What is the difference between gross pay and net pay in payroll accounting?

Gross pay is the total amount earned by an employee before deductions, while net pay is the amount the employee receives after taxes and other withholdings are subtracted.

Which taxes are typically withheld from an employee's paycheck?

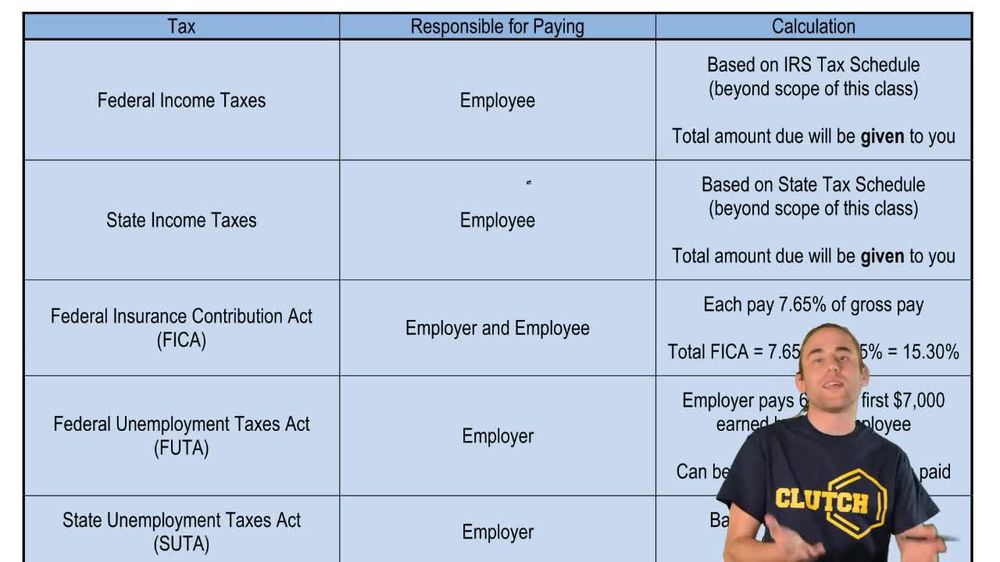

Federal income tax, state income tax (if applicable), and the employee's portion of FICA taxes (Social Security and Medicare) are typically withheld.

Who is responsible for remitting federal and state income taxes withheld from employees' paychecks?

The employer is responsible for remitting the withheld federal and state income taxes to the government on behalf of the employee.

What does FICA stand for, and what does it include?

FICA stands for Federal Insurance Contributions Act and includes Social Security and Medicare taxes.

What percentage of gross pay do both employees and employers contribute to FICA taxes?

Both employees and employers contribute 7.65% of gross pay to FICA taxes.

Who pays federal unemployment taxes (FUTA) and at what rate?

Employers pay federal unemployment taxes (FUTA) at a rate of 6.2% on the first \$7,000 earned by each employee.

What is SUTA and who is responsible for paying it?

SUTA stands for State Unemployment Tax Act, and it is paid by employers.

How are employee benefits such as health insurance and 401(k) plans treated in payroll accounting?

Employee benefits are considered part of salary and wage expense and may result in additional withholdings or direct payments by the employer.

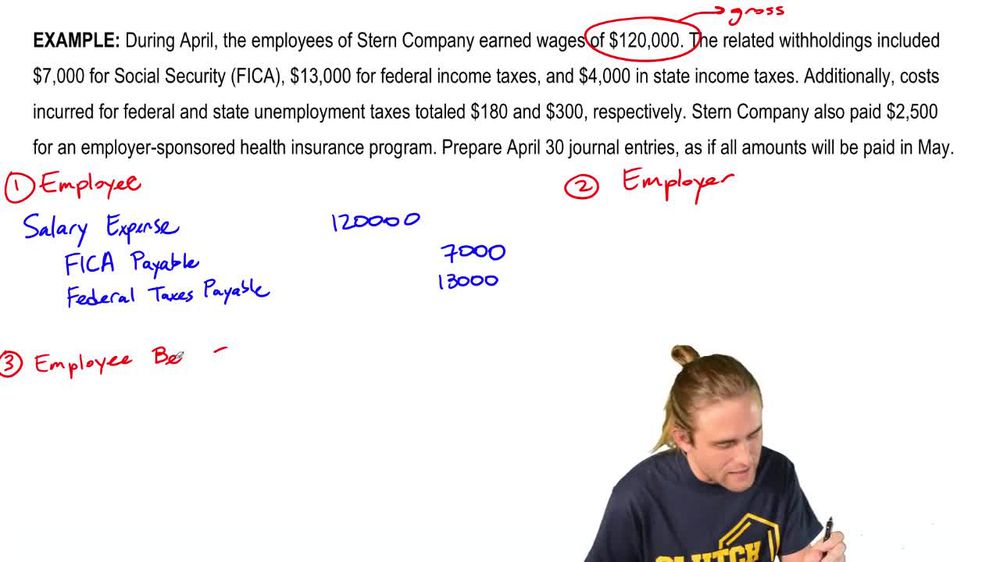

What are the typical journal entries for recording payroll expenses?

The typical journal entry debits salary expense and credits cash (for net pay) and payroll liabilities (for taxes and withholdings).

Why might the cash paid to employees be less than the salary expense recorded?

Cash paid is less because taxes and other withholdings are deducted from gross pay, with the employer remitting these amounts to the government.

Which party is responsible for paying unemployment taxes?

The employer is solely responsible for paying unemployment taxes (FUTA and SUTA).

What is the main purpose of withholding taxes from employees' paychecks?

Withholding ensures that employees' tax obligations are paid directly to the government throughout the year.

How does the employer account for payroll liabilities?

Payroll liabilities are credited when payroll is recorded and represent amounts owed to the government or other parties.

What is included in the salary and wage expense account?

Salary and wage expense includes gross pay, employer-paid taxes, and employee benefits.

How are employer-paid benefits recorded in payroll accounting?

Employer-paid benefits are recorded as part of salary and wage expense and reduce the employer's cash.

What is the effect of payroll taxes on a company's financial statements?

Payroll taxes increase expenses and liabilities, reducing net income and cash.

What is the main difference between employee and employer payroll tax responsibilities?

Employees are responsible for income and their share of FICA taxes, while employers pay their share of FICA and all unemployment taxes.

How is the employer's share of FICA taxes recorded?

The employer's share of FICA taxes is recorded as an additional payroll expense and liability.

What happens to the amounts withheld from employees' paychecks?

Withheld amounts are held as liabilities until remitted to the appropriate government agencies.

Why do employers withhold taxes from employees instead of having employees pay them directly?

Employers withhold taxes to ensure timely and accurate payment to the government, reducing the risk of underpayment by employees.

What is the journal entry to record the payment of payroll liabilities?

The journal entry debits payroll liabilities and credits cash when the liabilities are paid.

How does offering employee benefits affect payroll accounting?

Offering benefits increases salary and wage expense and may create additional withholdings or direct payments.

What is the impact of payroll taxes on net pay?

Payroll taxes reduce net pay, as they are deducted from gross pay before the employee receives their paycheck.

What is the purpose of the Federal Insurance Contributions Act (FICA)?

FICA funds Social Security and Medicare programs through payroll taxes collected from employees and employers.

How are state income taxes handled in payroll accounting?

State income taxes are withheld from employees' paychecks and remitted by the employer to the state government.

What is the significance of the \$7,000 wage base for FUTA taxes?

FUTA taxes are only applied to the first \$7,000 of each employee's annual earnings.

How do payroll liabilities affect the balance sheet?

Payroll liabilities appear as current liabilities until they are paid to the appropriate parties.

What is the relationship between salary expense and cash paid to employees?

Salary expense reflects gross pay, while cash paid is net pay after deductions.

Why are payroll taxes considered an expense for the employer?

Payroll taxes represent additional costs incurred by the employer for employing workers.

What is the main reason for employers to offer benefits like health insurance?

Employers offer benefits to attract and retain employees and to provide additional compensation beyond wages.

How are employee contributions to benefits like 401(k) plans handled in payroll?

Employee contributions are withheld from paychecks and remitted to the benefit provider by the employer.

What is the effect of payroll taxes on a company's cash flow?

Payroll taxes decrease cash flow as the company must remit withheld and employer-paid taxes to the government.

How does the employer's payment of unemployment taxes affect payroll accounting?

Employer-paid unemployment taxes are recorded as payroll expenses and reduce cash when paid.

What is the accounting treatment for taxes withheld but not yet remitted?

Withheld taxes not yet remitted are recorded as payroll liabilities on the balance sheet.

How does payroll accounting ensure compliance with tax laws?

Payroll accounting tracks withholdings and payments to ensure timely and accurate remittance to tax authorities.

What is the impact of payroll expenses on net income?

Payroll expenses reduce net income as they are recorded as operating expenses.

How are employer contributions to employee benefits recorded?

Employer contributions are recorded as salary and wage expense and reduce cash when paid.

What is the role of payroll liabilities in the payroll process?

Payroll liabilities represent amounts owed to third parties, such as the government or benefit providers, until paid.

How does the employer's share of payroll taxes differ from the employee's share?

The employer pays their own share of FICA and all unemployment taxes, while the employee pays income taxes and their share of FICA.

What is the effect of payroll withholdings on employees' take-home pay?

Payroll withholdings reduce employees' take-home pay by deducting taxes and other contributions from gross pay.

Back

Back

07:09

07:09