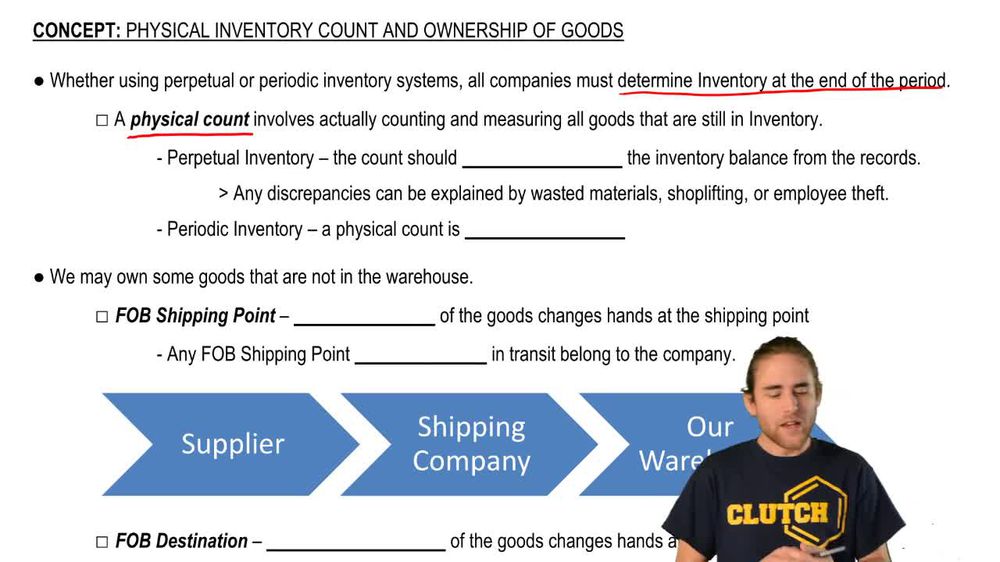

Why must companies perform a physical inventory count at the end of the accounting period, even if they use a perpetual inventory system?

A physical inventory count is required to confirm or adjust the recorded inventory balance, as discrepancies may arise due to theft, loss, or errors.

How does a physical inventory count differ in a periodic inventory system compared to a perpetual system?

In a periodic system, the physical count is necessary to determine ending inventory and calculate cost of goods sold, while in a perpetual system, it serves to verify the continuously updated records.

What does FOB Shipping Point mean regarding the ownership of goods in transit?

FOB Shipping Point means ownership transfers to the buyer at the shipping point, so goods in transit should be included in the buyer's inventory.

When should goods shipped FOB Destination be included in the buyer's inventory?

Goods shipped FOB Destination are included in the buyer's inventory only after they arrive at the buyer's location, as ownership transfers upon delivery.

If a company sells goods FOB Destination and the goods are still in transit at year-end, who owns the goods?

The seller still owns the goods while they are in transit under FOB Destination terms, so they remain in the seller's inventory until delivery.

How should a company determine if goods in transit at year-end should be included in its inventory?

The company should assess the shipping terms (FOB Shipping Point or FOB Destination) to determine if it owns the goods during transit and include them in inventory accordingly.

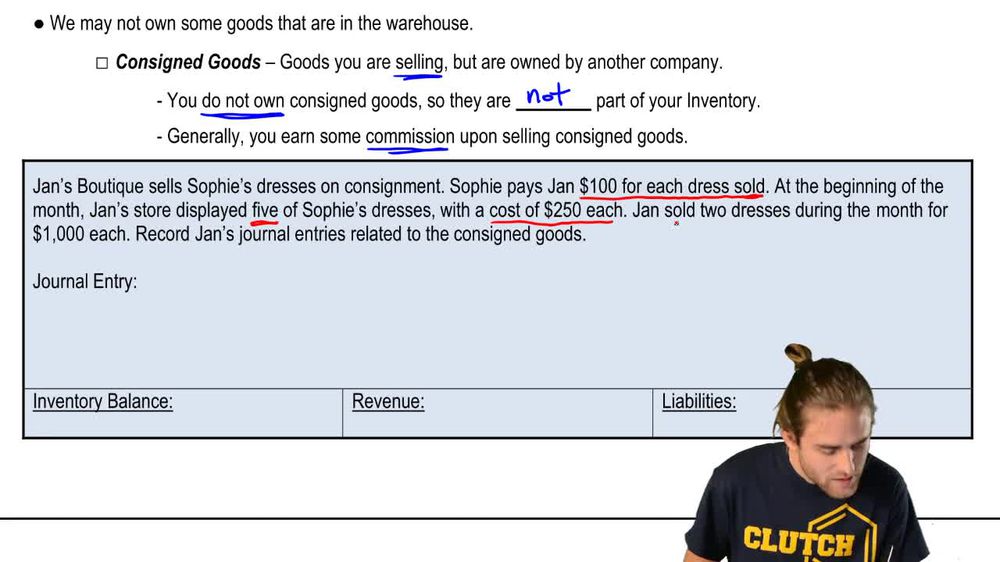

What are consigned goods, and who includes them in their inventory?

Consigned goods are items held and sold by one party (the consignee) on behalf of another (the consignor); only the consignor includes them in inventory, not the consignee.

How does a consignee record revenue from selling consigned goods?

The consignee records revenue only for the commission earned on sales, not for the total sales amount of the consigned goods.

What journal entry does a consignee make when selling consigned goods?

The consignee debits cash for the total received, credits commission revenue for the earned commission, and credits a liability for the amount owed to the consignor.

If a store sells consigned goods, should the value of those goods be included in the store's inventory balance?

No, consigned goods should not be included in the store's inventory balance because the store does not own them.

What liability does a consignee recognize after selling consigned goods?

The consignee recognizes a liability for the amount owed to the consignor, which is the sales proceeds minus the commission earned.

Why is it important to correctly determine ownership of goods at the end of an accounting period?

Correctly determining ownership ensures accurate inventory reporting and financial statements, preventing overstatement or understatement of assets and liabilities.

What is the purpose of taking a physical count of inventory at the end of an accounting period?

The purpose of taking a physical count of inventory at the end of an accounting period is to confirm or adjust the recorded inventory balance, ensuring the amount reported on the balance sheet accurately reflects the inventory actually on hand.

How is a physical inventory count performed, and why is it necessary in both perpetual and periodic inventory systems?

A physical inventory count is performed by physically counting, measuring, or weighing goods in the warehouse. It is necessary in both perpetual and periodic systems to verify the actual inventory on hand and reconcile any discrepancies with accounting records.

What is typically the first step in inventory management for a company?

The first step in inventory management is determining the amount of inventory on hand, which is usually done by performing a physical count of inventory.

What common events can result in inventory shrinkage for a company?

Common events that can result in inventory shrinkage include waste, shoplifting, and employee theft.

Which types of goods should not be included in a company's inventory balance?

Consigned goods should not be included in a company's inventory balance because they are owned by the consignor, not the consignee.

How do FOB shipping point and FOB destination terms affect the ownership and inclusion of goods in inventory during transit?

Under FOB shipping point, ownership transfers to the buyer at the shipping point, so goods in transit are included in the buyer's inventory. Under FOB destination, ownership transfers upon delivery, so goods in transit remain in the seller's inventory until they reach the destination.

Back

Back

03:56

03:56