Back

BackMacroeconomics: Economic Efficiency, Government Price Setting, and Taxes

03:39

03:39

Terms in this set (20)

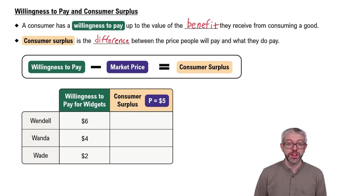

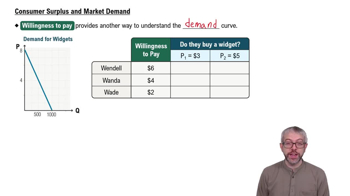

Consumer surplus is the difference between the highest price a consumer is willing to pay for a good or service and the actual price the consumer pays.

Producer surplus is the difference between the lowest price a firm would accept for a good or service and the price it actually receives.

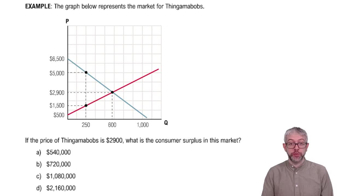

Consumer surplus is the area below the demand curve and above the price that consumers pay.

Producer surplus is the area above the supply curve and below the market price.

The marginal cost of producing that good or service determines the lowest price a firm would accept.

Economic efficiency occurs when the marginal benefit to consumers of the last unit produced equals its marginal cost of production, maximizing the sum of consumer and producer surplus.

There is a deadweight loss, which is a reduction in economic surplus and represents inefficiency in the market.

A price ceiling is a legally determined maximum price that sellers may charge for a good or service.

A price floor is a legally determined minimum price that sellers may receive for a good or service.

Examples include minimum wages (price floor), rent controls (price ceiling), and agricultural price supports (price floor).

It causes a surplus (excess supply), reduces quantity traded, transfers surplus from consumers to producers, and creates deadweight loss.

It causes a shortage (excess demand), reduces quantity traded, transfers surplus from producers to consumers, and creates deadweight loss.

Tax incidence is the actual division of the burden of a tax between buyers and sellers in a market, regardless of who legally pays the tax.

The relative slopes of the demand and supply curves determine tax incidence; steeper curves bear more of the tax burden.

A per-unit tax shifts the supply curve upward by the amount of the tax, increasing the price paid by consumers and decreasing the price received by producers.

Deadweight loss is the reduction in economic surplus caused by the tax, representing inefficiency due to decreased quantity traded.

The excess burden is the deadweight loss from a tax, reflecting the inefficiency relative to the tax revenue raised.

By estimating the demand curve and knowing the price, economists calculate the area below the demand curve and above the price to find consumer surplus.

Marginal cost is the change in a firm's total cost from producing one more unit of a good or service.

At competitive equilibrium, marginal benefit equals marginal cost, maximizing economic surplus and ensuring economic efficiency.