Back

BackAccrual Accounting and Income: Chapter 3 Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accrual Accounting and Income

Accrual vs. Cash-Basis Accounting

Accrual accounting and cash-basis accounting are two fundamental methods for recording financial transactions. Understanding their differences is essential for accurate financial reporting.

Accrual Accounting: Records revenues and expenses when they are earned or incurred, regardless of when cash is exchanged.

Cash-Basis Accounting: Records revenues and expenses only when cash is received or paid.

Accrual accounting includes both cash and noncash transactions, such as sales on account, accrual of expenses, depreciation, and usage of prepaid assets.

Time-Period Concept: Ensures accounting information is reported at regular intervals, typically annually or for interim periods.

Revenue and Expense Recognition Principles

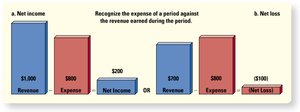

The principles of revenue and expense recognition guide when and how much revenue and expense to record, ensuring accurate measurement of net income or loss.

Revenue Principle: Revenue is recognized when goods or services are delivered, and the amount recorded is what the business expects to receive.

Expense Recognition Principle: Expenses are recognized in the same period as the related revenues, following a matching process.

Net Income: Calculated as revenue minus expenses.

Net Loss: Occurs when expenses exceed revenues.

Example: If a company earns $1,000 in revenue and incurs $800 in expenses, net income is $200. If expenses are $1,100, net loss is $100.

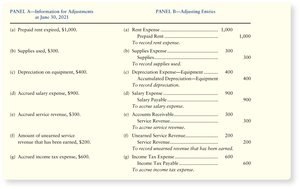

Adjusting the Accounts

Adjusting entries are necessary to ensure that all revenues and expenses are properly recorded for the period, updating both the income statement and balance sheet.

Categories of Adjusting Entries:

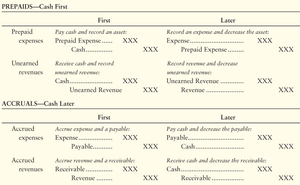

Deferrals: Payment or receipt of cash in advance (e.g., prepaid expenses, unearned revenue).

Depreciation: Allocation of plant asset cost over its useful life.

Accruals: Recognition of expenses or revenues before cash is exchanged.

Prepaid Expenses: Assets paid in advance, such as rent or supplies, which are expensed as used.

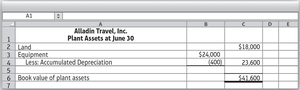

Depreciation: Spreads the cost of plant assets (except land) over their useful life using methods such as straight-line depreciation.

Accumulated Depreciation: Contra asset account showing total depreciation taken.

Accrued Expenses: Liabilities for expenses incurred but not yet paid (e.g., salaries).

Accrued Revenues: Revenues earned but not yet collected.

Unearned Service Revenue: Liability for cash received before revenue is earned.

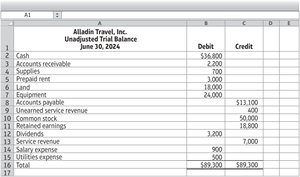

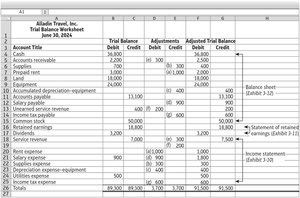

Adjusted Trial Balance

The adjusted trial balance summarizes all accounts after adjusting entries, providing the basis for preparing financial statements.

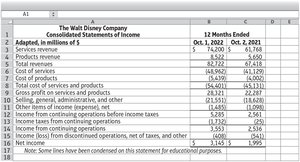

Constructing Financial Statements

Financial statements are prepared from the adjusted trial balance and include the income statement, statement of retained earnings, and balance sheet.

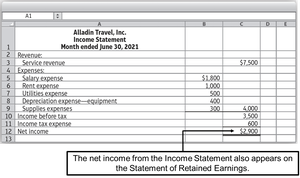

Income Statement: Lists revenues and expenses to determine net income.

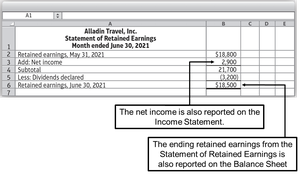

Statement of Retained Earnings: Shows changes in retained earnings, including net income and dividends.

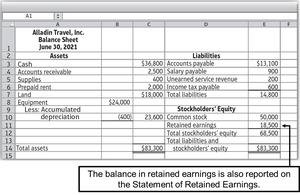

Balance Sheet: Reports assets, liabilities, and stockholders’ equity.

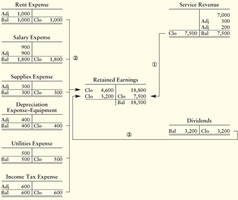

Closing the Books

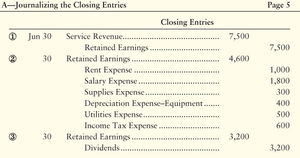

Closing entries reset temporary accounts (revenues, expenses, dividends) to zero, preparing the accounts for the next period. Permanent accounts (assets, liabilities, equity) are not closed.

Steps to Close the Books:

Close revenue accounts to Retained Earnings.

Close expense accounts to Retained Earnings.

Close dividends to Retained Earnings.

Example: Alladin Travel closes its books monthly, transferring balances to Retained Earnings.

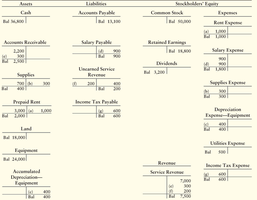

Classifying Assets and Liabilities

Assets and liabilities are classified as current or long-term based on liquidity, which measures how quickly an item can be converted to cash.

Current Assets: Most liquid, converted to cash within one year (e.g., cash, accounts receivable, prepaid expenses).

Long-Term Assets: Not converted to cash within one year (e.g., land, buildings, equipment).

Current Liabilities: Debts due within one year (e.g., accounts payable, salary payable, unearned revenue).

Long-Term Liabilities: Debts not due within one year (e.g., long-term notes payable).

Formats for Financial Statements

Financial statements can be presented in different formats, such as report or account format for the balance sheet, and single-step or multi-step format for the income statement.

Analyzing and Evaluating Debt-Paying Ability

Key ratios are used to assess a company’s liquidity and debt-paying ability.

Net Working Capital: Operating liquidity, calculated as current assets minus current liabilities.

Current Ratio: Measures liquidity; calculated as .

Debt Ratio: Measures the proportion of assets financed by debt; calculated as .

Example: A company with high current ratio and low debt ratio is considered financially stable.

Data Visualization and Chart Types

Data visualization helps in identifying patterns and trends in financial data. Two basic chart types are commonly used:

Bar Chart: Displays categorical data in a relative format.

Line Chart: Visualizes data over time, showing trends and changes.