Back

BackFinancial Accounting: Receivables and Revenue Recognition

08:00

08:00Terms in this set (23)

Revenue is recognized when earned, meaning goods are delivered or services performed, and recorded at the amount of cash received or fair market value of assets received.

Identify the contract, identify performance obligations, determine transaction price, allocate price to obligations, recognize revenue when obligations are satisfied.

Ownership and revenue recognition occur when goods leave the shipping dock.

Ownership and revenue recognition occur when goods are delivered to the customer.

A sales discount is a percentage reduction if customers pay early, e.g., 2/10, n/30 means 2% discount if paid within 10 days, otherwise full payment in 30 days.

A document authorizing a credit to the customer’s accounts receivable for returned or unsatisfactory goods.

Based on historical return rates, companies estimate returns and adjust sales revenue and inventory accordingly.

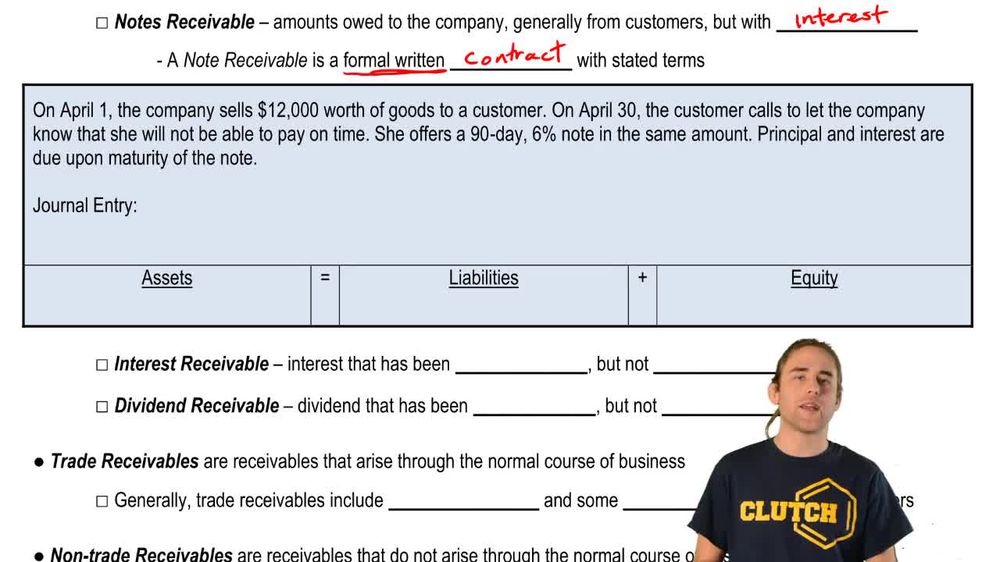

Monetary claims against others, usually current assets, acquired by selling goods/services (accounts receivable) or lending money (notes receivable).

A contra account to accounts receivable showing the estimated amount not expected to be collected.

Reported on the income statement as an expense reflecting estimated uncollectible accounts.

Estimates bad debt expense based on past experience and records an allowance contra account to accounts receivable.

Percent-of-sales method (income statement approach) and aging-of-receivables method (balance sheet approach).

Calculates bad debt expense as a percentage of total sales revenue to match expense with revenue.

Analyzes accounts receivable by age to estimate the allowance needed for uncollectible accounts.

The amount expected to be collected, calculated as accounts receivable minus allowance for bad debts.

Records bad debt expense only when a specific account is deemed uncollectible; not GAAP compliant and may overstate assets.

A written promise to pay a specified amount of money at a certain date, involving a creditor (lender) and debtor (borrower).

Interest = Principal × Rate × Time (fraction of year), with rates usually annual and time expressed in months/12 or days/365.

A liquidity ratio measuring ability to pay current liabilities without selling inventory; benchmark is 1:1.

Number of times a company collects its average accounts receivable in a year; higher turnover means faster collection.

The average number of days it takes to collect accounts receivable; lower DSO indicates quicker collection.

Summarizes receivables by age categories to estimate collectibility and required allowance for bad debts.

To summarize and organize large data sets, such as unpaid invoices, for better analysis of receivables collectibility.