Back

BackChapter 1: Financial Statements

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Financial Statements: Introduction to Financial Accounting

Overview of Accounting and Its Importance

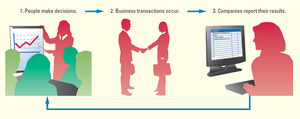

Accounting is a critical information system for businesses, enabling the measurement, processing, and communication of financial data. It supports decision-making by providing reliable financial statements and reports. The accounting cycle is the process by which these statements are prepared.

Key Point 1: Accounting measures business activities, processes data, and communicates results to decision makers.

Key Point 2: The accounting cycle ensures systematic preparation of financial statements.

Example: A company records sales transactions, processes them, and reports net income in its financial statements.

Types of Accounting and Decision Makers

Accounting serves both internal and external users. Financial accounting is for external stakeholders, while managerial accounting is for internal management.

Financial Accounting: Used by investors, creditors, government agencies, and the public.

Managerial Accounting: Used by managers for budgeting, forecasting, and projections.

Business Organization Structures

Businesses can be organized as proprietorships, partnerships, limited-liability companies (LLCs), or corporations. Each structure has distinct legal and financial implications.

Proprietorship: Single owner, personally liable for debts.

Partnership: Two or more co-owners, income/losses flow through to partners, liability varies by partnership type.

LLC: Business is liable for debts, members have limited liability, income flows through to members.

Corporation: Owned by stockholders, limited liability, double taxation, governed by board of directors.

Accounting Concepts, Assumptions, and Principles

Professional Frameworks

Accounting standards are established by GAAP (U.S.) and IFRS (international). These frameworks ensure consistency and comparability in financial reporting.

GAAP: Formulated by the Financial Accounting Standards Board (FASB).

IFRS: Formulated by the International Accounting Standards Board (IASB).

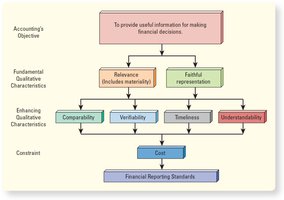

Conceptual Foundation of Accounting

The conceptual framework guides the preparation of financial statements, emphasizing relevance, faithful representation, comparability, verifiability, timeliness, and understandability, with cost as a constraint.

Entity Assumption: Each organization is a separate economic unit.

Continuity (Going-Concern) Assumption: Entity will continue operating in the foreseeable future.

Historical Cost Principle: Assets recorded at actual cost.

Stable-Monetary-Unit Assumption: Dollar’s purchasing power is assumed stable over time.

The Accounting Equation

Definition and Application

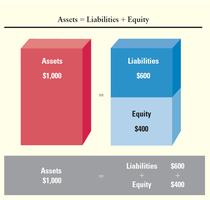

The accounting equation is fundamental to financial accounting, showing the relationship among assets, liabilities, and equity. It ensures that the two sides of the equation are always equal.

Assets: Economic resources expected to provide future benefits.

Liabilities: Debts owed to external parties.

Equity: Owners’ claims on the business.

Formula:

Components of Equity

Equity in a corporation consists of paid-in capital and retained earnings. Paid-in capital is the amount invested by stockholders, while retained earnings are accumulated profits kept in the business.

Paid-in Capital: Investments by stockholders, including common stock.

Retained Earnings: Earnings retained for business use.

Components of Retained Earnings

Retained earnings are affected by revenues, expenses, and dividends. Revenues increase retained earnings, expenses and dividends decrease them.

Revenues: Inflows from delivering goods/services.

Expenses: Outflows due to operational costs.

Dividends: Asset distributions to stockholders.

Financial Statements and Their Relationships

Income Statement

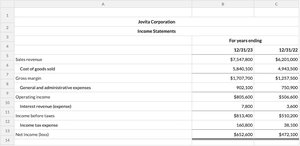

The income statement reports revenues and expenses for a period, resulting in net income or net loss. It is also known as the statement of operations.

Net Income: Revenues minus expenses.

Example: Jovita Corporation’s income statement shows sales revenue, cost of goods sold, and net income.

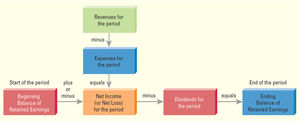

Statement of Retained Earnings

This statement shows changes in retained earnings over a period, including net income and dividends.

Beginning Retained Earnings

Add: Net income (loss)

Less: Dividends declared

Ending Retained Earnings

Balance Sheet

The balance sheet reports assets, liabilities, and stockholders’ equity at a specific point in time. It reflects the company’s financial position.

Current Assets: Used or converted to cash within one business cycle.

Long-term Assets: Benefit the company beyond the next fiscal year.

Current Liabilities: Debts due within one year.

Long-term Liabilities: Debts payable after one year.

Equity: Stockholders’ ownership of assets.

Statement of Cash Flows

This statement reports cash receipts and payments, classified into operating, investing, and financing activities.

Operating Activities: Cash flows from selling goods/services.

Investing Activities: Cash flows from buying/selling long-term assets.

Financing Activities: Cash flows from borrowing/repaying funds or equity transactions.

Ethical Decision Making in Accounting

Evaluating Business Decisions Ethically

Business and accounting decisions are influenced by economic, legal, and ethical factors. Ethical guidelines help ensure decisions are not only profitable and legal but also right.

Economic: Maximize economic benefits.

Legal: Comply with laws and regulations.

Ethical: Consider what is right beyond profitability and legality.

AICPA Code of Professional Conduct

The American Institute of Certified Public Accountants (AICPA) provides a code of conduct for accountants, emphasizing responsibilities, public interest, integrity, objectivity, independence, due care, and scope of services.

Accounting and ESG Practices

Role of Accounting in ESG

Environmental, social, and governance (ESG) reporting is increasingly important. Accountants support ESG by providing assurance and analysis for sustainability efforts.

ESG Reporting Frameworks: GRI, ISSB, UNGC, TCFD.

Measures: Energy consumed, water withdrawn, renewable energy percentage, emissions, food waste.

Accountant’s Role: Analyze carbon footprint, recommend improvements, support supplier diversity.

Accounting Careers and Certifications

Career Path Options

Accountants can pursue various career paths, including external auditor, management accountant, internal auditor, budget analyst, and financial analyst.

Certifications: CPA, CMA, CGMA, CIA, CFE.

CPA Exam: Four-section, 16-hour format covering accounting, auditing, tax, and a primary discipline.

Tools and Technologies in Accounting

Spreadsheets and Data Analytics

Spreadsheets (Excel, Google Sheets, Apple Numbers) are essential for organizing, calculating, and visualizing data. Data analytics helps discover trends and improve processes.

Artificial Intelligence: Machines solve problems creatively; machine learning enables learning from data.

Robotic Process Automation: Software bots automate routine tasks, freeing accountants for analysis.

Technology Risks: Proper use facilitates decisions; improper use can lead to errors.

Additional info: These notes expand on brief points from the original materials, providing definitions, examples, and academic context for clarity and completeness.