Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

GAAP vs. IFRS: Statement of Cash Flows definitions

You can tap to flip the card.

GAAP

You can tap to flip the card.

👆

GAAP

U.S. accounting standards established by FASB, governing financial reporting and presentation, including the cash flow statement.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

GAAP vs. IFRS: Statement of Cash Flows quiz

GAAP vs. IFRS: Statement of Cash Flows

15 Terms

GAAP vs. IFRS: Statement of Cash Flows

15. GAAP vs IFRS

10 problems

Topic

GAAP vs. IFRS: Analysis and Income Statement Presentation

15. GAAP vs IFRS

10 problems

Topic

15. GAAP vs IFRS

13 topics

13 problems

Chapter

Guided course

05:02

GAAP vs. IFRS: Statement of Cash Flows

501

views

6

rank

Terms in this set (15)

Hide definitions

GAAP

U.S. accounting standards established by FASB, governing financial reporting and presentation, including the cash flow statement.

IFRS

International accounting standards set by IASB, providing global guidelines for financial statements, including cash flow reporting.

FASB

U.S. organization responsible for developing and updating generally accepted accounting principles.

IASB

International body that creates and maintains the International Financial Reporting Standards.

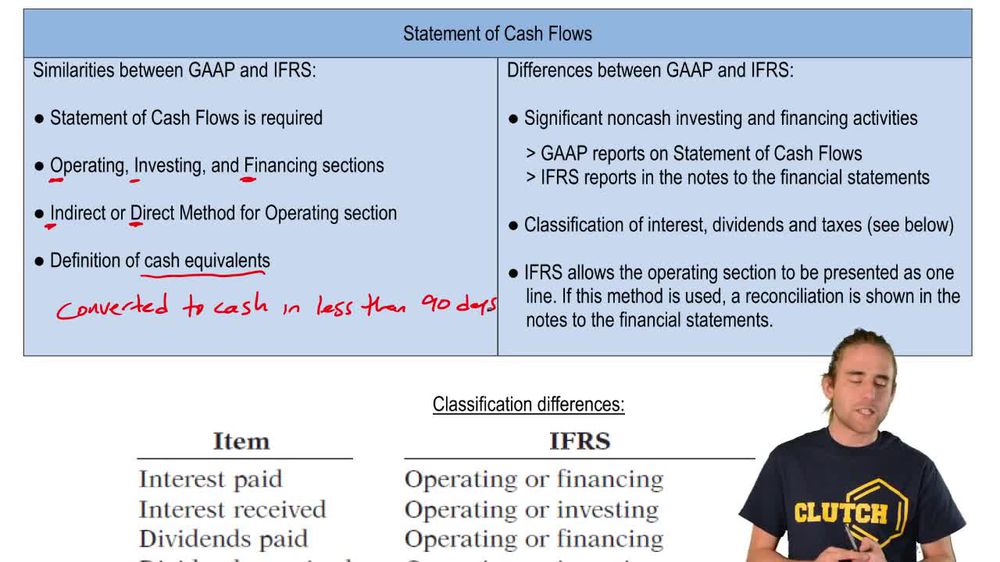

Statement of Cash Flows

Financial report dividing cash movements into operating, investing, and financing activities for a specific period.

Operating Activities

Section of the cash flow statement reflecting cash generated or used by core business operations.

Investing Activities

Cash flow statement section showing cash used for or received from buying and selling long-term assets.

Financing Activities

Part of the cash flow statement detailing cash flows from transactions with owners and creditors.

Direct Method

Approach to presenting operating cash flows by listing specific cash receipts and payments.

Indirect Method

Operating section format starting with net income and adjusting for non-cash items and changes in working capital.

Cash Equivalents

Highly liquid investments readily convertible to cash within 90 days, considered nearly as liquid as cash.

Non-cash Investing and Financing Activities

Significant transactions, such as exchanging stock for assets, that do not involve actual cash movement.

Notes to the Financial Statements

Supplementary disclosures providing details and explanations for items in the main financial statements.

Dividends Paid

Distributions to shareholders, classified as financing activities under GAAP and with flexible classification under IFRS.

Interest Paid

Outflows related to borrowing costs, typically classified as operating activities under GAAP, with options under IFRS.

BackBack

BackBack

05:02

05:02