Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Journal Entries: Debits and Credits definitions

3 students found this helpful

You can tap to flip the card.

Transaction

You can tap to flip the card.

👆

Transaction

An event involving the exchange of value between accounts, impacting at least two accounts in the accounting records.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Journal Entries: Debits and Credits quiz #1

Journal Entries: Debits and Credits

40 Terms

Journal Entries: Debits and Credits quiz #2

Journal Entries: Debits and Credits

35 Terms

Journal Entries: Debits and Credits

2. Transaction Analysis

10 problems

Topic

Accounting Flow Intuition: BASE Formula

2. Transaction Analysis

10 problems

Topic

2. Transaction Analysis

5 topics

15 problems

Chapter

Guided course

02:35

Journal Entries: Debits and Credits

8185

views

207

rank

Guided course

04:24

Journal Entry

5423

views

152

rank

Terms in this set (15)

Hide definitions

Transaction

An event involving the exchange of value between accounts, impacting at least two accounts in the accounting records.

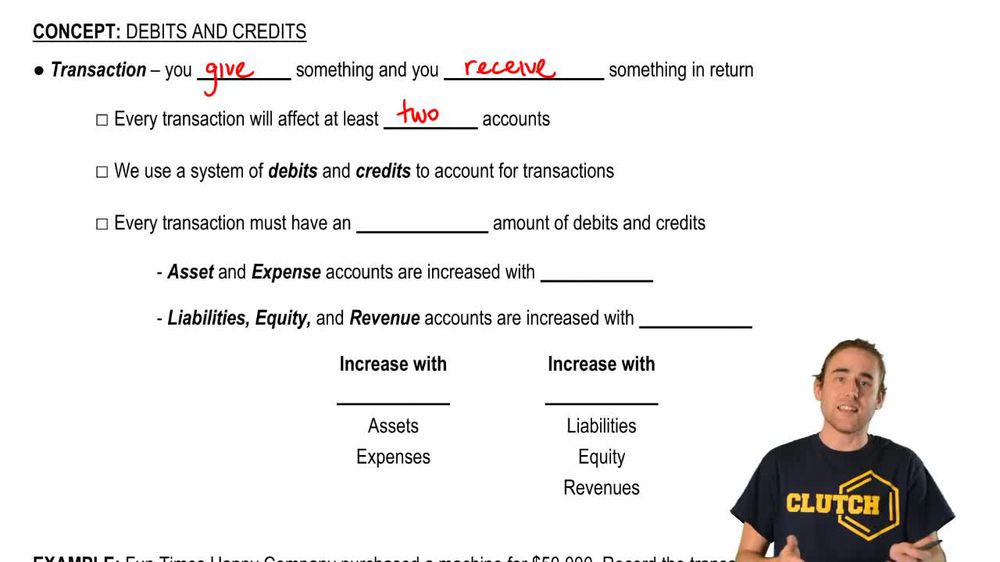

Debit

An entry on the left side of an account, used to increase assets and expenses or decrease liabilities, equity, and revenue.

Credit

An entry on the right side of an account, used to increase liabilities, equity, and revenue or decrease assets and expenses.

Asset

A resource owned by a company, such as cash or land, that provides future economic benefit.

Liability

An obligation or debt owed by a company to outsiders, representing claims against assets.

Equity

The residual interest in the assets of a company after deducting liabilities; represents ownership.

Revenue

Income earned from the sale of goods or services, increasing equity through credits.

Expense

Costs incurred in the process of earning revenue, decreasing equity and increased by debits.

Account

A record used to track increases and decreases in specific assets, liabilities, equity, revenue, or expenses.

Accounts Receivable

A type of asset representing amounts owed to a company by customers for goods or services provided.

Accounts Payable

A liability account showing amounts a company owes to suppliers or creditors for purchases made on credit.

Retained Earnings

Cumulative net income of a company that has been kept rather than distributed to shareholders.

Investment Account

An account used to record the value of investments held by a company, such as stocks or bonds.

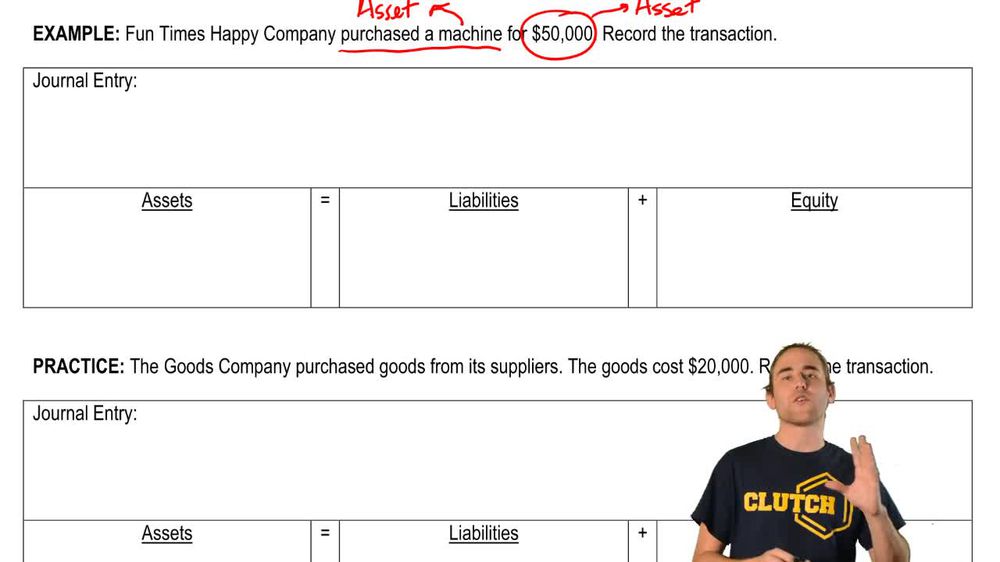

Journal Entry

A formal record of a transaction, showing which accounts are debited and credited and by what amounts.

Double-Entry System

An accounting method where every transaction affects at least two accounts, ensuring debits equal credits.

BackBack

BackBack

02:35

02:35