Back

BackA Further Look at Financial Statements: Structure, Elements, and Liquidity Analysis

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 2: A Further Look at Financial Statements

Learning Objectives

Construct the three primary financial statements: the Statement of Income, the Statement of Changes in Shareholders’ Equity, and the Statement of Financial Position.

Understand the relationships among these statements.

Calculate and interpret liquidity ratios.

Comprehend the framework for the preparation and presentation of financial statements.

The Statement of Income

Purpose and Structure

The Statement of Income (or Income Statement) measures a company’s operational performance over a specific period (monthly, quarterly, or annually). It summarizes revenues and expenses to determine net income or net loss.

Revenues: Income from the sale of goods or services during the period. Classified as principal (e.g., sales revenue) or other (e.g., rent, interest revenue).

Expenses: Costs incurred to generate revenues. Classified as principal (e.g., cost of goods sold, operating expenses) or other (e.g., interest expense, income tax expense).

Net Income: The difference between total revenues and total expenses.

Format:

Name of Company

Name of Statement

Date (e.g., For the year ended…)

Revenues – Expenses = Net Income (or Net Loss)

Example: If a company earns $100,000 in revenues and incurs $70,000 in expenses, net income is $30,000.

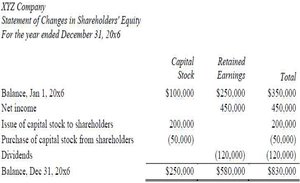

Statement of Changes in Shareholders’ Equity

Purpose and Structure

The Statement of Changes in Shareholders’ Equity reconciles each equity account from the beginning to the end of the period. It shows how net income, dividends, and share transactions affect equity.

Share Capital: Investments made by shareholders. Increases with new share issues, decreases with share repurchases.

Retained Earnings: Accumulated net income not distributed as dividends since inception.

Format: The statement lists opening balances, adds net income, adjusts for share transactions and dividends, and presents closing balances.

Example: If a company starts with $100,000 in share capital and $250,000 in retained earnings, earns $450,000 net income, issues $200,000 in new shares, repurchases $60,000 in shares, and pays $120,000 in dividends, the closing balances are $250,000 (share capital) and $580,000 (retained earnings).

Statement of Financial Position

Purpose and Structure

The Statement of Financial Position (or Balance Sheet) provides a snapshot of a company’s financial position at a specific date. It lists assets, liabilities, and shareholders’ equity, following the accounting equation:

Assets: Economic resources controlled by the company.

Liabilities: Economic obligations to creditors.

Shareholders’ Equity: Residual interest in assets after deducting liabilities.

Assets

Current Assets: Expected to be used, sold, or converted to cash within one year or operating cycle (e.g., cash, short-term investments, accounts receivable, inventory, prepaid expenses).

Noncurrent Assets: Used or converted to cash over periods longer than one year (e.g., property, plant & equipment, intangible assets, long-term investments).

Liabilities

Current Liabilities: Due within one year or operating cycle (e.g., accounts payable, taxes payable, salaries payable, dividends payable, unearned revenue).

Noncurrent Liabilities: Due beyond one year (e.g., bonds payable, long-term notes payable).

Shareholders’ Equity

Share Capital: Amounts invested by shareholders.

Retained Earnings: Cumulative net income not distributed as dividends.

Summary: The statement lists accounts under the correct categories and ensures total assets equal total liabilities plus shareholders’ equity.

Relationships Among the Financial Statements

The three statements are interrelated:

Net income from the Statement of Income is used in the Statement of Changes in Shareholders’ Equity.

Ending balances from the Statement of Changes in Shareholders’ Equity are reported in the Statement of Financial Position.

Business Models and Financial Statements

Manufacturing-sector companies: Produce tangible goods from raw materials.

Service-sector companies: Provide intangible products or services (e.g., audit, legal services).

Merchandising-sector companies: Sell tangible products purchased in finished form (e.g., retailers, wholesalers).

Liquidity Analysis and Ratios

Purpose

Liquidity ratios assess a company’s ability to meet short-term obligations. Key ratios include working capital, current ratio, and quick ratio.

Working Capital

Measures the difference between current assets and current liabilities:

Current Ratio

Indicates the ability to cover current liabilities with current assets:

Quick Ratio (Acid-Test Ratio)

Measures the ability to meet short-term obligations with the most liquid assets:

Example: Home Depot vs. Lowe’s (2023)

Home Depot | Lowe’s | |

|---|---|---|

Current Assets | $29,775 million | $19,071 million |

Current Liabilities | $22,015 million | $15,568 million |

Working Capital | $7,760 million | $3,503 million |

Current Ratio | 1.35 | 1.23 |

Quick Ratio | 0.32 | 0.08 |

Interpretation: Home Depot has higher liquidity than Lowe’s, as indicated by its higher working capital, current ratio, and quick ratio.

Where to Find Financial Statements

Canadian public companies: SEDAR

US public companies: EDGAR

Company websites (Investor Relations section)

Summary Table: Key Elements of Financial Statements

Statement | Main Purpose | Key Elements |

|---|---|---|

Statement of Income | Measures operational performance over a period | Revenues, Expenses, Net Income |

Statement of Changes in Shareholders’ Equity | Reconciles equity accounts from beginning to end of period | Share Capital, Retained Earnings, Dividends |

Statement of Financial Position | Snapshot of financial position at a point in time | Assets, Liabilities, Shareholders’ Equity |

Additional info: The framework for the preparation and presentation of financial statements is covered as self-study and is based on generally accepted accounting principles (GAAP) or International Financial Reporting Standards (IFRS), depending on jurisdiction.