Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Limitations of Internal Controls definitions

You can tap to flip the card.

Internal Controls

You can tap to flip the card.

👆

Internal Controls

Systems designed to prevent or detect fraud and ensure the safeguarding of assets and reliability of financial information.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Limitations of Internal Controls quiz #1

Limitations of Internal Controls

10 Terms

Limitations of Internal Controls

6. Internal Controls and Reporting Cash

10 problems

Topic

Petty Cash

6. Internal Controls and Reporting Cash

10 problems

Topic

6. Internal Controls and Reporting Cash

8 topics

15 problems

Chapter

Guided course

03:59

Limitations of Internal Controls

1195

views

45

rank

Terms in this set (15)

Hide definitions

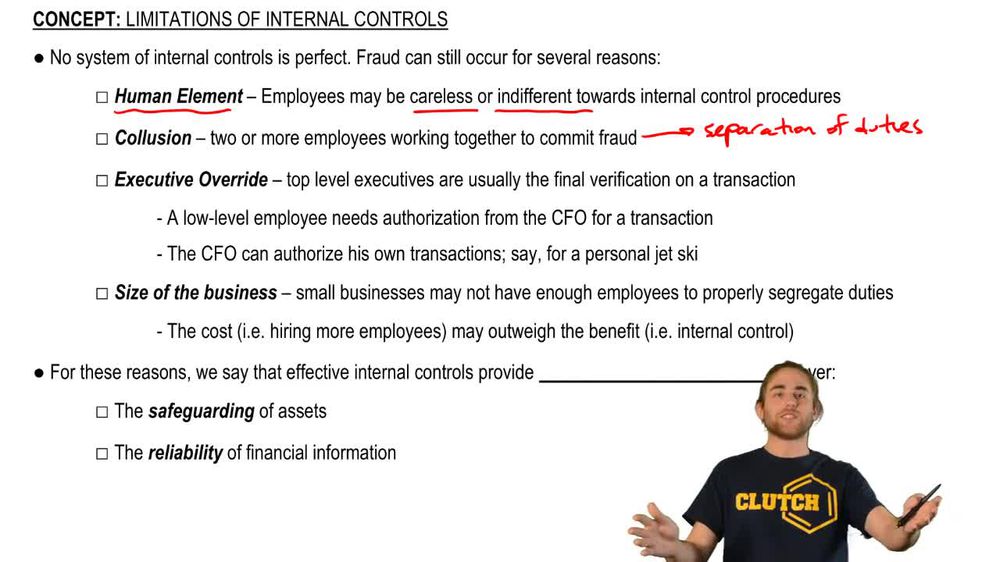

Internal Controls

Systems designed to prevent or detect fraud and ensure the safeguarding of assets and reliability of financial information.

Fraud

Intentional deception or misappropriation of company resources, often targeted by internal control systems.

Human Error

Mistakes or oversights by employees that can undermine the effectiveness of established procedures.

Carelessness

Lack of attention or diligence by staff, potentially leading to the failure of control measures.

Indifference

Employee attitude of disregard toward procedures, reducing the effectiveness of internal controls.

Collusion

Cooperation between two or more employees to bypass controls and commit fraud, defeating separation of duties.

Separation of Duties

Division of responsibilities among employees to reduce the risk of error or fraud.

Executive Override

Ability of high-level management to bypass controls, often by authorizing their own transactions.

CFO

Top financial executive who may have authority to approve transactions without additional oversight.

Small Business

Organization with limited staff, making it challenging to implement effective separation of duties.

Cost-Benefit Analysis

Evaluation of whether the expense of implementing controls is justified by the potential reduction in fraud risk.

Trustworthiness

Reliability and integrity of employees, a factor considered when deciding on the extent of controls.

Reasonable Assurance

Level of confidence provided by controls, indicating a high but not absolute likelihood of achieving objectives.

Safeguarding of Assets

Protection of company resources from loss, theft, or misuse through internal control measures.

Reliability of Financial Information

Confidence that reported financial data accurately reflects the company's true financial position.

BackBack

BackBack

03:59

03:59