What is the purpose of the allowance for doubtful accounts in accounting for accounts receivable?

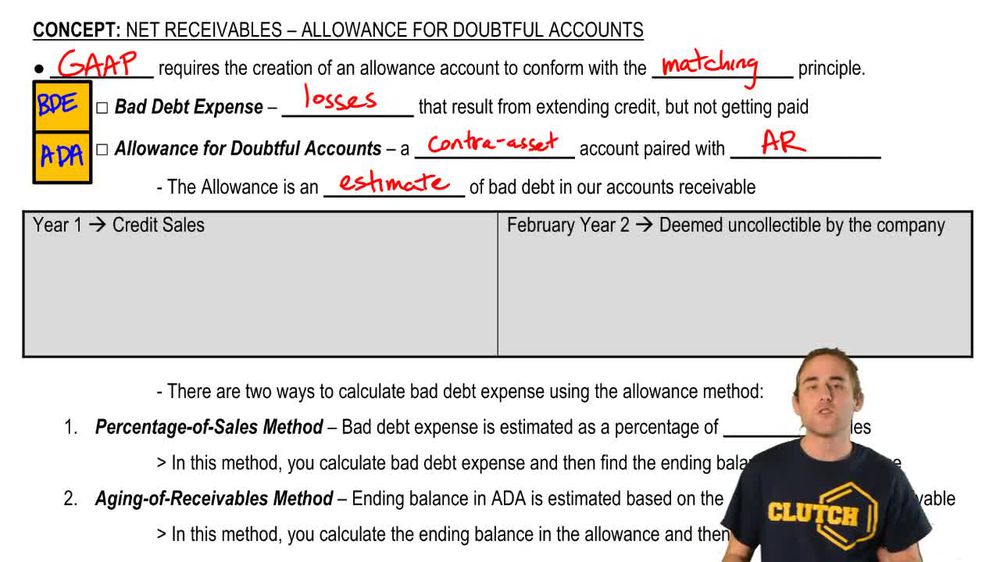

The allowance for doubtful accounts estimates the portion of accounts receivable that is expected to be uncollectible, ensuring adherence to the matching principle.

Why is the direct write-off method not compliant with GAAP?

The direct write-off method is not GAAP compliant because it does not match bad debt expense with the related revenue in the same period, violating the matching principle.

How is bad debt expense recorded under the allowance method in the first year?

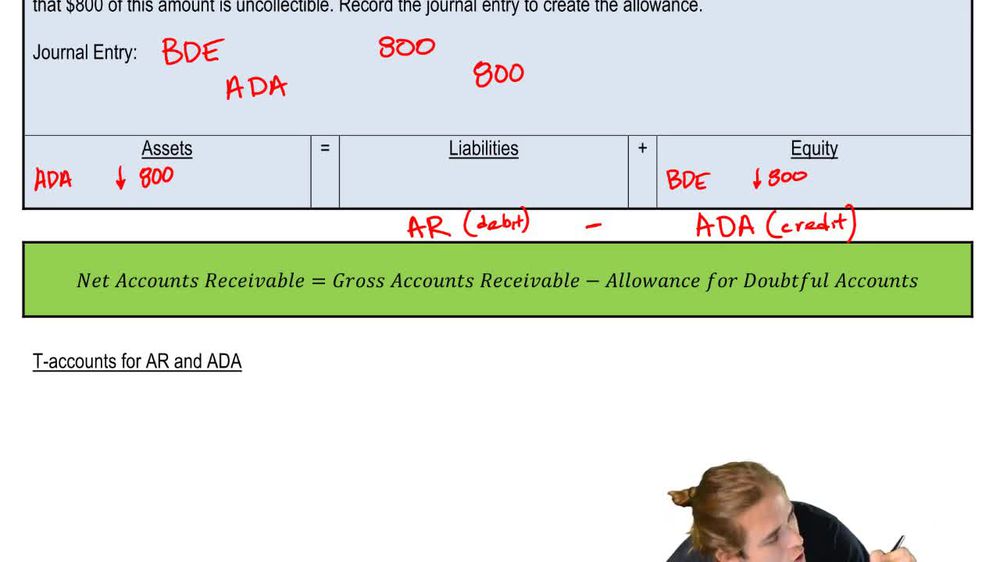

Bad debt expense is estimated and recorded by debiting bad debt expense and crediting the allowance for doubtful accounts.

What type of account is the allowance for doubtful accounts, and what is its normal balance?

The allowance for doubtful accounts is a contra asset account with a normal credit balance.

How does the allowance for doubtful accounts affect the net accounts receivable balance?

The allowance for doubtful accounts reduces the accounts receivable balance to reflect the amount expected to be collected, resulting in net accounts receivable.

What journal entry is made when an account is determined to be uncollectible under the allowance method?

Debit allowance for doubtful accounts and credit accounts receivable.

When is bad debt expense recognized under the allowance method?

Bad debt expense is recognized in the same period as the related credit sales, based on an estimate.

What are the two main methods for estimating the allowance for doubtful accounts?

The percentage of sales method and the aging of receivables method.

How does the percentage of sales method estimate bad debt expense?

It estimates bad debt expense as a percentage of total credit sales for the period.

How does the aging of receivables method estimate the allowance for doubtful accounts?

It estimates the required ending balance in the allowance account based on the age of each receivable, with older receivables considered more likely to be uncollectible.

What is the matching principle and how does the allowance method comply with it?

The matching principle requires expenses to be recorded in the same period as the related revenues; the allowance method does this by estimating and recording bad debt expense in the same period as credit sales.

What is the effect on bad debt expense when an account is written off in a later period under the allowance method?

No additional bad debt expense is recorded when an account is written off, as the expense was already recognized in the earlier period.

What is a contra asset account?

A contra asset account is an account that offsets a related asset account, having an opposite normal balance.

How is net accounts receivable calculated?

Net accounts receivable is calculated as accounts receivable minus the allowance for doubtful accounts.

Why is it important to estimate uncollectible accounts?

Estimating uncollectible accounts ensures that financial statements reflect a more accurate value of receivables and comply with the matching principle.

What is the journal entry to record estimated bad debt expense at year-end?

Debit bad debt expense and credit allowance for doubtful accounts.

If a previously written-off account is later collected, what is the appropriate accounting treatment?

First, reverse the write-off by debiting accounts receivable and crediting allowance for doubtful accounts, then record the cash collection by debiting cash and crediting accounts receivable.

What is the main difference between the percentage of sales and aging of receivables methods?

The percentage of sales method estimates bad debt expense directly, while the aging of receivables method estimates the required ending balance in the allowance account.

How does the allowance for doubtful accounts appear on the balance sheet?

It is shown as a deduction from accounts receivable to arrive at net accounts receivable.

What is bad debt expense?

Bad debt expense is the estimated loss from credit sales that are not expected to be collected.

Why is the allowance for doubtful accounts considered a contra asset?

Because it has a credit balance and reduces the total accounts receivable, which has a debit balance.

What happens to the allowance for doubtful accounts when an account is written off?

The allowance for doubtful accounts is debited, reducing its balance.

How does the aging of receivables method help in estimating uncollectible accounts?

It categorizes receivables by age and applies different uncollectibility rates to each category to estimate the total allowance needed.

What is the impact on the income statement when bad debt expense is recorded?

Bad debt expense increases total expenses, reducing net income.

How does the allowance method improve the accuracy of financial statements?

It provides a more realistic estimate of collectible receivables and matches expenses with revenues.

What is the normal balance of accounts receivable and allowance for doubtful accounts?

Accounts receivable has a normal debit balance; allowance for doubtful accounts has a normal credit balance.

What is the effect of underestimating bad debt expense in the allowance method?

Net income will be overstated and net accounts receivable will be overstated.

What is the effect of overestimating bad debt expense in the allowance method?

Net income will be understated and net accounts receivable will be understated.

Why is the allowance for doubtful accounts necessary for companies that sell on credit?

It allows companies to anticipate and account for potential losses from customers who do not pay.

How does the write-off of an account affect total assets?

It does not affect total assets, as both accounts receivable and the allowance for doubtful accounts decrease by the same amount.

What is the primary objective of using the allowance method for bad debts?

To match bad debt expense with the related revenue and present a realistic value of receivables.

How is the percentage used in the percentage of sales method determined?

It is based on historical data and management's judgment about the proportion of credit sales that will be uncollectible.

What is the effect on the allowance for doubtful accounts if actual write-offs exceed the estimated allowance?

The allowance account will have a debit balance, indicating that the estimate was too low and an additional expense may be needed.

What is the effect on the allowance for doubtful accounts if actual write-offs are less than the estimated allowance?

The allowance account will have a remaining credit balance, indicating that the estimate was more than sufficient.

What does a debit balance in the Allowance for Doubtful Accounts indicate in financial accounting?

A debit balance in the Allowance for Doubtful Accounts indicates that actual write-offs of uncollectible accounts have exceeded previous estimates of bad debts, meaning more accounts were written off than had been allowed for.

At what value are accounts receivable normally reported on the balance sheet under GAAP?

Accounts receivable are normally reported at their net realizable value, which is the gross accounts receivable minus the Allowance for Doubtful Accounts.

How does the Allowance for Doubtful Accounts affect the reported value of accounts receivable?

The Allowance for Doubtful Accounts is a contra asset account with a credit balance that reduces the gross accounts receivable to its net realizable value on the balance sheet.

How is bad debt expense reported on the financial statements?

Bad debt expense is reported on the income statement as an operating expense, reflecting estimated losses from uncollectible accounts.

What is the purpose of using an allowance account for doubtful accounts in financial accounting?

The allowance account for doubtful accounts is used to estimate and record expected uncollectible amounts, ensuring that bad debt expense is matched with related revenue in the same period according to the matching principle.

What are two common methods for estimating the Allowance for Doubtful Accounts?

The two common methods are the percentage of sales method, which estimates bad debt expense as a percentage of credit sales, and the aging of receivables method, which estimates the ending balance in the allowance based on the age of each receivable.

Back

Back

05:50

05:50