Back

BackAccounting Inventories: Concepts, Methods, and Financial Implications

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accounting Inventories

Merchandising Company vs. Manufacturing Company

Understanding the distinction between merchandising and manufacturing companies is essential for inventory accounting. Each type of company manages inventory differently based on its operations.

Merchandising Company: Maintains a single Inventory account, often called Merchandise Inventory. Merchandisers purchase finished goods from suppliers and resell them without further processing.

Manufacturing Company: Maintains three inventory accounts:

Raw Materials Inventory: Inputs acquired from suppliers for production.

Work-in-Process Inventory: Goods currently in production but not yet complete.

Finished Goods Inventory: Completed products ready for sale.

Example: XYZ Company purchases goods from its supplier for $10,000 on account. The journal entry would debit Inventory and credit Accounts Payable.

Physical Inventory Count and Ownership of Goods

Regardless of the inventory system used, companies must determine the actual inventory on hand at period-end through a physical count. Ownership of goods is determined by shipping terms and consignment arrangements.

Physical Count: Involves counting and measuring all goods in inventory.

Perpetual Inventory System: The physical count should match the recorded inventory balance. Discrepancies may indicate waste, theft, or errors.

Periodic Inventory System: The physical count is essential to determine ending inventory and cost of goods sold (COGS).

Ownership of Goods:

FOB Shipping Point: Ownership transfers at the shipping point; goods in transit belong to the buyer.

FOB Destination: Ownership transfers at the destination; goods in transit belong to the seller.

Consigned Goods: Goods held for sale but owned by another company. Consigned goods are not included in the consignee's inventory.

Example: Jan’s Boutique sells Sophie’s dresses on consignment. Jan does not record the dresses as inventory but earns a commission upon sale.

Specific Identification Method

The specific identification method assigns actual costs to each unit sold and each unit remaining in inventory. This method is suitable for unique or high-value items.

COGS: The actual cost of each unit sold is recorded as cost of goods sold.

Ending Inventory: The actual cost of each unsold unit is recorded as inventory.

Example: ABC Yacht Company tracks the cost of each yacht individually. When Yacht B is sold, its specific cost is recorded as COGS.

Periodic System – FIFO, LIFO, and Average Cost

When dealing with large quantities of similar items, companies use cost flow assumptions to allocate costs between COGS and ending inventory.

First In, First Out (FIFO): The earliest goods purchased are the first to be sold. COGS reflects older costs; ending inventory reflects recent costs.

Last In, First Out (LIFO): The most recently purchased goods are the first to be sold. COGS reflects recent costs; ending inventory reflects older costs.

Average Cost: Goods are sold at the average cost of all units available for sale.

Key Formulas:

Average Cost per Unit: \text{Average Cost} = \frac{\text{Total Cost}}{\text{Quantity}} $ $

Goods Available for Sale: \text{Beginning Inventory} + \text{Purchases} = \text{Goods Available for Sale} $ $

Ending Inventory: \text{Beginning Inventory} + \text{Purchases} - \text{COGS} = \text{Ending Inventory} $ $

Example: A company with periodic inventory must calculate COGS and ending inventory using each method based on units sold and remaining.

Perpetual System – FIFO, LIFO, and Average Cost

In a perpetual inventory system, inventory records are updated continuously after each purchase or sale. Cost flow assumptions are applied in real-time.

FIFO: The oldest costs are assigned to COGS as sales occur.

LIFO: The most recent costs are assigned to COGS as sales occur.

Moving Average Cost: The average cost per unit is recalculated after each purchase.

Key Formula:

Moving Average Cost: \text{Average Cost} = \frac{\text{Total Cost}}{\text{Quantity}} $ $

Example: A company tracks inventory balances and COGS after each transaction using the chosen cost flow method.

Financial Statement Effects of Costing Methods

The choice of inventory costing method affects key financial statement figures, especially in periods of changing prices.

COGS: Varies depending on the method, affecting gross profit and net income.

Gross Profit: Calculated as Sales Revenue minus COGS.

Net Income: Calculated as Gross Profit minus other expenses/revenues.

Ending Inventory: Calculated as Beginning Inventory plus Purchases minus COGS.

Rising Price Environment:

FIFO: Lower COGS, higher gross profit, higher net income, higher ending inventory.

LIFO: Higher COGS, lower gross profit, lower net income, lower ending inventory.

Falling Price Environment:

FIFO: Higher COGS, lower gross profit, lower net income, lower ending inventory.

LIFO: Lower COGS, higher gross profit, higher net income, higher ending inventory.

Companies using LIFO must disclose the value of inventory under FIFO using a LIFO reserve.

Lower of Cost or Market (LCM)

The LCM rule is an application of the conservatism principle, ensuring that inventory is not overstated on the balance sheet.

Cost: The historical cost paid for inventory.

Market: The current replacement cost or net realizable value (estimated selling price minus disposal costs).

LCM Rule: Inventory is reported at the lower of its cost or market value.

Net Realizable Value Formula: \text{Net Realizable Value} = \text{Estimated Selling Price} - \text{Disposal Costs} $ $

If inventory is written down, a loss is recognized in the period.

Example: If inventory cost is $84,000, estimated selling price is $86,000, and disposal costs are $7,000, the net realizable value is $79,000. Inventory should be reported at the lower of cost ($84,000) or market ($79,000), so $79,000.

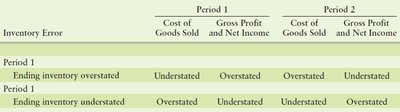

Inventory Errors

Inventory errors affect the calculation of COGS, gross profit, net income, and balance sheet values. These errors typically self-correct after two periods.

Ending Inventory Overstated: COGS understated, gross profit and net income overstated in the current period; the opposite effect in the next period.

Ending Inventory Understated: COGS overstated, gross profit and net income understated in the current period; the opposite effect in the next period.

Balance Sheet Effects: Overstated ending inventory leads to overstated assets and equity; understated inventory leads to understated assets and equity.

Example: If ending inventory is overstated by $5,000, both assets and equity are overstated on the balance sheet.

Inventory Error | Period 1 | Period 2 | ||

|---|---|---|---|---|

Cost of Goods Sold | Gross Profit and Net Income | Cost of Goods Sold | Gross Profit and Net Income | |

Ending inventory overstated | Understated | Overstated | Overstated | Understated |

Ending inventory understated | Overstated | Understated | Understated | Overstated |

Additional info: Inventory errors are a common source of misstatements in financial reporting and are corrected automatically in the following period due to the nature of inventory accounting.