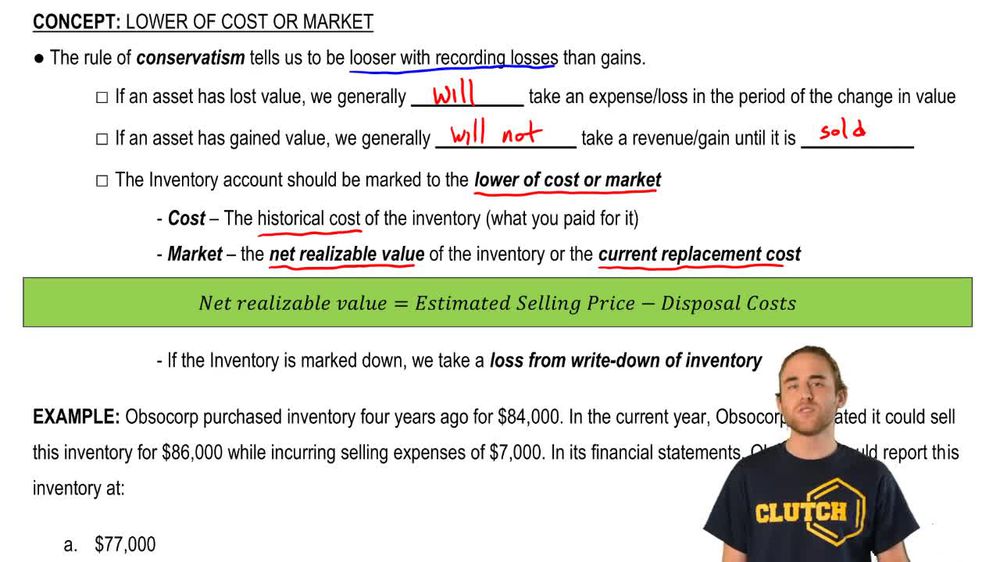

What is the rule of conservatism in accounting, and how does it affect the recording of asset values?

The rule of conservatism requires accountants to record losses more readily than gains, meaning asset values are reduced immediately if they decline, but increases in value are only recognized upon sale.

Back

Back

07:09

07:09