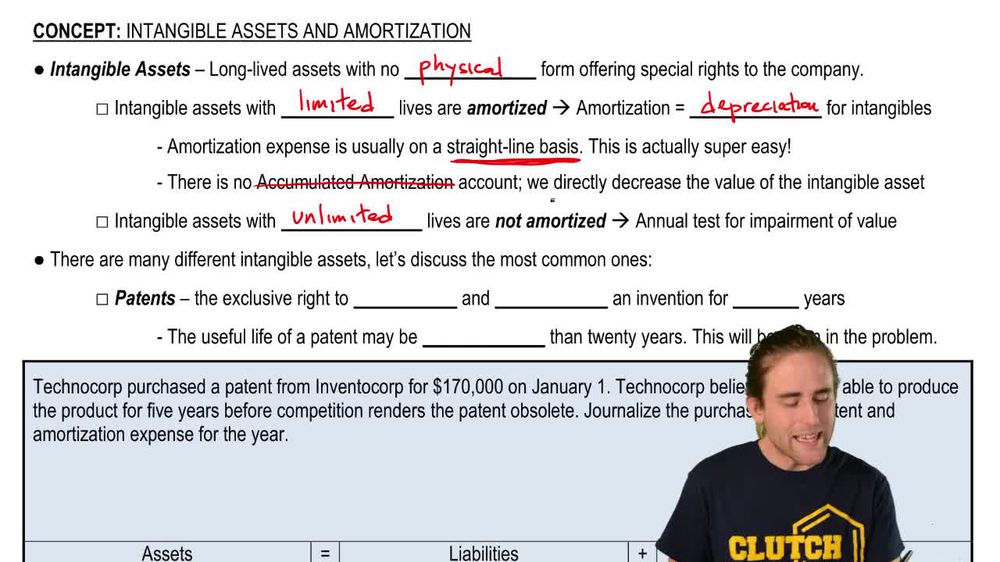

What is an intangible asset, and how does it differ from a tangible asset?

An intangible asset is a long-lived asset without physical form that provides special rights to a company, such as patents or trademarks, whereas a tangible asset has a physical presence, like machinery or buildings.

Back

Back

10:18

10:18