Back

BackFinancial Accounting Key Concepts and Formulas

02:47

02:47

Terms in this set (27)

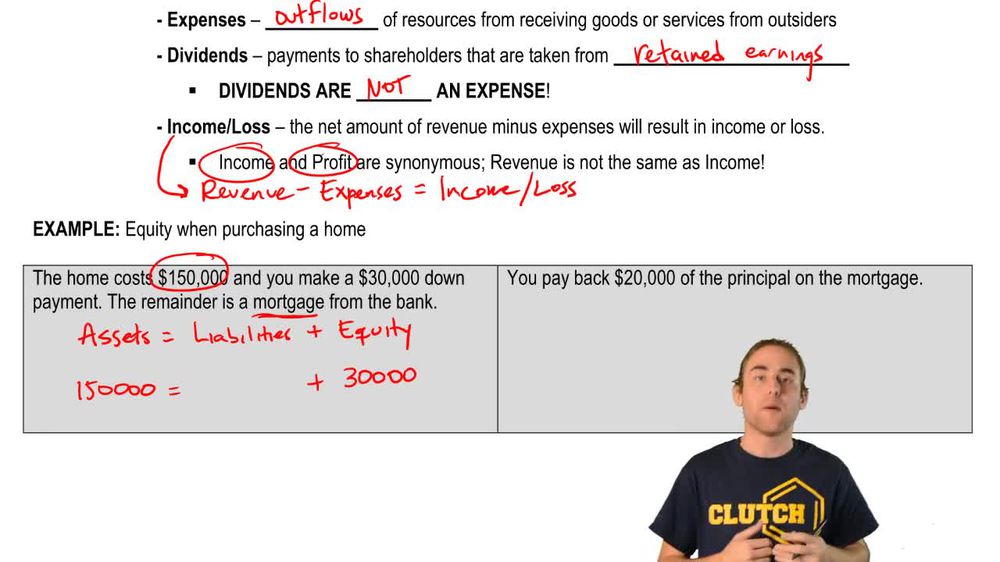

Assets = Liabilities + Shareholders' Equity

Working Capital = Current Assets − Current Liabilities

Indicates short-term liquidity.

Cash, Accounts Receivable, Inventory, Prepaid Expenses expected to convert to cash or be used within 1 year.

A contra-asset below Accounts Receivable showing net realizable value; estimates receivables not collectible.

Intangible asset created when acquiring a company for more than fair value of net assets; not amortized but tested annually for impairment.

Groups all revenues and expenses separately; one subtraction to get Net Income; simple but limited analysis.

Shows multiple subtotals: Gross Profit, Operating Income, EBT, Net Income; separates operating from non-operating items.

Gross Profit = Net Revenue − Cost of Goods Sold (COGS)

Operating Income = Gross Profit − Operating Expenses (SG&A, D&A, R&D)

Annual SEC report with comprehensive, audited financial statements.

Quarterly SEC report with condensed, unaudited financial statements.

SEC report filed as needed to disclose material events like mergers or CEO changes.

Unqualified (clean), Qualified, Adverse, Disclaimer of Opinion.

SEC has legal authority over public company accounting; FASB sets U.S. GAAP standards.

Basic EPS = (Net Income − Preferred Dividends) ÷ Weighted Avg. Common Shares

EPS including potentially dilutive securities; always less than or equal to Basic EPS.

Operating Cash Flow ≥ Net Income, low accruals, no sudden policy changes, no large unusual items, unqualified audit opinion.

Unrealized gains/losses on AFS securities, foreign currency translation, pension adjustments, cash flow hedges.

Non-cash expense reducing Net Income but added back in cash flow statement (indirect method).

Operating (day-to-day), Investing (long-term assets), Financing (debt and equity transactions).

Starts with Net Income, adjusts for non-cash items and working capital changes.

Current Assets decrease → Cash increases; Current Assets increase → Cash decreases.

Current Liabilities increase → Cash increases; Current Liabilities decrease → Cash decreases.

Each line item ÷ Total Assets × 100 to compare companies and track changes.

Each line item ÷ Net Revenue × 100 to analyze cost structure and margins.

Net Revenue → Gross Profit → Operating Income (EBIT) → Income Before Taxes (EBT) → Net Income.

Filed before shareholder meetings to inform voting on executive compensation, board nominees, and proposals.