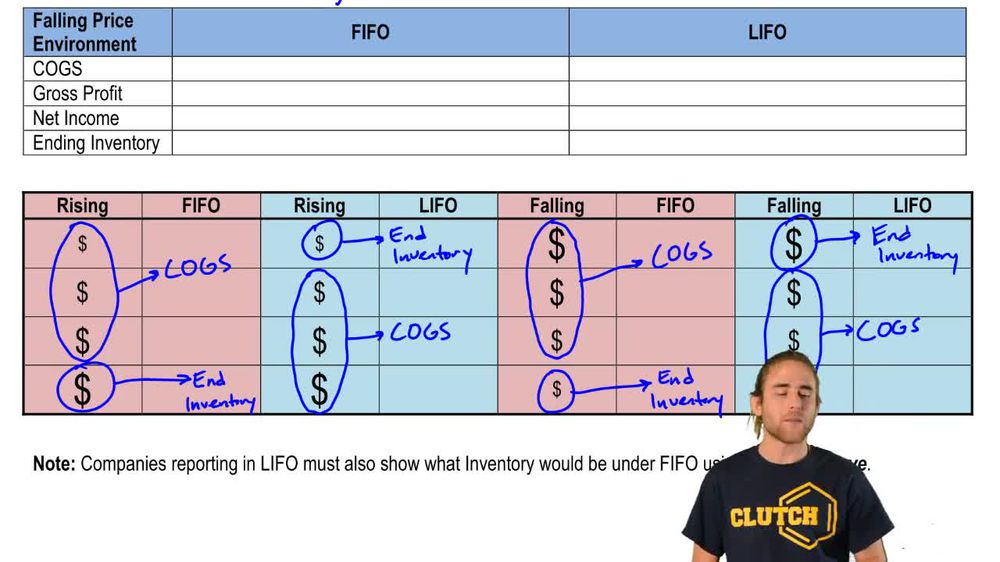

In a falling price environment, which inventory costing method results in the highest Cost of Goods Sold (COGS)?

FIFO results in the highest COGS during periods of falling prices.

How does LIFO affect gross profit in a falling price environment?

LIFO leads to higher gross profit in a falling price environment because it assigns lower costs to COGS.

What is the impact of FIFO on net income when prices are declining?

FIFO results in lower net income during periods of falling prices due to higher COGS.

How does the ending inventory value under LIFO compare to FIFO in a falling price environment?

LIFO results in a higher ending inventory value than FIFO when prices are falling.

Why do companies need to use inventory costing methods like FIFO, LIFO, or Average Cost?

Companies use these methods because inventory purchases often occur at different prices, requiring a systematic way to assign costs to COGS and ending inventory.

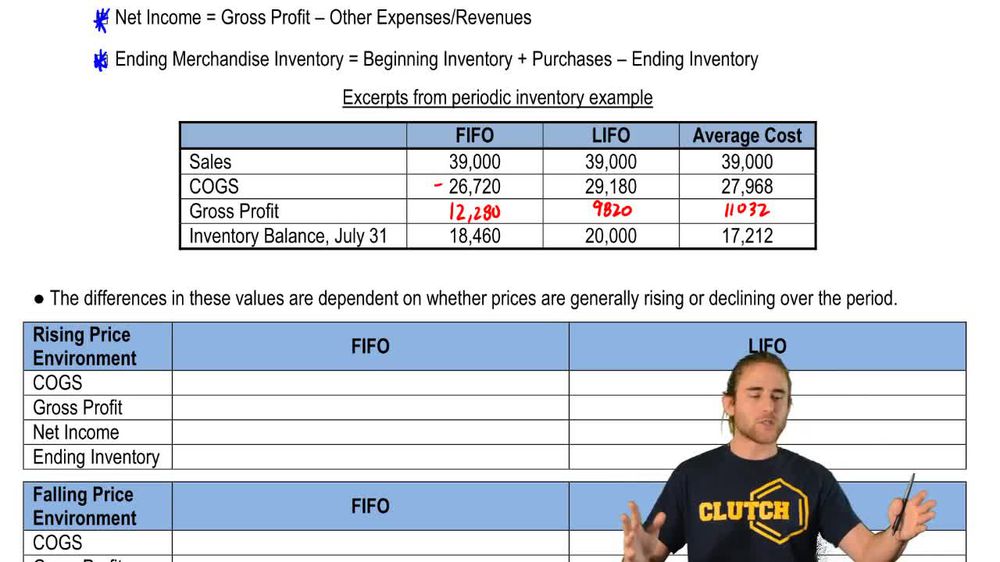

How does the Average Cost method typically compare to FIFO and LIFO in terms of financial statement effects?

The Average Cost method usually results in COGS, gross profit, net income, and ending inventory values that fall between those produced by FIFO and LIFO.

What is a LIFO reserve and why is it important for companies using LIFO?

A LIFO reserve is the difference between inventory reported under LIFO and FIFO; it is disclosed to enhance comparability across companies.

How does the choice between FIFO and LIFO affect comparability of financial statements between companies?

Different methods can lead to significant differences in reported COGS, gross profit, net income, and inventory, making direct comparison difficult unless adjustments like the LIFO reserve are disclosed.

Which inventory costing method would a company likely choose to minimize taxable income in a period of rising prices?

A company would likely choose LIFO to minimize taxable income during rising prices, as it results in higher COGS and lower net income.

How does the sales revenue amount change when different inventory costing methods are used?

Sales revenue remains the same regardless of the inventory costing method used; only COGS and related accounts are affected.

What is the relationship between COGS and gross profit when inventory costing methods are changed?

Gross profit is calculated as sales minus COGS, so any change in COGS due to the costing method directly affects gross profit.

Why might a company’s net income fluctuate significantly if it switches from FIFO to LIFO during periods of price volatility?

Switching methods changes which costs are assigned to COGS, causing net income to fluctuate with price changes.

In what scenario would FIFO result in the lowest ending inventory value?

FIFO results in the lowest ending inventory value during periods of falling prices.

Why is it important for companies using LIFO to disclose what their financials would look like under FIFO?

Disclosure of FIFO-based financials via the LIFO reserve improves comparability for investors and analysts across companies using different inventory methods.

How does the choice of inventory costing method (FIFO, LIFO, or Average Cost) impact key financial statement items such as Cost of Goods Sold, Gross Profit, Net Income, and Ending Inventory?

The selected inventory costing method affects Cost of Goods Sold (COGS), Gross Profit, Net Income, and Ending Inventory. In a rising price environment, FIFO results in lower COGS and higher Gross Profit, Net Income, and Ending Inventory compared to LIFO, which produces higher COGS and lower Gross Profit, Net Income, and Ending Inventory. In a falling price environment, FIFO leads to higher COGS and lower Gross Profit and Net Income, while LIFO results in lower COGS and higher Gross Profit and Net Income. The Average Cost method typically yields results between FIFO and LIFO. The choice of method can significantly affect financial reporting, especially when prices are volatile.

Back

Back

07:32

07:32