What is the specific identification method in inventory valuation, and when is it most appropriately used?

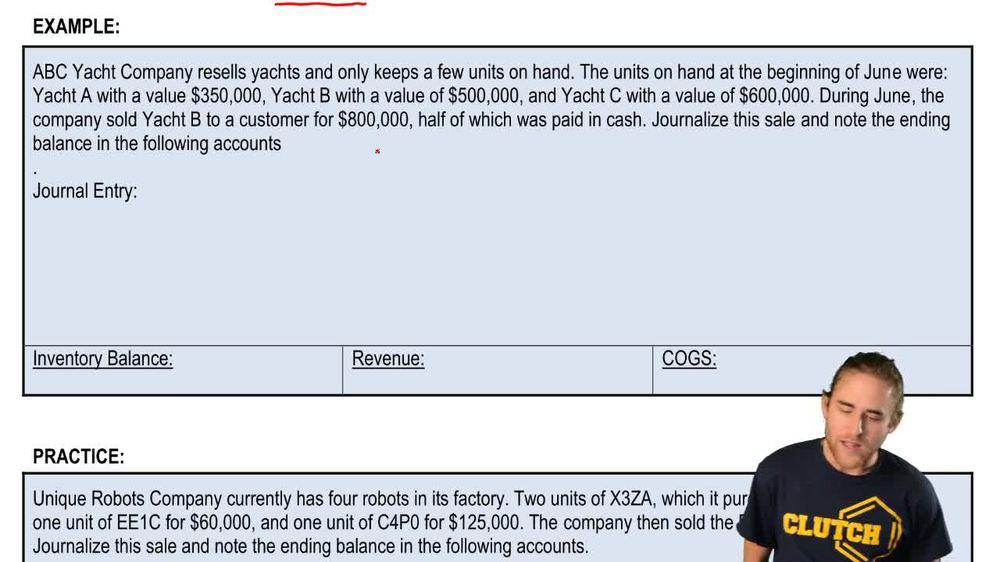

The specific identification method tracks the actual cost of each unique or easily identifiable inventory item sold and remaining. It is most appropriate for businesses dealing with high-value, distinguishable items, such as yachts or custom goods.

Back

Back

04:47

04:47