What is the main purpose of using FIFO, LIFO, and Average Cost methods in a periodic inventory system?

These methods are used to assign costs to goods sold and ending inventory when tracking identical units, especially when purchase prices change over time.

How does the FIFO (First In, First Out) method determine the cost of goods sold in a periodic inventory system?

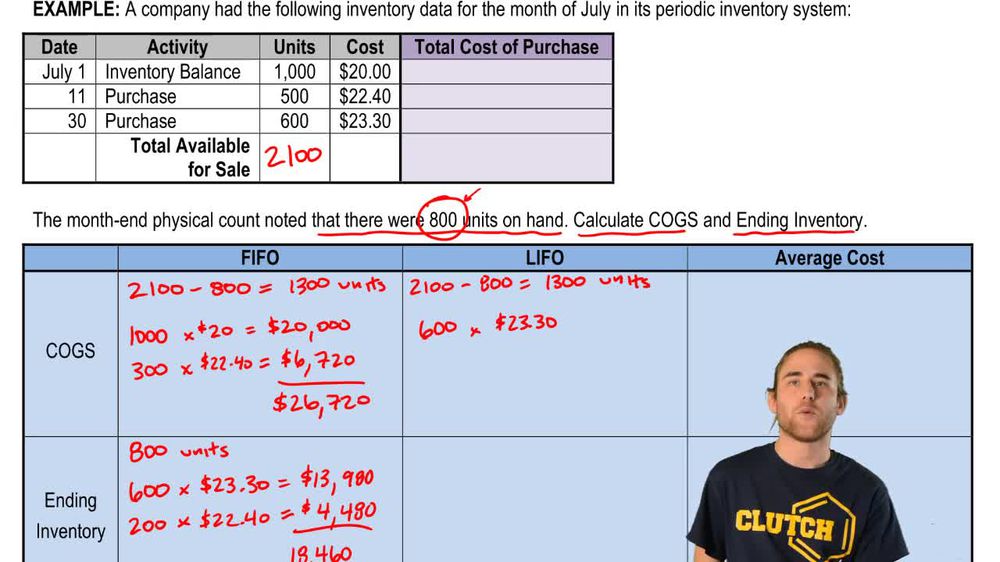

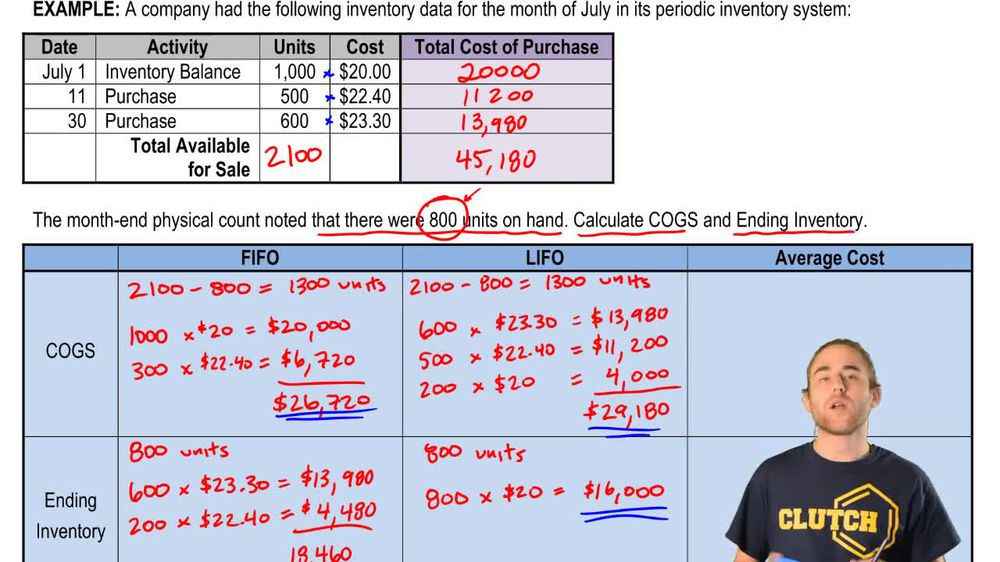

FIFO assumes the oldest inventory items are sold first, so the cost of goods sold reflects the cost of the earliest purchased units.

How does the LIFO (Last In, First Out) method determine the cost of goods sold in a periodic inventory system?

LIFO assumes the newest inventory items are sold first, so the cost of goods sold reflects the cost of the most recently purchased units.

How is the Average Cost method calculated in a periodic inventory system?

The Average Cost method divides the total cost of all units available for sale by the total number of units, resulting in a weighted average cost per unit.

What does 'goods available for sale' mean in the context of periodic inventory?

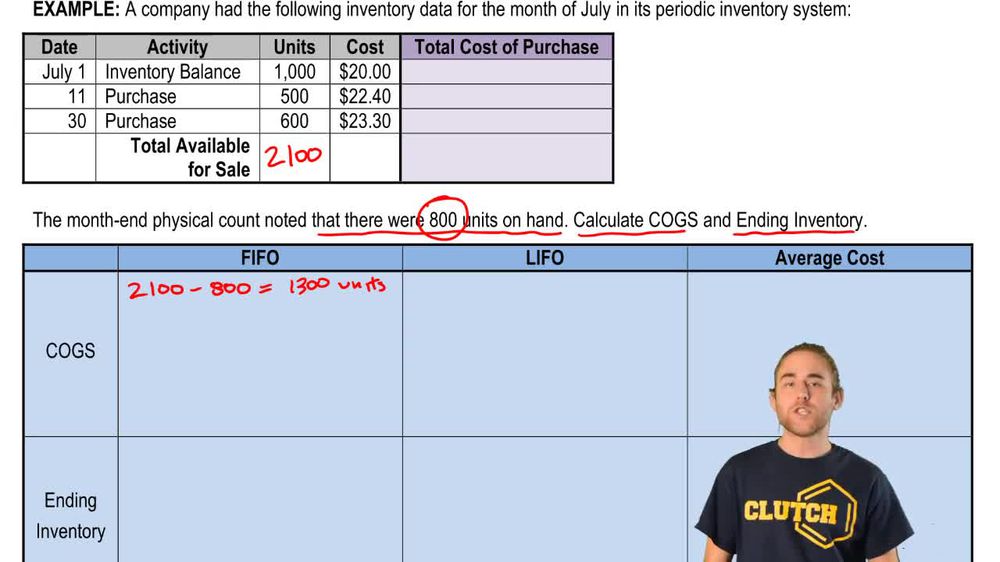

'Goods available for sale' refers to the sum of beginning inventory and all purchases made during the period.

In a periodic inventory system, when is the cost of goods sold determined?

The cost of goods sold is determined at the end of the period, after a physical count of ending inventory.

Does the cost flow assumption (FIFO, LIFO, or Average Cost) have to match the physical flow of goods?

No, the cost flow assumption does not need to match the actual physical flow of goods; it is used for accounting purposes.

Why are cost flow assumptions like FIFO and LIFO important when purchase prices change over time?

They help assign costs to inventory and cost of goods sold when identical units are purchased at different prices.

What is the formula for calculating goods available for sale?

Goods available for sale = Beginning Inventory + Purchases during the period.

How is ending inventory determined in a periodic inventory system?

Ending inventory is determined by physically counting the remaining inventory at the end of the period.

What happens to goods available for sale by the end of the period?

Goods available for sale are either sold (becoming cost of goods sold) or remain as ending inventory.

How does the periodic inventory system differ from the perpetual inventory system in recording cost of goods sold?

In a periodic system, cost of goods sold is recorded only at the end of the period, not after each sale as in a perpetual system.

Why might a company choose to use FIFO over LIFO or vice versa?

A company might choose FIFO or LIFO based on financial reporting preferences, tax implications, or to better match costs with revenues.

What is the impact of using FIFO during periods of rising prices?

FIFO results in lower cost of goods sold and higher ending inventory values, potentially increasing reported profits.

What is the impact of using LIFO during periods of rising prices?

LIFO results in higher cost of goods sold and lower ending inventory values, potentially reducing reported profits and taxes.

How do you calculate the average cost per unit in the Average Cost method?

Divide the total cost of goods available for sale by the total number of units available for sale.

Can a company physically sell its oldest inventory while using the LIFO method for accounting?

Yes, the physical flow of goods does not have to match the cost flow assumption used for accounting.

What is the main difference between FIFO and LIFO in terms of which inventory costs are assigned to cost of goods sold?

FIFO assigns the oldest costs to cost of goods sold, while LIFO assigns the newest costs.

Why is a physical inventory count necessary in a periodic inventory system?

A physical count is needed to determine the actual quantity of ending inventory, as inventory records are not updated continuously.

Back

Back

06:32

06:32