Back

BackAccrual Accounting and Income: Chapter 3 Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accrual Accounting and Income

Introduction

This chapter covers the principles and procedures of accrual accounting, the process of adjusting accounts, and the preparation of financial statements. It is essential for understanding how businesses measure and report financial performance and position in accordance with Generally Accepted Accounting Principles (GAAP).

Accrual vs. Cash-Basis Accounting

Key Differences

Accrual Accounting: Records transactions when they occur, regardless of when cash is exchanged. Required by GAAP.

Cash-Basis Accounting: Records only cash transactions (receipts and payments). Ignores non-cash transactions, resulting in incomplete financial statements. Used only by the smallest businesses.

Accrual accounting includes both cash and non-cash transactions, such as sales on account, accrual of expenses, depreciation, and usage of prepaid assets.

The Time-Period Concept

Accounting information is reported at regular intervals, typically one year (fiscal or calendar). Interim statements may be prepared for periods less than a year.

Revenue and Expense Recognition Principles

The Revenue Principle

When to recognize revenue: When goods are delivered or services performed for an amount expected to be received.

Amount to record: The cash or equivalent value to be received.

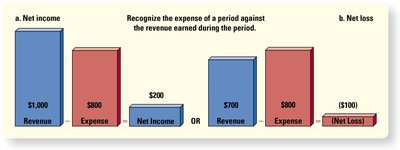

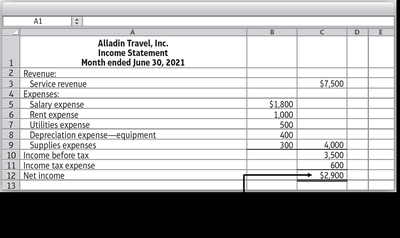

The Expense Recognition (Matching) Principle

Expenses are recognized in the same period as the related revenues.

Net income (NI) is calculated as:

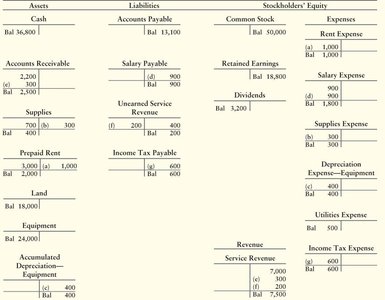

Adjusting the Accounts

Purpose of Adjusting Entries

Ensure revenues and expenses are recognized in the correct period.

Made at the end of the accounting period; affect one income statement account and one balance sheet account (no cash involved).

Categories of Adjusting Entries

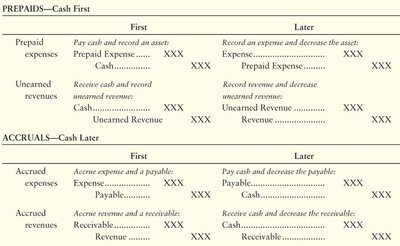

Deferrals: Cash is paid or received before the expense or revenue is recognized (e.g., prepaid expenses, unearned revenue).

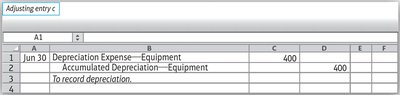

Depreciation: Allocates the cost of plant assets over their useful life.

Accruals: Expense or revenue is recognized before cash is paid or received (e.g., accrued expenses, accrued revenues).

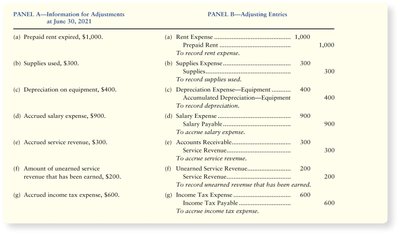

Examples of Adjusting Entries

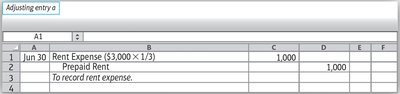

Prepaid Expenses

Prepaid rent and supplies are assets until used; then they become expenses.

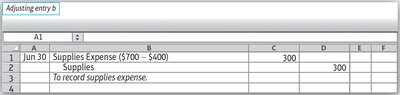

Supplies

Supplies purchased are assets; the portion used is expensed at period end.

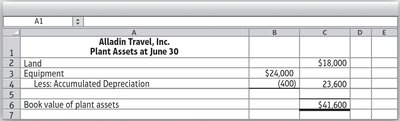

Depreciation of Plant Assets

Depreciation spreads the cost of long-lived assets over their useful life, except land.

Straight-line depreciation formula:

Monthly depreciation:

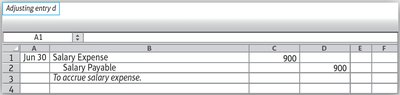

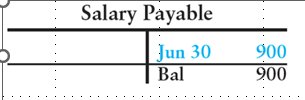

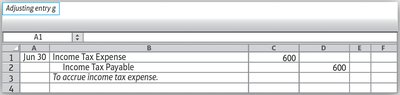

Accrued Expenses

Expenses incurred but not yet paid (e.g., salaries, taxes) are recorded as liabilities.

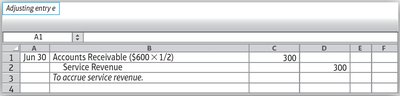

Accrued Revenues

Revenue earned but not yet collected is recorded as an asset (accounts receivable).

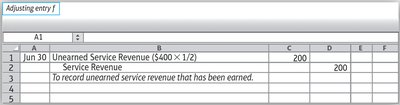

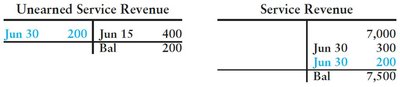

Unearned Revenue

Cash received before revenue is earned is recorded as a liability (unearned revenue).

Summary Table: Prepaid and Accrual Adjustments

This table summarizes the journal entries for prepaid expenses, unearned revenues, accrued expenses, and accrued revenues.

Summary of the Adjusting Process

Adjusting entries measure income and update the balance sheet.

Each entry affects a revenue or expense account and an asset or liability account.

No cash is involved in adjusting entries.

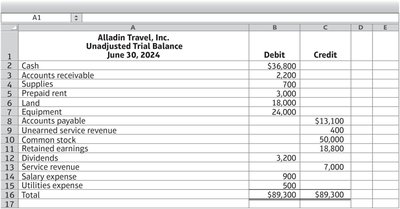

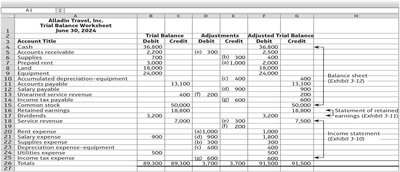

The Adjusted Trial Balance

The adjusted trial balance lists all accounts and their final balances after adjustments, ensuring total debits equal total credits.

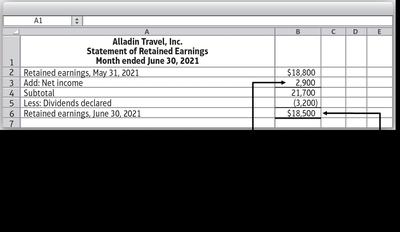

Constructing the Financial Statements

Income Statement: Reports revenues and expenses for a period.

Statement of Retained Earnings: Shows changes in retained earnings.

Balance Sheet: Reports assets, liabilities, and equity at a point in time.

Closing the Books

Purpose and Process

Prepares accounts for the next period and updates retained earnings.

Temporary accounts (revenues, expenses, dividends) are closed; permanent accounts (assets, liabilities, equity) are not.

Steps: Close revenues to retained earnings, close expenses to retained earnings, close dividends to retained earnings.

Classifying Assets and Liabilities

Current vs. Long-Term

Current Assets: Most liquid; converted to cash or used within one year (e.g., cash, receivables, supplies).

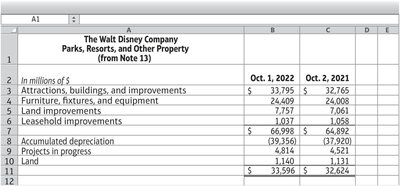

Long-Term Assets: Not expected to be converted to cash within one year (e.g., land, buildings, equipment).

Current Liabilities: Debts due within one year (e.g., accounts payable, salary payable, unearned revenue).

Long-Term Liabilities: Debts due after one year (e.g., long-term notes payable).

Formats for Financial Statements

Balance Sheet: Report format and account format.

Income Statement: Single-step (all revenues and expenses together) and multi-step (separates operating and non-operating items).

Analyzing and Evaluating Debt-Paying Ability

Key Ratios

Net Working Capital:

Current Ratio:

Debt Ratio:

Higher current ratio indicates better liquidity; lower debt ratio indicates safer financial position.

Data Visualization in Accounting

Charts and Graphs

Bar Chart: Displays categorical data for comparison.

Line Chart: Shows trends over time.

Data visualization helps accountants and managers spot patterns and trends in financial data, aiding decision-making.

Summary Table: Adjusting Entries

Category | Debit | Credit |

|---|---|---|

Prepaid expense | Expense | Asset |

Depreciation | Expense | Contra asset |

Accrued expense | Expense | Liability |

Accrued revenue | Asset | Revenue |

Unearned revenue | Liability | Revenue |

Practice Problems

Calculate current and debt ratios after various transactions (e.g., issuing stock, purchasing assets, accruing expenses).

Analyze how transactions affect liquidity and financial position.

Additional info: These notes expand on the original slides and images, providing definitions, formulas, and context for each topic. All images included are directly relevant to the explanation and reinforce the educational content.