Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Fraud and the Fraud Triangle quiz #2

You can tap to flip the card.

What is the relationship between opportunity and internal controls?

You can tap to flip the card.

👆

What is the relationship between opportunity and internal controls?

Internal controls are designed to limit opportunities for employees to commit fraud.

Track progress

Control buttons has been changed to "navigation" mode.

1/40

Related flashcards

Related practice

Recommended videos

Fraud and the Fraud Triangle definitions

Fraud and the Fraud Triangle

14 Terms

Fraud and the Fraud Triangle quiz #1

Fraud and the Fraud Triangle

40 Terms

Fraud and the Fraud Triangle quiz #3

Fraud and the Fraud Triangle

40 Terms

Fraud and the Fraud Triangle

6. Internal Controls and Reporting Cash

10 problems

Topic

Sarbanes-Oxley Act

6. Internal Controls and Reporting Cash

10 problems

Topic

6. Internal Controls and Reporting Cash

8 topics

15 problems

Chapter

Guided course

04:54

Fraud and the Fraud Triangle

2011

views

83

rank

1

comments

Terms in this set (40)

Hide definitions

What is the relationship between opportunity and internal controls?

Internal controls are designed to limit opportunities for employees to commit fraud.

How can a company minimize rationalization among employees?

A company can minimize rationalization by fostering a fair and ethical work environment.

What is the purpose of having checks and balances in financial transactions?

Checks and balances help detect and prevent errors or fraud by requiring multiple approvals or reviews.

How does employee frustration contribute to fraud risk?

Employee frustration, such as feeling underpaid, can increase the likelihood of rationalizing and committing fraud.

What is the role of ethics in preventing fraud?

Promoting ethical behavior discourages rationalization and reduces the risk of fraud.

How can a company detect fake invoices?

A company can detect fake invoices by regularly reviewing and verifying all invoices and supporting documentation.

What is the impact of fraud on financial information?

Fraud can distort financial information, making it unreliable for decision-making.

How can companies support employees to reduce fraud incentives?

Companies can offer financial counseling, fair wages, and support programs to reduce financial pressures.

What is the benefit of having policies for asset safeguarding?

Policies for asset safeguarding help prevent unauthorized access and reduce the risk of theft or loss.

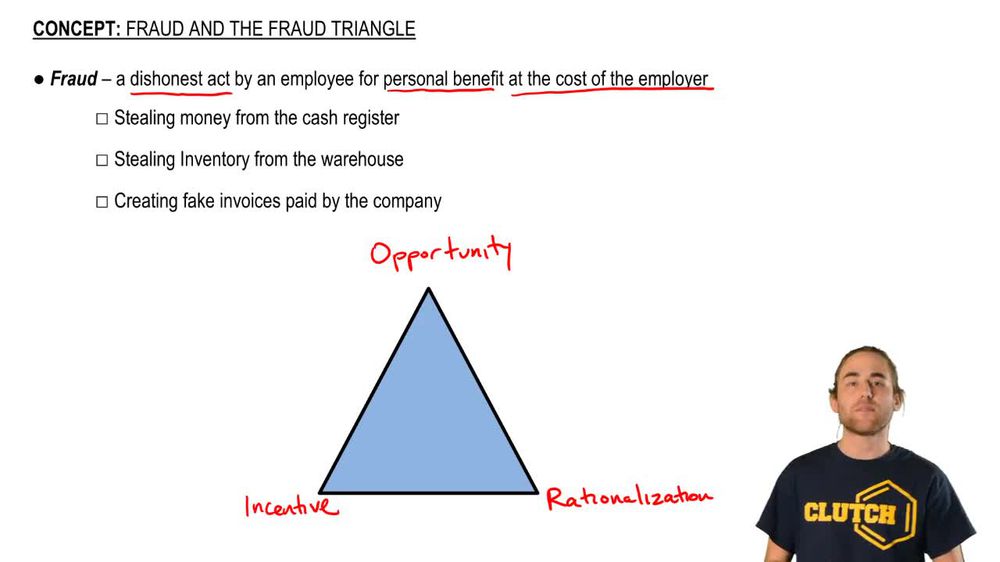

How does the fraud triangle help in designing internal controls?

Understanding the fraud triangle helps companies target controls to reduce opportunity, incentive, and rationalization.

What is the consequence of not addressing fraud risks?

Not addressing fraud risks can lead to financial losses, legal issues, and reputational damage.

How can companies encourage employees to report suspected fraud?

Companies can establish anonymous reporting systems and protect whistleblowers from retaliation.

What is the role of segregation of duties in internal controls?

Segregation of duties ensures that no single employee has control over all aspects of a transaction, reducing fraud risk.

How can regular reconciliation of accounts help prevent fraud?

Regular reconciliation helps identify discrepancies and detect unauthorized transactions early.

What is the importance of reliable financial information?

Reliable financial information is essential for accurate decision-making and maintaining stakeholder trust.

How does employee justification of fraud affect company culture?

If employees justify fraud, it can create a culture of dishonesty and increase overall fraud risk.

What is the relationship between financial pressure and fraud?

Financial pressure increases the incentive for employees to commit fraud.

How can companies monitor compliance with internal controls?

Companies can monitor compliance through regular audits and management reviews.

What is the effect of a lack of oversight on fraud risk?

A lack of oversight increases the opportunity for fraud by reducing the likelihood of detection.

How can companies create an ethical work environment?

Companies can create an ethical environment by promoting integrity, transparency, and accountability.

What is the purpose of requiring multiple approvals for transactions?

Multiple approvals help prevent unauthorized or fraudulent transactions by adding layers of review.

How does employee awareness of controls affect fraud risk?

When employees are aware of controls, they are less likely to attempt fraud due to increased risk of detection.

What is the impact of fraud on company reputation?

Fraud can damage a company's reputation, leading to loss of customer trust and business opportunities.

How can companies use technology to prevent fraud?

Companies can use technology to automate controls, monitor transactions, and detect unusual activities.

What is the significance of documenting internal control procedures?

Documenting procedures ensures consistency and provides a reference for training and audits.

How can management set the tone for ethical behavior?

Management can set the tone by modeling ethical behavior and enforcing policies consistently.

What is the role of audits in fraud prevention?

Audits help identify weaknesses in controls and detect fraudulent activities.

How can companies address rationalization to reduce fraud?

Companies can address rationalization by promoting fairness and open communication.

What is the benefit of surprise audits?

Surprise audits can catch fraudulent activities that regular audits might miss and deter employees from attempting fraud.

How does employee morale affect fraud risk?

Low morale can increase rationalization and the likelihood of fraud, while high morale can reduce it.

What is the importance of clear job responsibilities in fraud prevention?

Clear job responsibilities help prevent overlap and reduce opportunities for fraud.

How can companies ensure that internal controls are effective?

Companies can regularly review and update controls to address new risks and ensure effectiveness.

What is the relationship between company size and fraud risk?

Smaller companies may have higher fraud risk due to fewer resources for internal controls.

How can whistleblower policies help prevent fraud?

Whistleblower policies encourage employees to report fraud without fear of retaliation.

What is the impact of fraud on employee trust?

Fraud can erode trust among employees and between staff and management.

How can companies use background checks to reduce fraud risk?

Background checks can help identify individuals with a history of dishonest behavior before hiring.

What is the purpose of monitoring employee behavior?

Monitoring can help detect signs of fraud or unethical conduct early.

How does management override of controls contribute to fraud?

If management overrides controls, it increases the opportunity for fraud and undermines the control environment.

What is the benefit of rotating job assignments?

Rotating job assignments can prevent employees from developing schemes and help detect fraud.

How can companies address employee grievances to reduce fraud risk?

Addressing grievances can reduce rationalization and improve morale, lowering fraud risk.

BackBack

BackBack

04:54

04:54