What is bad debt expense and when does it arise in accounting?

Bad debt expense arises when credit extended to customers is not repaid, resulting in a loss for the company.

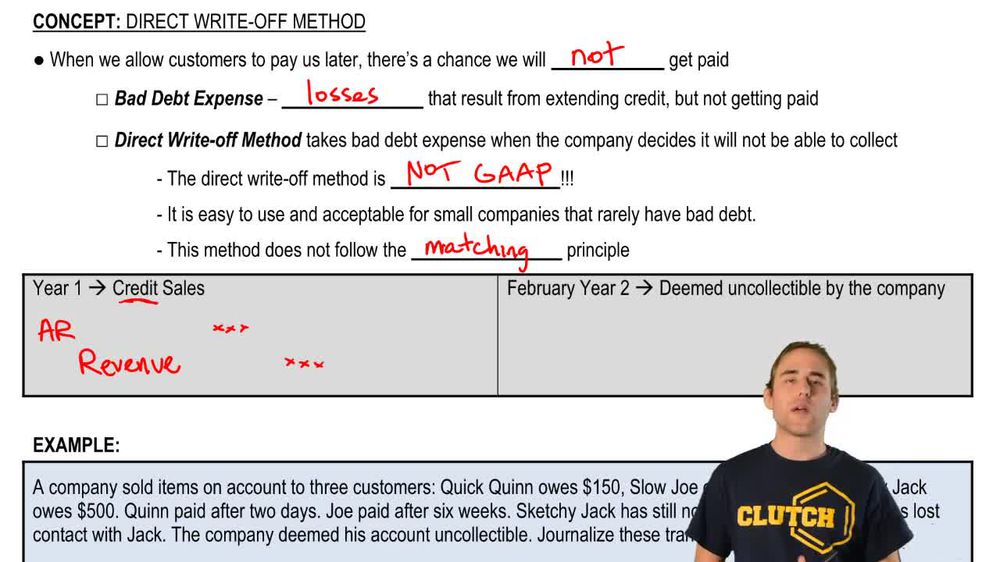

How does the direct write-off method record bad debt expense?

The direct write-off method records bad debt expense only when it is certain that a specific account will not be collected.

Why does the direct write-off method violate the matching principle?

It violates the matching principle because it records bad debt expense in a different period from when the related revenue was recognized.

What is the matching principle in accounting?

The matching principle requires that expenses be recorded in the same period as the revenues they help generate.

Is the direct write-off method compliant with Generally Accepted Accounting Principles (GAAP)?

No, the direct write-off method is not GAAP-compliant because it does not follow the matching principle.

When is revenue recorded under the direct write-off method?

Revenue is recorded at the time of the credit sale, regardless of when or if the receivable is collected.

When is bad debt expense recorded under the direct write-off method?

Bad debt expense is recorded only when a specific account is deemed uncollectible.

What journal entry is made when a sale is made on account under the direct write-off method?

Debit Accounts Receivable and credit Revenue for the amount of the sale.

What journal entry is made when a customer pays off their account under the direct write-off method?

Debit Cash and credit Accounts Receivable for the amount received.

What journal entry is made when an account is written off as uncollectible under the direct write-off method?

Debit Bad Debt Expense and credit Accounts Receivable for the uncollectible amount.

How does the direct write-off method affect the income statement?

Bad debt expense is reported on the income statement in the period the account is written off, not when the related revenue was earned.

How does the direct write-off method affect the balance sheet?

Accounts Receivable is reduced only when a specific account is written off, potentially overstating assets until that point.

Why is the direct write-off method considered simple to use?

It is simple because bad debt expense is only recorded when an account is clearly uncollectible, requiring fewer estimates and adjustments.

In the example provided, what happens when Quick Quinn pays his debt promptly?

The company debits Cash and credits Accounts Receivable for the amount paid by Quick Quinn.

In the example, what is the accounting treatment when Sketchy Jack's account is deemed uncollectible?

The company debits Bad Debt Expense and credits Accounts Receivable for the amount owed by Sketchy Jack.

What is the main disadvantage of the direct write-off method?

The main disadvantage is that it does not match bad debt expense with the related revenue, leading to less accurate financial statements.

How does the direct write-off method potentially misstate net income?

It can overstate net income in the period of the sale and understate it in the period when the bad debt is written off.

Why might a company use the direct write-off method despite its shortcomings?

A company might use it for its simplicity, especially if uncollectible accounts are infrequent or immaterial.

What is the impact of the direct write-off method on net accounts receivable?

Net accounts receivable may be overstated until uncollectible accounts are actually written off.

How does the direct write-off method differ from the allowance method?

The direct write-off method records bad debts only when specific accounts are uncollectible, while the allowance method estimates bad debts in the same period as the related sales.

What is the effect of the direct write-off method on financial statement users?

It may mislead users by not accurately reflecting the risk of uncollectible accounts in the period the revenue is earned.

What is the correct journal entry to write off a \$500 uncollectible account under the direct write-off method?

Debit Bad Debt Expense \$500; credit Accounts Receivable \$500.

Why is the direct write-off method commonly tested in accounting exams?

Because it is straightforward and helps illustrate the concept of bad debt expense, despite not being GAAP-compliant.

What happens to accounts receivable when a bad debt is written off using the direct write-off method?

Accounts receivable is reduced by the amount of the written-off account.

What is the primary reason the direct write-off method is not preferred under GAAP?

Because it does not match expenses with revenues, leading to less accurate financial reporting.

Back

Back

05:59

05:59