Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Operating Activities: Indirect Method definitions

You can tap to flip the card.

Indirect Method

You can tap to flip the card.

👆

Indirect Method

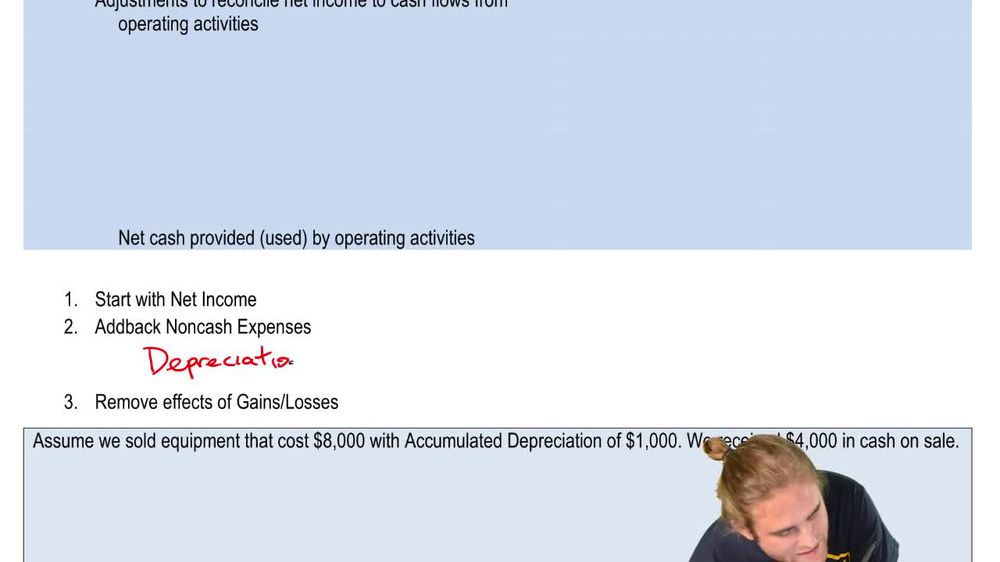

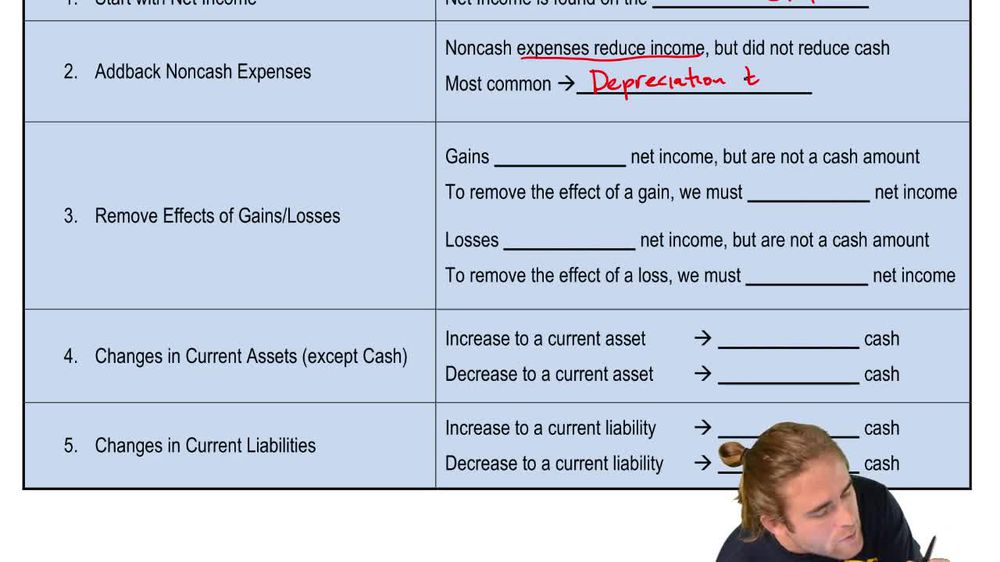

A process starting with net income and adjusting for non-cash items and working capital changes to determine operating cash flows.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Operating Activities: Indirect Method quiz #1

Operating Activities: Indirect Method

10 Terms

Operating Activities: Indirect Method

13. Statement of Cash Flows

10 problems

Topic

Operating Activities: Direct Method

13. Statement of Cash Flows

9 problems

Topic

13. Statement of Cash Flows

6 topics

15 problems

Chapter

Guided course

07:11

Indirect Method (3)

1260

views

29

rank

Guided course

06:35

Indirect Method (1)

1608

views

45

rank

1

comments

Guided course

08:54

Indirect Method Summary

2351

views

67

rank

Terms in this set (15)

Hide definitions

Indirect Method

A process starting with net income and adjusting for non-cash items and working capital changes to determine operating cash flows.

Net Income

The bottom-line figure from the income statement, serving as the starting point for calculating operating cash flows.

Operating Cash Flows

Cash generated or used by a company's core business activities, excluding investing and financing transactions.

Non-cash Expenses

Items like depreciation or amortization that reduce net income but do not involve actual cash outflows.

Depreciation Expense

An allocation of the cost of tangible assets over their useful lives, representing wear and tear without cash movement.

Amortization

A systematic reduction of intangible asset value over time, similar to depreciation but for non-physical assets.

Gain

An increase in net income from selling assets above book value, not representing a cash inflow in operating activities.

Loss

A decrease in net income from selling assets below book value, not representing a cash outflow in operating activities.

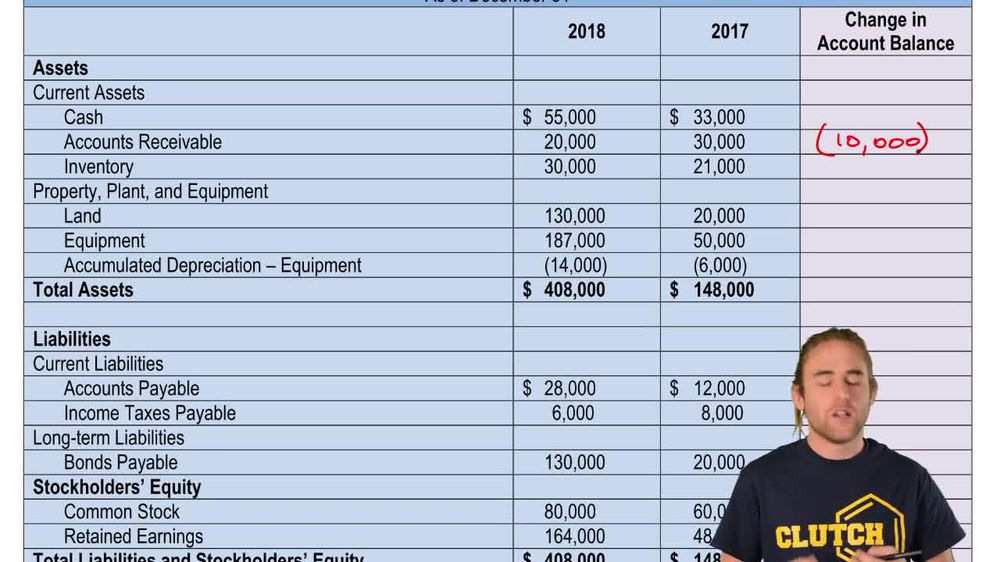

Current Asset

Resources expected to be converted to cash within a year, such as inventory or receivables, excluding cash itself.

Current Liability

Obligations due within one year, like accounts payable, affecting cash flow calculations in the indirect method.

Accounts Payable

Amounts owed to suppliers for goods or services received, classified as a current liability on the balance sheet.

Inventory

Goods held for sale or production, classified as a current asset and impacting cash flow when its balance changes.

Book Value

The recorded value of an asset on the balance sheet, used to determine gains or losses upon sale.

Income Statement

A financial report showing revenues and expenses over a period, providing the net income figure for cash flow calculations.

Working Capital

The difference between current assets and current liabilities, with changes affecting operating cash flows.

BackBack

BackBack

07:11

07:11