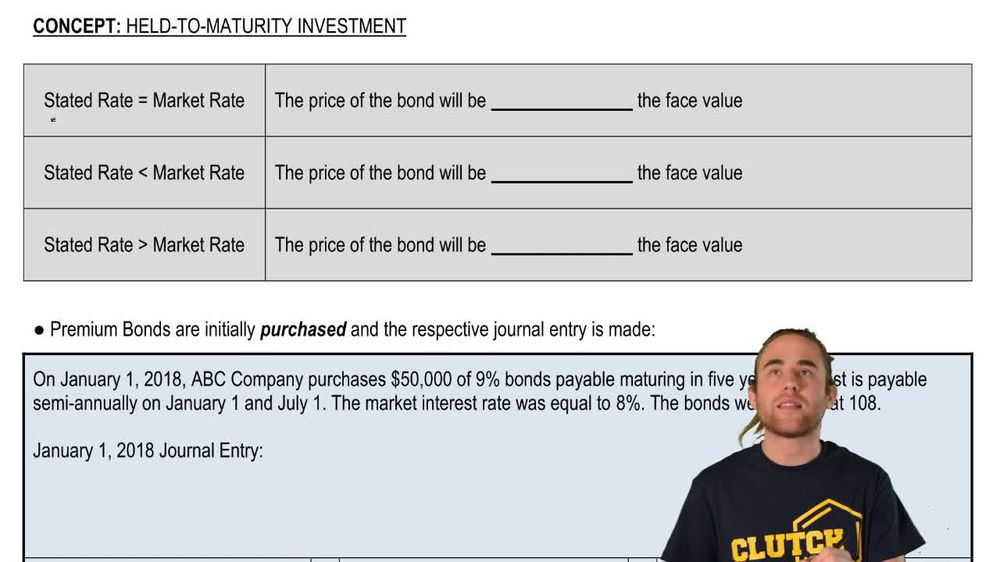

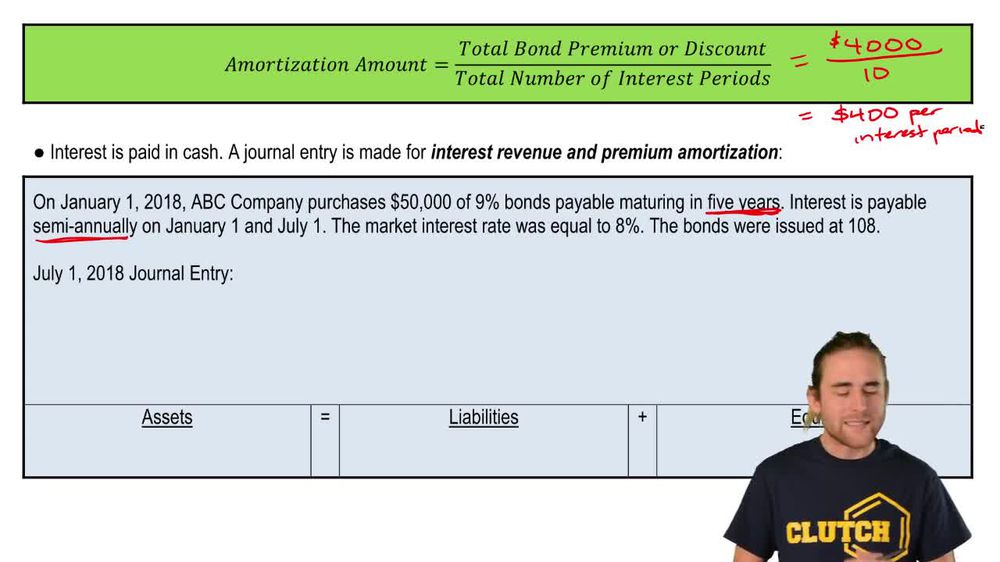

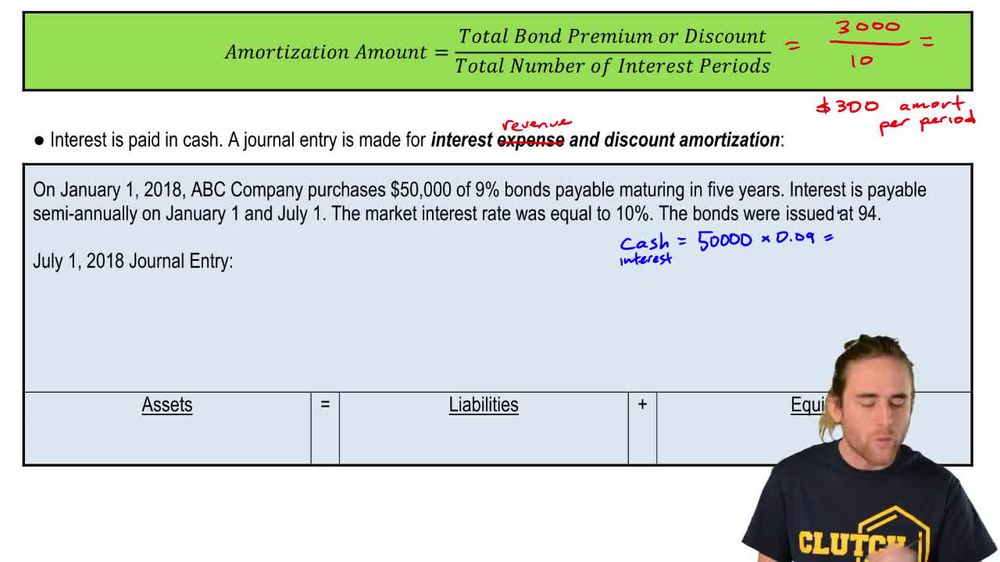

What are held-to-maturity (HTM) securities, and how are they accounted for when purchased at a premium or discount?

Held-to-maturity (HTM) securities are debt investments, like bonds, that a company intends and is able to hold until maturity. When purchased at a premium (above face value), the premium is amortized over the bond's life, reducing interest revenue each period. When purchased at a discount (below face value), the discount is amortized over the bond's life, increasing interest revenue each period. The straight-line method is commonly used for amortization in educational settings.

Back

Back

03:45

03:45