Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Initial Cost of Long Lived Assets definitions

You can tap to flip the card.

Long-lived Assets

You can tap to flip the card.

👆

Long-lived Assets

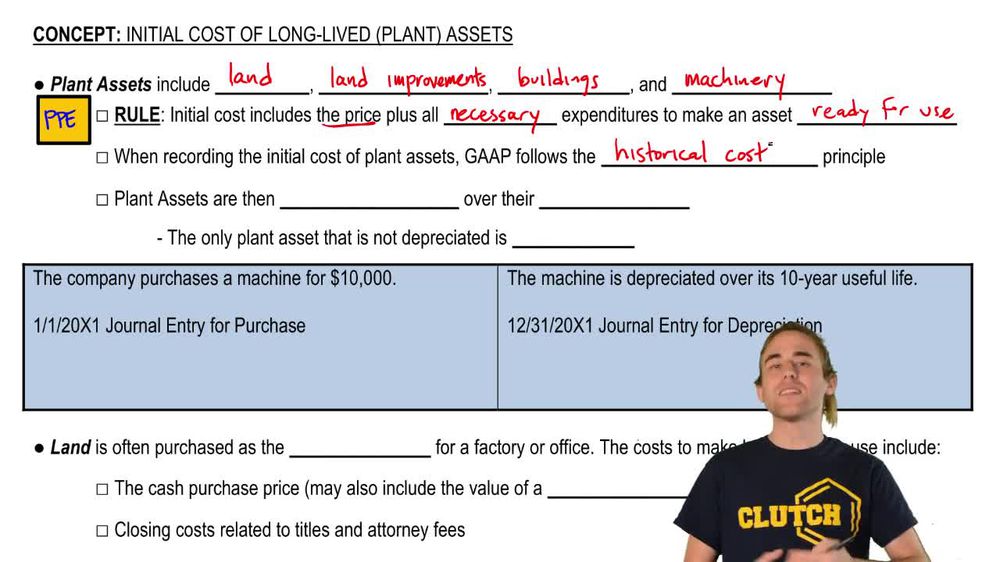

Resources expected to provide economic benefits for multiple years, including land, land improvements, buildings, and machinery.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Initial Cost of Long Lived Assets quiz

Initial Cost of Long Lived Assets

15 Terms

Initial Cost of Long Lived Assets

8. Long Lived Assets

10 problems

Topic

Basket (Lump-sum) Purchases

8. Long Lived Assets

10 problems

Topic

8. Long Lived Assets

14 topics

15 problems

Chapter

Guided course

11:36

Introduction to Plant Assets (Fixed Assets, PPE)

2020

views

49

rank

Guided course

02:00

Initial Cost of Buildings

913

views

9

rank

Guided course

09:26

Initial Cost of Land

1181

views

26

rank

Terms in this set (15)

Hide definitions

Long-lived Assets

Resources expected to provide economic benefits for multiple years, including land, land improvements, buildings, and machinery.

Property, Plant, and Equipment

A balance sheet category encompassing tangible long-term assets used in business operations, often abbreviated as PPE.

Historical Cost Principle

Accounting guideline requiring assets to be recorded at the original purchase price plus necessary expenditures, not adjusted for market changes.

Land

A non-depreciable fixed asset representing the ground owned by a business, excluding any structures or improvements.

Land Improvements

Additions to land such as fences, parking lots, or lighting, which have limited useful lives and are subject to depreciation.

Leasehold Improvements

Alterations made to leased property by the lessee, depreciated over the shorter of the lease term or the improvement's useful life.

Buildings

Structures owned by a business, recorded at cost including purchase price and necessary expenditures, and depreciated over their useful lives.

Machinery

Tangible assets like equipment used in production, capitalized at all costs to make them operational, and depreciated over time.

Depreciation

Systematic allocation of an asset's cost over its useful life, reflecting wear and tear or obsolescence, except for land.

Useful Life

Estimated period over which a fixed asset is expected to contribute to business operations and generate revenue.

Accumulated Depreciation

Contra asset account representing the total depreciation expense charged against an asset since its acquisition.

Contra Asset

An account that offsets a related asset account on the balance sheet, such as accumulated depreciation reducing asset book value.

Necessary Expenditures

All costs required to acquire an asset and prepare it for intended use, including taxes, installation, and removal of old structures.

Salvage Value

Estimated residual value received from disposing of an asset or its components, deducted from initial cost calculations.

Capitalization

Process of recording expenditures as part of an asset's cost on the balance sheet, rather than expensing them immediately.

BackBack

BackBack

11:36

11:36