Back

BackAccounts Receivable: Recognition, Measurement, and Earnings Management

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accounts Receivable

Introduction to Accounts Receivable

Accounts Receivable (A/R) represent amounts owed to a business by its customers for goods or services delivered on credit. These transactions are common in business-to-business sales and are recorded as assets on the balance sheet. Revenue is recognized at the time of sale, even if cash has not yet been received, and an A/R is established to reflect the promise of future payment.

Definition: Accounts Receivable are current assets representing amounts due from customers for credit sales.

Recognition: Revenue is credited and A/R is debited at the time of sale.

Risk: There is a risk that some customers may default and not pay their debts.

Accounting for Accounts Receivable

When goods are sold on credit, the following journal entries are made:

To record credit sales:

To record cash collections:

Allowance for Doubtful Accounts

Because not all receivables will be collected, companies must estimate and account for potential bad debts. This is done using the Allowance for Doubtful Accounts (AFDA), a contra-asset account that reduces the gross amount of A/R to its net realizable value.

Purpose: To estimate and match bad debt expense to the period in which the related sales are recognized (matching principle).

Journal Entry:

Net Realizable Value:

Analogy: Similar to how accumulated depreciation reduces the carrying value of PPE.

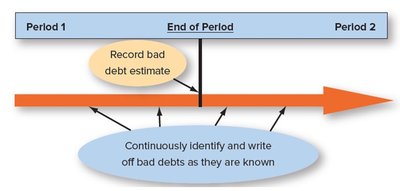

Write-off of Uncollectible Accounts

When a specific account is determined to be uncollectible, it is written off against the allowance. This does not affect the income statement, as the expense was already recognized.

Journal Entry for Write-off:

Effect: Reduces both A/R and AFDA, leaving net A/R unchanged.

Reversing Write-offs

If a previously written-off account is later collected, the write-off is reversed and the cash is recorded:

Reinstatement:

Collection:

Estimating Bad Debt Expense

Income Statement (I/S) Approach

Bad debt expense is estimated as a percentage of total credit sales for the period. This method focuses on matching expenses to the period's sales.

Formula:

Effect: Increases AFDA and reduces net income for the period.

Balance Sheet (B/S) Approach

Bad debt expense is estimated based on the ending balance of A/R, often using an aging schedule that applies different percentages to receivables based on their age.

Steps:

Estimate required ending balance in AFDA as a percentage of A/R (gross), often using aging analysis.

Calculate bad debt expense as a plug:

Aging of Receivables

Receivables are categorized by age, and higher percentages are applied to older accounts to estimate uncollectibles more accurately.

Example Table:

Days Past Due | Balance | Estimated Default Rate |

|---|---|---|

Current | 3,200 | 1% |

0-60 | 300 | 12% |

Beyond 60 | 50 | 50% |

Total | 3,550 | - |

Accounts Receivable Analysis

Key Ratios

Accounts Receivable Turnover: Measures how efficiently a company collects its receivables.

Average Collection Period (Days Sales Outstanding, DSO): Indicates the average number of days it takes to collect receivables.

A lower DSO or higher turnover indicates faster collection, which is generally favorable for liquidity and cash management.

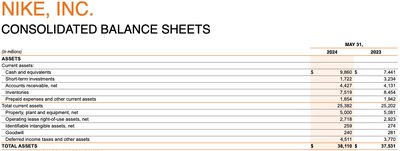

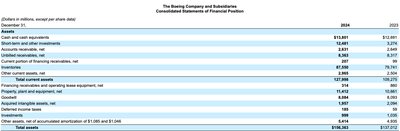

Financial Statement Examples

Companies report A/R and related allowances on their balance sheets. For example, see the following extracts:

Earnings Management and Accounts Receivable

Allowance for Doubtful Accounts and Earnings Management

The estimation of AFDA is subject to management judgment. Underestimating the allowance can inflate current period income, while overestimating can shift income to future periods. This discretion can be used for earnings management.

Earnings Management: The use of judgment in financial reporting to alter financial results, potentially misleading stakeholders or influencing contractual outcomes.

Methods:

Real Earnings Management (REM): Changing actual business activities (e.g., offering discounts, delaying expenses).

Accrual Earnings Management (AEM): Manipulating accruals (e.g., revenue recognition, underprovisioning for bad debts).

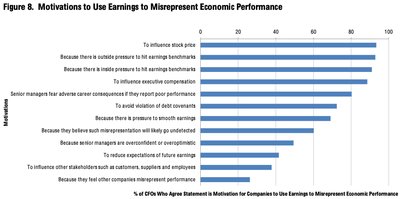

Motivations for Earnings Management

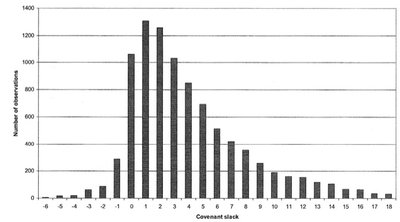

Managers may be motivated to manage earnings to influence stock price, meet benchmarks, or avoid debt covenant violations.

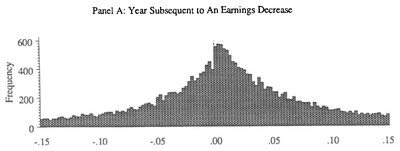

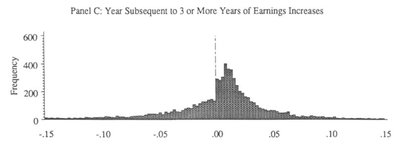

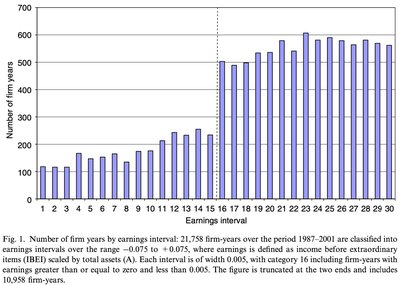

Empirical Evidence of Earnings Management

Research shows patterns in earnings distributions and behaviors around benchmarks and covenants.

Summary

Accounts Receivable are reported at net realizable value, reflecting expected collectibility.

GAAP and IFRS require estimation of bad debts using the Allowance for Doubtful Accounts.

Bad debt expense can be estimated using the I/S or B/S approach.

Discretion in estimating AFDA can be used for earnings management, affecting reported income across periods.