Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Periodic Inventory - FIFO, LIFO, and Average Cost definitions

You can tap to flip the card.

Periodic Inventory System

You can tap to flip the card.

👆

Periodic Inventory System

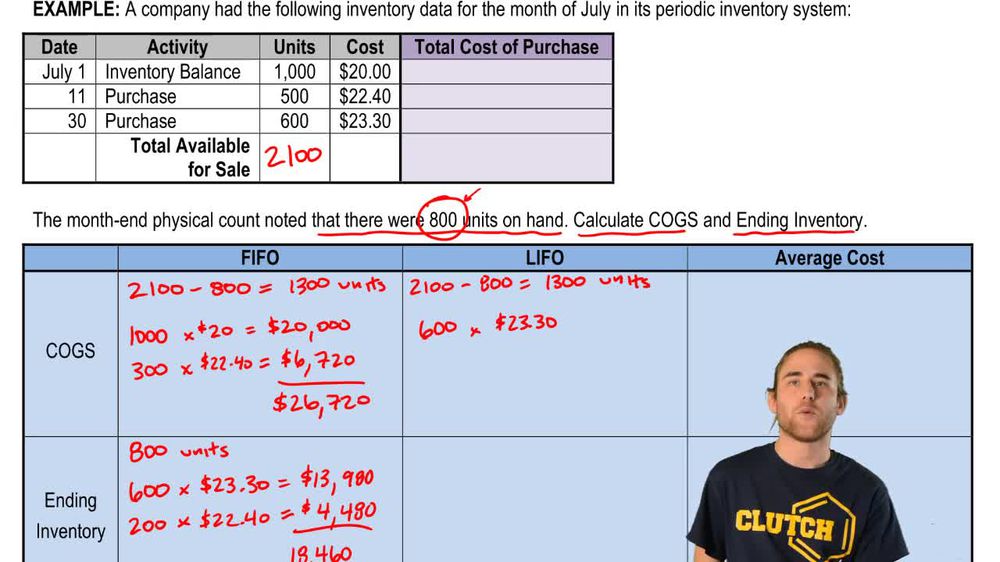

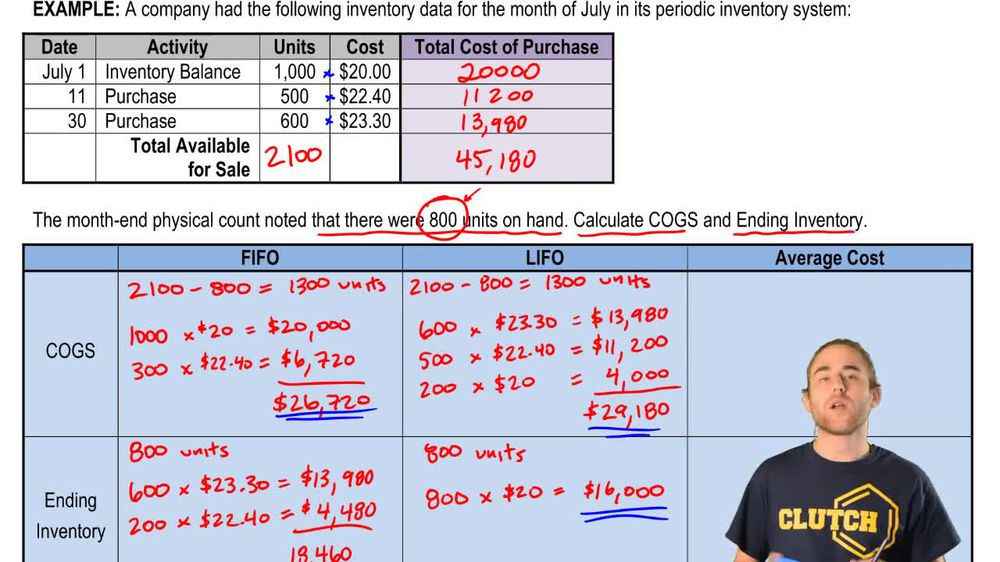

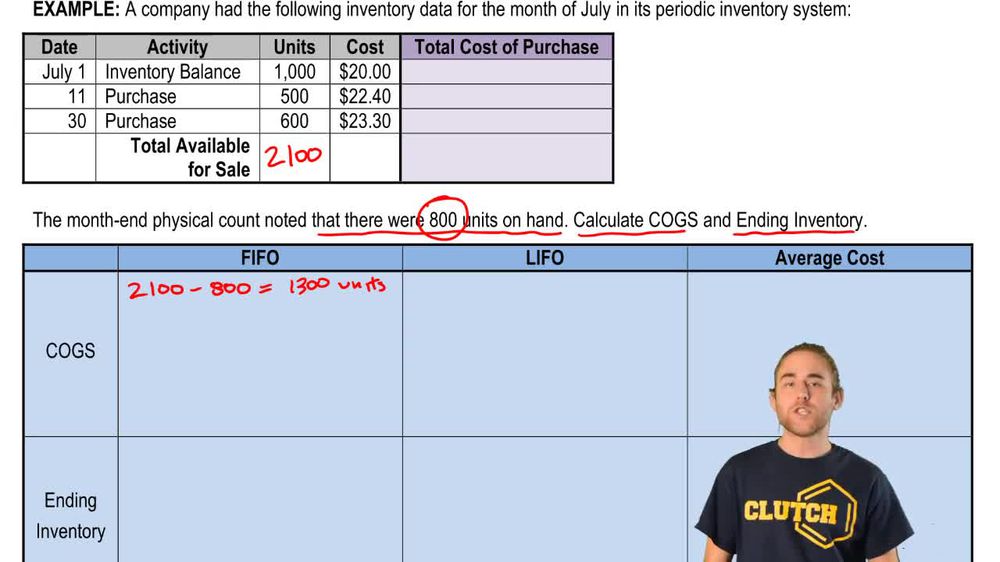

Inventory and cost of goods sold are updated only at the end of the period, not after each transaction.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Periodic Inventory - FIFO, LIFO, and Average Cost quiz #1

Periodic Inventory - FIFO, LIFO, and Average Cost

19 Terms

Periodic Inventory - FIFO, LIFO, and Average Cost

5. Inventory

10 problems

Topic

5. Inventory

7 topics

15 problems

Chapter

Guided course

06:32

Periodic Inventory FIFO Method

2824

views

38

rank

Guided course

04:30

Periodic Inventory LIFO Method

1905

views

31

rank

Guided course

06:23

Periodic Inventory Average Cost Method

1961

views

50

rank

Terms in this set (15)

Hide definitions

Periodic Inventory System

Inventory and cost of goods sold are updated only at the end of the period, not after each transaction.

FIFO

Costing method where the oldest inventory costs are assigned to cost of goods sold, reflecting earlier purchase prices.

LIFO

Costing method where the most recent inventory costs are assigned to cost of goods sold, reflecting latest purchase prices.

Average Cost Method

Costing method using the weighted average of all units' costs to determine cost of goods sold and ending inventory.

Cost Flow Assumption

Accounting approach for assigning costs to inventory and cost of goods sold, independent of the actual movement of goods.

Cost of Goods Sold

Total cost assigned to inventory items that have been sold during the period, reducing inventory value.

Ending Inventory

Value of unsold goods physically counted and reported at the end of the accounting period.

Goods Available for Sale

Sum of beginning inventory and purchases, representing all inventory that could be sold during the period.

Beginning Inventory

Inventory value carried over from the previous period, forming the starting point for current period calculations.

Purchases

Inventory items acquired during the period, added to beginning inventory to determine goods available for sale.

Physical Flow of Goods

Actual movement of inventory items, which may differ from the cost flow assumption used in accounting records.

Cost per Unit

Average amount paid for each inventory item, calculated by dividing total cost by total units purchased.

Inventory Count

Physical process of tallying remaining inventory items at the end of the period to determine ending inventory.

Identical Units

Inventory items that are indistinguishable from each other, making cost assignment dependent on accounting methods.

Financial Records

Documentation and reports tracking inventory values, purchases, and cost of goods sold for accounting purposes.

BackBack

BackBack

06:32

06:32