Back

BackChapter 11: Shareholders’ Equity – Structure, Transactions, and Analysis

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Shareholders’ Equity & Its Significance

Measuring Ownership Interest

Shareholders’ equity represents the owners’ claim on the assets of a corporation after all liabilities have been paid. It is a key indicator of the value that belongs to shareholders collectively.

Definition: Shareholders’ equity is the residual interest in the assets of the entity after deducting liabilities.

Example: If shareholders’ equity is $1,000,000, that amount belongs to shareholders collectively.

Equity Financing

Equity financing involves raising capital by issuing shares rather than borrowing funds.

Advantages:

No repayment required (unlike loans).

Dividends are optional, not mandatory like interest payments.

Disadvantages:

Ownership dilution – issuing more shares reduces existing shareholders’ ownership percentage.

Dividends are not tax-deductible, making debt financing cheaper for tax purposes.

Shareholders’ Equity Overview

The Accounting Equation

The accounting equation forms the foundation of financial accounting:

Equation:

Residual Interest: Shareholders’ equity is what remains after creditors are paid.

Example: If assets are $1,000,000 and liabilities are $700,000, equity is $300,000.

Dividends

Dividends are distributions of profits to shareholders, decided by the board of directors. They are not guaranteed and are only paid if the company has sufficient retained earnings and cash.

Equity Terminology

Shareholders’ Equity: Used by corporations.

Owner’s Equity: Used by sole proprietorships.

Components of Shareholders’ Equity ("CCRA")

C – Share Capital: Money invested by shareholders when shares are issued.

C – Contributed Surplus: Created from certain transactions with shareholders (e.g., share repurchases, stock options).

R – Retained Earnings: Profits kept in the business instead of being paid as dividends.

A – Accumulated Other Comprehensive Income (AOCI): Includes gains and losses from certain items (e.g., investments, foreign currency adjustments, hedging instruments). Only in IFRS, not ASPE.

Comprehensive Income

Definition and Formula

Comprehensive income includes all changes in equity during a period except those resulting from investments by owners and distributions to owners.

Formula:

Example: Net Income = $1,500,000; OCI = $400,000; Total Comprehensive Income = $1,900,000.

Accumulated Other Comprehensive Income (AOCI): Includes gains/losses on certain investments, foreign currency translation adjustments, and hedging instruments. Reported after net income and only under IFRS.

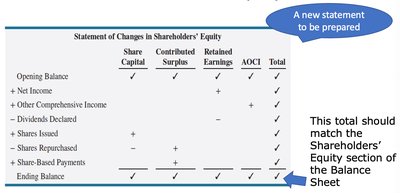

Statement of Changes in Shareholders’ Equity

Purpose and Structure

This statement explains how each component of equity changed during the year. The total must match the equity section of the balance sheet.

Shows changes in share capital, contributed surplus, retained earnings, and AOCI.

Includes net income, OCI, dividends, shares issued/repurchased, and share-based payments.

Share Terminology and Types

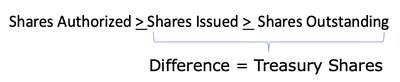

Authorized, Issued, Outstanding, and Treasury Shares

Authorized Shares: Maximum number a company can issue.

Issued Shares: Shares actually sold by the company.

Outstanding Shares: Shares currently held by investors (includes employees, officers, public investors).

Treasury Shares: Shares repurchased by the company but not cancelled; not considered outstanding and receive no dividends or voting rights.

Par Value

Par value is an older concept where each share had a minimum value. Most Canadian jurisdictions no longer allow par value shares.

Types of Shares

Common Shares: Basic ownership, residual claim, voting rights, no guaranteed dividend.

Preferred Shares: Priority rights (dividends, assets on dissolution), usually no voting rights, may be cumulative, convertible, redeemable, retractable, or participating.

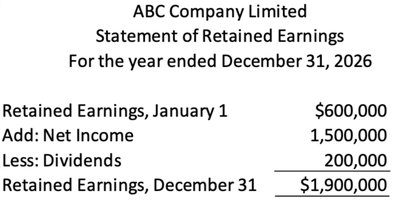

Retained Earnings

Definition and Formula

Retained earnings are profits reinvested in the corporation minus dividends declared over the company’s life.

Formula:

Events Affecting Retained Earnings:

Net income/loss

Dividends

Correction of errors

Accounting policy changes

Share retirement (if repurchased above average price)

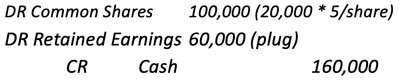

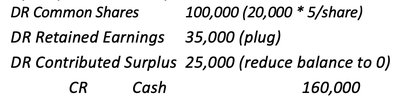

Repurchases of Shares and Contributed Surplus

Share Repurchase Accounting

When a company buys back its own shares, the accounting depends on whether the repurchase price is above or below the average issue price.

Above Average Price: Extra cost reduces contributed surplus first, then retained earnings (contributed surplus cannot go below zero).

Below Average Price: Difference increases contributed surplus.

Dividends

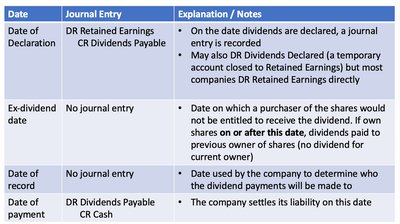

Dividend Process and Journal Entries

Dividends are declared by the board and paid only on outstanding shares. The company must have sufficient retained earnings and cash.

Date of Declaration: Record liability (Dividends Payable).

Ex-dividend Date: No entry; determines who receives dividend.

Date of Record: No entry; company determines eligible shareholders.

Date of Payment: Settle liability (pay cash).

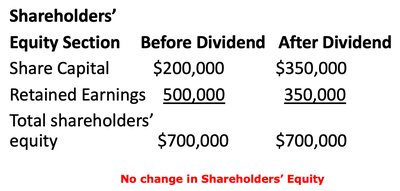

Stock Dividends

Stock dividends distribute additional shares to shareholders instead of cash, maintaining ownership percentage but increasing the number of shares outstanding.

Recording: Stock dividends are recorded at market value on the declaration date.

Effect: Increases share capital, decreases retained earnings, no change in total equity.

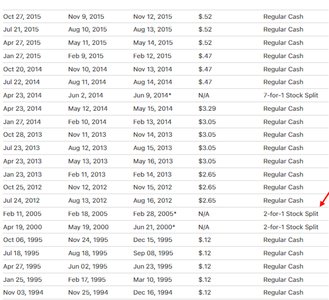

Stock Splits

Definition and Accounting

A stock split increases the number of shares outstanding and decreases the market price per share, making shares more affordable. No journal entry is required; only a memo disclosure is made.

Example: 2-for-1 split: Each share becomes two shares; price per share halves.

Reverse Split: Reduces number of shares, increases price per share.

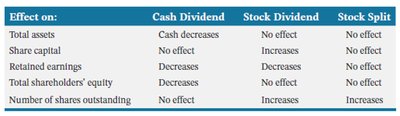

Comparison of Dividends and Stock Splits

The effects of cash dividends, stock dividends, and stock splits differ in their impact on equity accounts and total assets.

Effect on: | Cash Dividend | Stock Dividend | Stock Split |

|---|---|---|---|

Total assets | Cash decreases | No effect | No effect |

Share capital | No effect | Increases | No effect |

Retained earnings | Decreases | Decreases | No effect |

Total shareholders’ equity | Decreases | No effect | No effect |

Number of shares outstanding | No effect | Increases | Increases |

Employee Stock Options

Explanation and Accounting

Stock options give employees the right to buy shares at a fixed price, often as part of compensation. The vesting period is the time employees must wait before exercising options.

Accounting: The total option value is expensed over the vesting period.

Example: $80,000 total value, 4-year vesting = $20,000 expense per year.

Financial Statement Analysis

Key Ratios

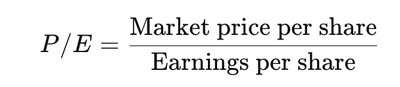

Price-to-Earnings (P/E) Ratio: Indicates how much investors are willing to pay per dollar of earnings.

Dividend Payout Ratio: Shows the percentage of earnings paid as dividends.

Dividend Yield: Measures the return from dividends relative to share price.

Return on Shareholders’ Equity (ROE): Indicates how efficiently a company generates profit from shareholders’ investment.