Back

BackChapter 1: Accounting in the Business Environment – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accounting: The Language of Business

Why Is Accounting Important?

Accounting is a fundamental information system that enables businesses to measure, process, and communicate financial information. This information is essential for making informed decisions and assessing business performance.

Measures business activities: Accounting tracks all financial transactions and events.

Processes information into reports: Data is organized into structured financial statements.

Communicates results to decision makers: Reports are shared with stakeholders for decision-making.

Users of accounting information: Includes external users (investors, creditors, taxing authorities) and internal users (managers, employees).

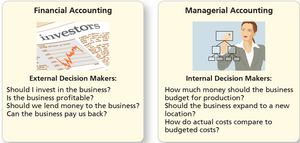

Decision Makers: Financial vs. Managerial Accounting

Accounting information serves both external and internal decision makers. Financial accounting focuses on external users, while managerial accounting is tailored for internal management.

Financial Accounting: Provides information for investors, creditors, and government agencies.

Managerial Accounting: Supports managers and employees in planning, budgeting, and controlling operations.

Types of Accountants

Accountants may specialize in various fields, each serving different roles within the business environment.

Certified Public Accountants (CPAs): Serve the general public.

Chartered Global Management Accountants (CGMAs): Advanced expertise in finance and management.

Certified Management Accountants (CMAs): Focus on internal financial management.

Certified Financial Planners (CFPs): Help individuals with personal financial planning.

Data Analytics in Accounting

Modern accountants must understand technology and data analytics, as artificial intelligence, cloud systems, and automation are transforming financial information processing.

Collaboration with IT: Accountants work with technology teams to develop robust accounting systems.

Emerging technologies: AI and automation streamline financial operations and reporting.

Organizations and Rules That Govern Accounting

Governing Organizations

Accounting standards and practices are overseen by several key organizations.

Financial Accounting Standards Board (FASB): Oversees creation and governance of accounting standards.

Securities and Exchange Commission (SEC): Regulates U.S. financial markets.

Generally Accepted Accounting Principles (GAAP)

GAAP provides guidelines for preparing financial statements, ensuring information is relevant and faithfully represented.

Relevance: Information must help users make decisions.

Faithful Representation: Information must be complete, neutral, and free from error.

International Financial Reporting Standards (IFRS)

IFRS are global accounting guidelines used in over 166 countries, published by the International Accounting Standards Board (IASB).

The Economic Entity Assumption

This principle states that each business is a separate economic unit, distinct from its owners or other entities.

Types of entities: Sole Proprietorship, Partnership, Corporation, Limited-Liability Company (LLC).

Features of a Corporation

Separate legal entity

Continuous life and transferability of ownership

No mutual agency

Limited liability for stockholders

Separation of ownership and management

Corporate taxation and government regulation

Other Key Principles

Cost Principle: Assets and services are recorded at their actual cost.

Going Concern Assumption: The entity will continue operating in the foreseeable future.

Monetary Unit Assumption: Financial statements are measured in monetary units.

Ethics in Accounting and Business

Audit: Examination of financial statements and records.

Sarbanes-Oxley Act (SOX): Requires review of internal controls.

Public Company Accounting Oversight Board (PCAOB): Monitors audits of public companies.

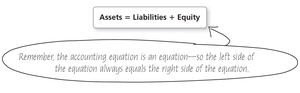

The Accounting Equation: Assets, Liabilities, and Equity

The Accounting Equation

The accounting equation is the foundation of financial accounting, representing the relationship between a company’s resources and claims to those resources.

Formula:

Definitions

Assets: Economic resources expected to benefit the business (e.g., cash, inventory, land).

Liabilities: Debts owed to creditors (e.g., accounts payable, notes payable).

Equity: Owners’ claims to assets, consisting of contributed capital and retained earnings.

Expanded Accounting Equation

Contributed Capital: Investments by owners (common stock).

Retained Earnings: Profits not distributed as dividends.

Increases in equity: Owner contributions and revenues.

Decreases in equity: Dividends and expenses.

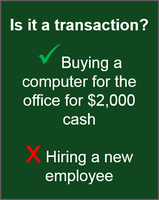

Analyzing Transactions Using the Accounting Equation

Transaction Analysis Steps

Each transaction must be analyzed to determine its effect on the accounting equation.

Identify the accounts and account type.

Decide if each account increases or decreases.

Ensure the accounting equation remains balanced.

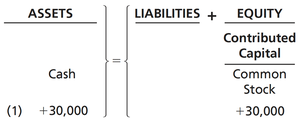

Examples of Transaction Analysis

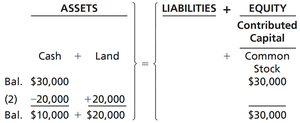

Stockholder Contribution: Owner invests cash in exchange for stock.

Purchase of Land for Cash: Asset (land) increases, asset (cash) decreases.

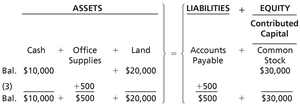

Purchase of Office Supplies on Account: Asset (supplies) increases, liability (accounts payable) increases.

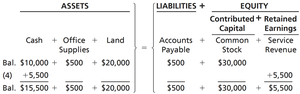

Earning Service Revenue for Cash: Asset (cash) and equity (retained earnings) increase.

Preparing Financial Statements

Types of Financial Statements

Financial statements communicate a company’s financial performance and position.

Income Statement: Reports net income or net loss for a period.

Statement of Retained Earnings: Shows changes in retained earnings.

Balance Sheet: Reports assets, liabilities, and equity at a specific date.

Statement of Cash Flows: Details cash receipts and payments.

Evaluating Business Performance: Return on Assets (ROA)

Return on Assets (ROA)

ROA is a key metric for evaluating how efficiently a company uses its assets to generate profit.

Formula:

Application: Used by investors and managers to assess profitability and asset utilization.

Example: If a company has net income of \text{ROA} = \frac{7,618}{92,647.5} \approx 8.2\%$.

Summary Table: Expanded Accounting Equation

Assets | Liabilities | Equity |

|---|---|---|

Cash, Inventory, Land | Accounts Payable, Notes Payable | Contributed Capital (Common Stock), Retained Earnings (Revenues, Expenses, Dividends) |

Additional info: Academic context and examples were added to clarify definitions and applications for exam preparation.