Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Issuing Par Value Stock definitions

You can tap to flip the card.

Common Stock

You can tap to flip the card.

👆

Common Stock

Equity account representing ownership in a company, credited with the par value of shares issued.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Issuing Par Value Stock quiz

Issuing Par Value Stock

15 Terms

Issuing Par Value Stock

12. Stockholders' Equity

10 problems

Topic

Issuing No Par Value Stock

12. Stockholders' Equity

10 problems

Topic

12. Stockholders' Equity

12 topics

15 problems

Chapter

Guided course

05:26

Issuing Par Value Stock above Par Value

1009

views

45

rank

Guided course

03:10

Issuing Par Value Stock Definitions

1329

views

32

rank

Guided course

04:03

Issuing Par Value Stock at Par Value

1107

views

30

rank

Terms in this set (15)

Hide definitions

Common Stock

Equity account representing ownership in a company, credited with the par value of shares issued.

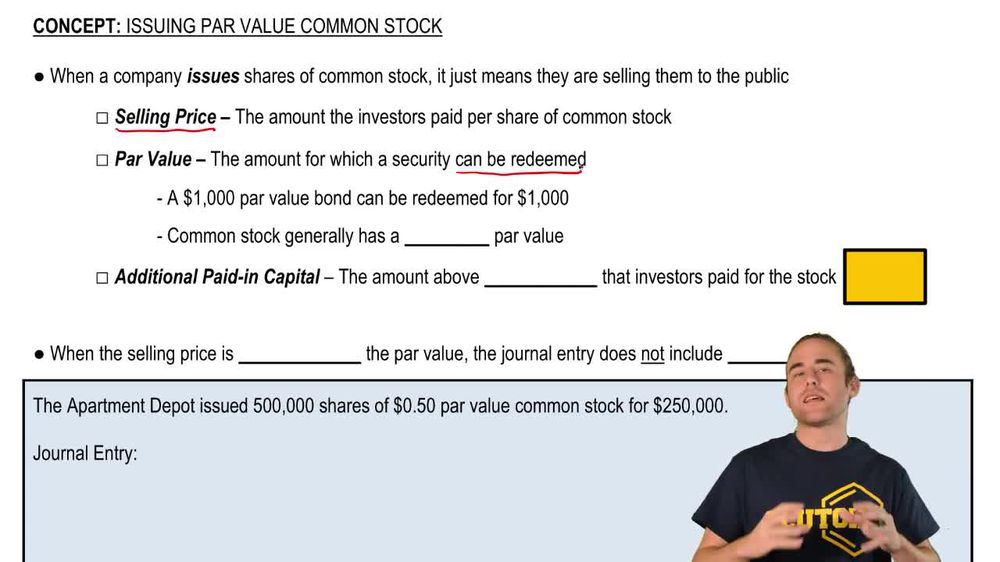

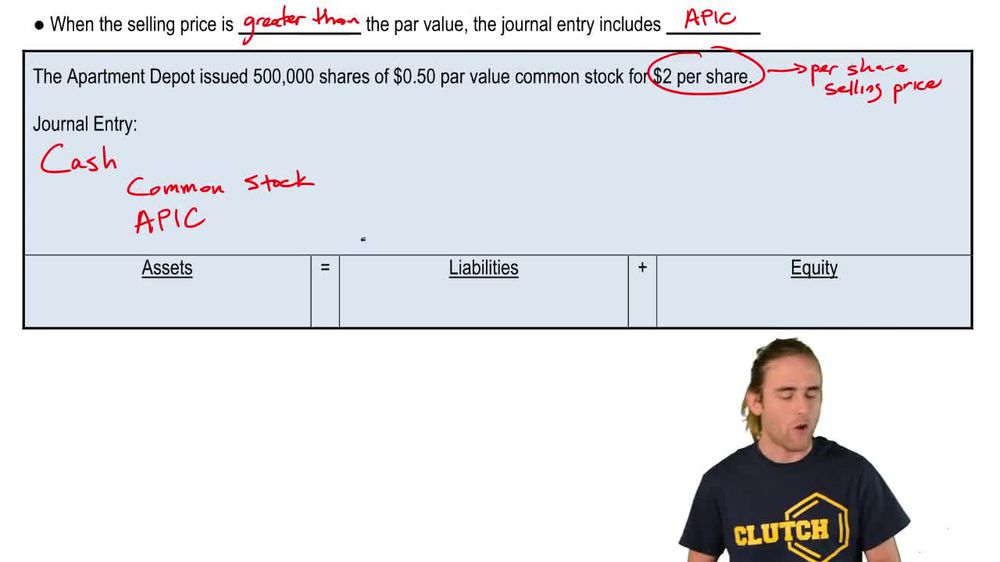

Par Value

Nominal amount assigned to each share, typically low, used to allocate proceeds in equity accounts.

Additional Paid-In Capital

Equity account for amounts received from stock issuance above par value, often abbreviated as APIC.

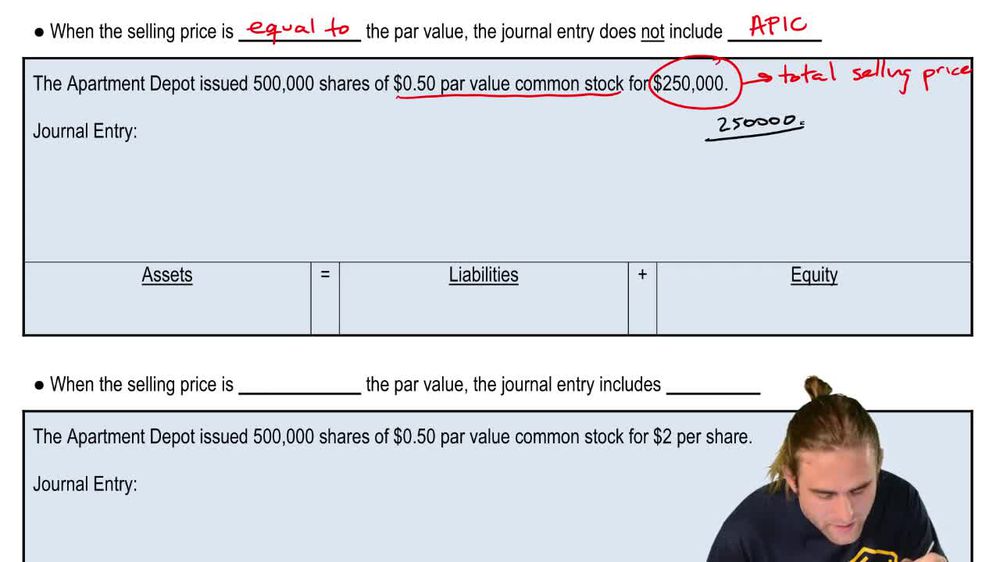

Selling Price

Amount at which shares are sold to investors, can be stated per share or as a total for all shares.

Equity

Ownership interest in a company, increased by proceeds from issuing common stock.

Journal Entry

Accounting record showing debits and credits for transactions, such as stock issuance.

Cash

Asset account debited for the total amount received from selling stock.

Shares

Units of ownership in a corporation, each representing a portion of equity.

Credit Balance

Normal balance for equity accounts like common stock and APIC, increased by stock issuance.

Debit

Accounting entry that increases assets, such as cash received from stock sales.

Assets

Resources owned by a company, increased by cash from issuing stock.

Liabilities

Obligations of a company, unaffected directly by stock issuance but part of the accounting equation.

Accounting Equation

Fundamental relationship: assets equal liabilities plus equity, maintained during stock issuance.

Paid-In Capital in Excess of Par

Alternative term for APIC, representing amounts received above par value for issued shares.

Ownership

Stake in a company acquired by purchasing common stock, reflected in equity accounts.

BackBack

BackBack

05:26

05:26