Skip to main content

Financial Accounting

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Service Company vs. Merchandising Company definitions

You can tap to flip the card.

Service Company

You can tap to flip the card.

👆

Service Company

Business model focused on providing intangible services to customers, with revenue recognized upon completion of the service.

Track progress

Control buttons has been changed to "navigation" mode.

1/15

Related flashcards

Related practice

Recommended videos

Service Company vs. Merchandising Company quiz #1

Service Company vs. Merchandising Company

28 Terms

Service Company vs. Merchandising Company

4. Merchandising Operations

10 problems

Topic

Net Sales

4. Merchandising Operations

10 problems

Topic

4. Merchandising Operations

14 topics

14 problems

Chapter

Guided course

07:01

Merchandising Company

2220

views

122

rank

Guided course

03:43

Service Company

3152

views

77

rank

Terms in this set (15)

Hide definitions

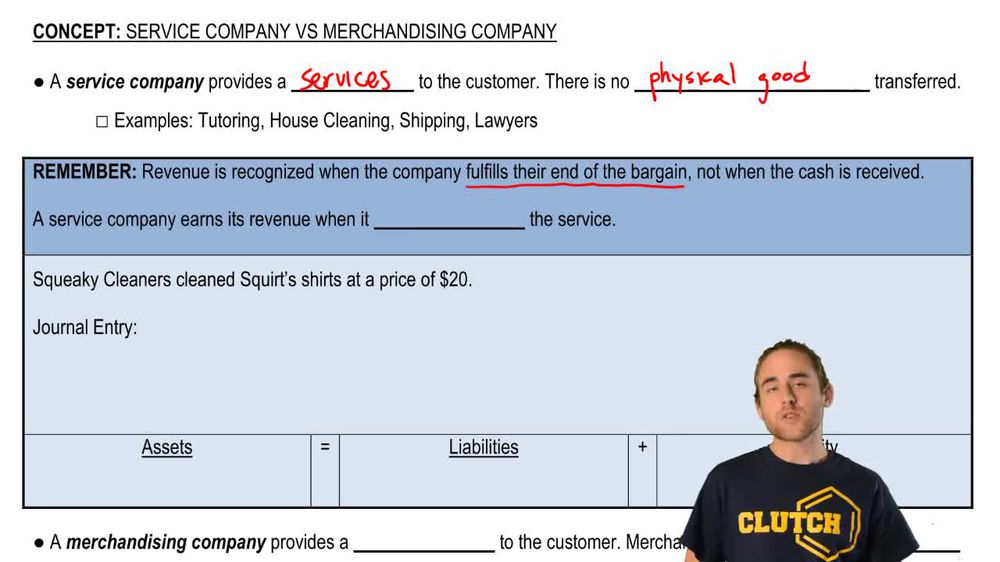

Service Company

Business model focused on providing intangible services to customers, with revenue recognized upon completion of the service.

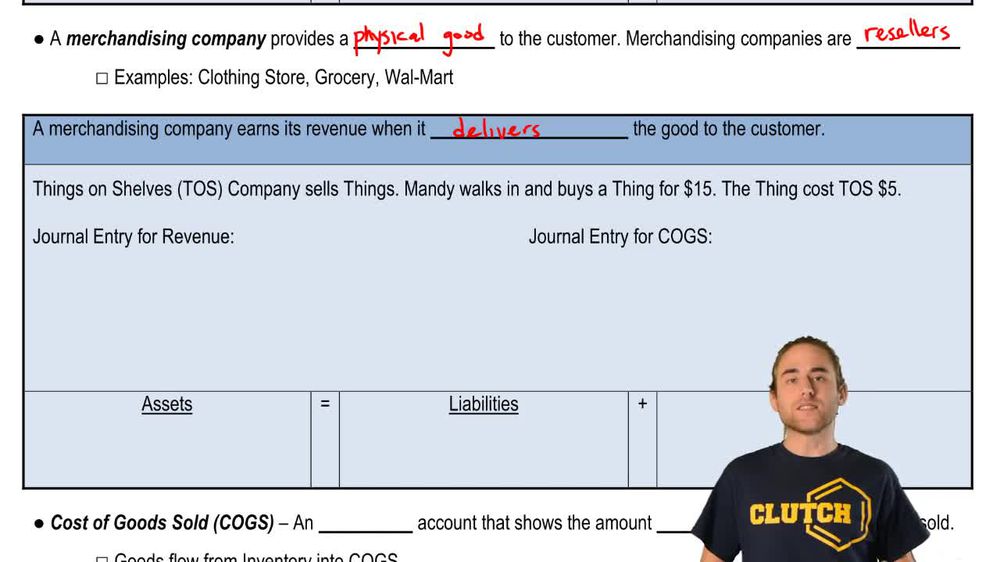

Merchandising Company

Business that resells tangible goods purchased from suppliers, earning revenue when goods are delivered to customers.

Intangible Service

Non-physical benefit provided to customers, such as tutoring or cleaning, with no transfer of physical goods.

Tangible Good

Physical item transferred from seller to buyer, forming the basis of sales in merchandising companies.

Revenue Recognition Principle

Accounting guideline requiring revenue to be recorded when a company fulfills its performance obligation, not when cash is received.

Journal Entry

Formal accounting record documenting the financial impact of business transactions, affecting accounts like revenue or inventory.

Accounts Receivable

Asset account representing amounts owed by customers for services or goods delivered on credit.

Service Revenue

Income earned from providing services, recorded when the service is completed, regardless of payment timing.

Sales Revenue

Income generated from selling goods, recognized when goods are delivered to the customer.

Cost of Goods Sold

Expense account reflecting the direct cost incurred by a merchandising company to acquire goods sold to customers.

Inventory

Current asset account representing goods held for resale by a merchandising company.

Matching Principle

Accounting concept requiring expenses to be recorded in the same period as the related revenues to accurately reflect profitability.

Asset

Resource owned by a company, such as cash, inventory, or accounts receivable, providing future economic benefit.

Equity

Owner's residual interest in the assets of a company after deducting liabilities, increased by revenues and decreased by expenses.

Expense

Outflow or using up of assets as part of operations, such as cost of goods sold in merchandising companies.

BackBack

BackBack

07:01

07:01