Back

BackCapital Budgeting: Incremental Cash Flows, Depreciation, and Project Evaluation

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Capital Budgeting

Introduction to Capital Budgeting

Capital budgeting is the process by which firms evaluate and select long-term investments that are consistent with their goal of maximizing shareholder wealth. It involves analyzing the expected incremental cash flows from investment projects and deciding which projects to accept based on financial criteria such as Net Present Value (NPV) and Internal Rate of Return (IRR).

Incremental Cash Flows: The changes in a firm's future cash flows that are a direct result of taking the project.

Project Types: Replacement, expansion, and independent projects.

Key Steps: Estimate incremental earnings, adjust for non-cash items, account for capital expenditures and changes in net working capital, and discount cash flows to present value.

Types of Projects

Replacement Decisions: Assessing whether to replace an old asset with a new one.

Expansion Decisions: Evaluating the addition of new products or business lines.

Independent Projects: Projects that do not affect other operations of the firm.

Estimating Incremental Cash Flows

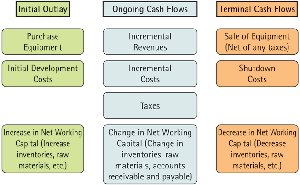

Components of Project Cash Flows

Project cash flows are typically divided into three categories: initial outlay, ongoing cash flows, and terminal cash flows. Each category includes specific items that must be considered when evaluating a project.

Initial Outlay: Purchase of equipment, initial development costs, and increases in net working capital.

Ongoing Cash Flows: Incremental revenues, incremental costs, taxes, and changes in net working capital.

Terminal Cash Flows: Sale of equipment (net of taxes), shutdown costs, and recovery of net working capital.

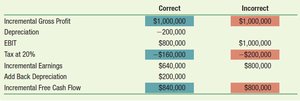

Incremental Earnings Calculation

Incremental earnings are calculated by estimating the additional revenues and subtracting the associated costs, including depreciation and taxes. The result is the unlevered net income, which is independent of the project's financing method.

Formula:

Depreciation: A non-cash expense that reduces taxable income.

Unlevered Net Income: Earnings before interest and after taxes, not affected by financing decisions.

Tax Effects and Depreciation

Depreciation reduces taxable income, creating a tax shield. The two main methods are straight-line and accelerated depreciation (e.g., MACRS). The choice of method affects the timing of tax savings but not the total amount over the asset's life.

Straight-Line Depreciation: Equal expense each year.

MACRS: Allows for greater depreciation in earlier years.

Adjusting Incremental Earnings to Free Cash Flow (FCF)

Free Cash Flow Computation

Free cash flow (FCF) represents the total incremental effect of a project on a firm's available cash. It is calculated by adjusting incremental earnings for non-cash expenses, capital expenditures, and changes in net working capital.

Formula:

Depreciation is added back because it is a non-cash expense.

Capital expenditures and changes in net working capital are subtracted as they represent actual cash outflows.

Net Working Capital (NWC)

Net working capital is the difference between current operating assets and current operating liabilities. Only operating items are included, and financing-related items are excluded.

Formula:

Examples of Current Assets: Cash, accounts receivable, inventory, prepaid expenses.

Examples of Current Liabilities: Accounts payable, unearned revenue, accrued wages.

Special Issues in Cash Flow Estimation

Opportunity Costs, Sunk Costs, and Externalities

Opportunity Costs: Include the value of foregone alternatives (e.g., lost rental income from using a facility for the project).

Sunk Costs: Exclude costs that have already been incurred and cannot be recovered (e.g., past R&D expenses).

Externalities: Include effects on other cash flows of the firm, such as cannibalization or synergies with existing products.

Project Evaluation: NPV and IRR

Net Present Value (NPV)

NPV is the sum of the present values of all cash flows associated with a project, discounted at the project's cost of capital. A positive NPV indicates that the project is expected to add value to the firm.

Formula:

Decision Rule: Accept projects with NPV > 0.

Internal Rate of Return (IRR)

IRR is the discount rate that makes the NPV of a project equal to zero. Projects are accepted if the IRR exceeds the required rate of return.

Formula:

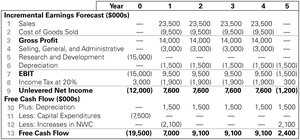

Comprehensive Example: HomeNet Project

Incremental Earnings and Free Cash Flow Forecast

The HomeNet project provides a detailed example of how to forecast incremental earnings and free cash flows over the life of a project. The forecast includes sales, costs, depreciation, taxes, and adjustments for capital expenditures and changes in net working capital.

Year 0: Large initial outlay for R&D and equipment, resulting in negative free cash flow.

Years 1-4: Positive incremental earnings and free cash flows as the project generates revenue.

Year 5: Recovery of net working capital and no salvage value for equipment.

Terminal and Continuation Value

Liquidation Value

At the end of a project's life, assets may be sold, and net working capital is recovered. The after-tax proceeds from asset sales and the recovery of working capital are included in the terminal cash flow.

Formula for After-Tax Salvage Value:

Continuation Value (Growing Perpetuity)

If a project is expected to generate cash flows indefinitely, the continuation value is calculated using the growing perpetuity formula.

Formula:

Where is the free cash flow in the first year after the forecast period, is the discount rate, and is the growth rate.

Sensitivity and Scenario Analysis

Assessing Project Risk

Sensitivity analysis examines how changes in key assumptions (e.g., discount rate, sales volume, costs) affect the project's NPV. Scenario analysis considers the impact of interrelated changes in multiple variables, such as a recession affecting both sales and costs.

Sensitivity Analysis: Varies one input at a time to see its effect on NPV.

Scenario Analysis: Evaluates the impact of simultaneous changes in several variables.

Summary

Capital budgeting is a critical process for evaluating long-term investments. It requires careful estimation of incremental cash flows, proper treatment of depreciation and taxes, and consideration of opportunity costs, sunk costs, and externalities. The use of NPV and IRR helps ensure that only value-adding projects are accepted, while sensitivity and scenario analysis provide insight into the robustness of investment decisions.