Back

BackChapter 5: Receivables and Revenue – Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Receivables and Revenue

Learning Objectives

Apply GAAP for proper revenue recognition

Account for sales returns and allowances

Account for sales discounts

Account for accounts receivable

Evaluate collectability using the allowance for uncollectible accounts

Account for notes receivable and interest revenue

Evaluate liquidity using three new ratios

Analyze receivables collectibility using an aging schedule created with an Excel pivot table

Revenue Recognition under GAAP

Principles of Revenue Recognition

Revenue is recognized when it is earned, which occurs when goods are delivered or services are performed. The amount recorded is either the cash received or the fair market value of assets received in exchange. According to GAAP, companies are entitled to receive amounts from customers for delivering goods or performing services.

Key Point: Revenue is recognized when control of goods or services is transferred to the customer.

Key Point: For most product sales, control transfers when products are shipped; for services, control transfers over time as services are delivered.

Example: Apple Inc. recognizes revenue when products are shipped (FOB shipping point) or as services are delivered.

Five-Step Revenue Recognition Model

Identify the contract(s)

Identify the performance obligation(s)

Determine the transaction price

Allocate the transaction price to the performance obligations

Recognize revenue when the entity satisfies the obligations

Key Point: Multiple performance obligations require allocation of revenue based on stand-alone selling prices (SSPs).

Example: Apple allocates revenue to hardware, bundled services, and future software upgrades.

Shipping Terms and Revenue Recognition

FOB Shipping Point: Ownership and revenue recognition occur when goods leave the shipping dock.

FOB Destination: Ownership and revenue recognition occur when goods are delivered to the customer.

Sales Returns and Allowances

Accounting for Returns and Allowances

Customers may return unsatisfactory or damaged goods. Companies with significant return experience estimate returns and record them as a contra revenue account, reducing reported sales revenue.

Key Point: Sales Returns & Allowances is a contra revenue account with a debit balance.

Example: If Apple expects 1% of sales to be returned, it records estimated returns in the same period as sales to comply with the matching principle.

Price Protection Allowances

Companies may grant allowances for price reductions after a sale. These must be estimated and reserved for in the period of the price change, not when refund requests are received.

Key Point: Estimating allowances ensures proper matching of revenue and related expenses.

Sales Discounts

Accounting for Sales Discounts

Sales discounts are incentives for early payment, such as 2/10, n/30 (2% discount if paid within 10 days, net due in 30 days). Discounts are recorded in a contra revenue account.

Key Point: Net revenue is calculated as Sales minus Sales Returns & Allowances minus Sales Discounts.

Example: If a customer pays $2,000 invoice within the discount period, the cash received is $1,960 ($2,000 x 98%).

Accounts Receivable

Types of Receivables

Receivables are monetary claims against others and are classified as current assets. They arise from selling goods/services (accounts receivable) or lending money (notes receivable).

Key Point: Subsidiary ledgers track individual customer balances.

Managing Receivables

Run credit checks

Extend credit only to creditworthy customers

Separate cash handling and record-keeping

Monitor payment habits

Send reminders and statements

Allowance for Uncollectible Accounts

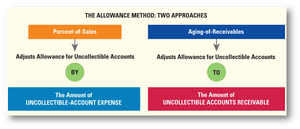

Allowance Method

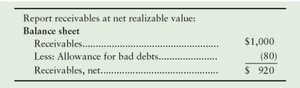

The allowance method estimates uncollectible accounts based on past experience. The Allowance for Uncollectible Accounts is a contra account to Accounts Receivable, reducing the asset to its net realizable value (NRV).

Formula:

Key Point: The allowance is a reserve for estimated uncollectible amounts.

Example: Apple Inc. reports accounts receivable net of allowance on its balance sheet.

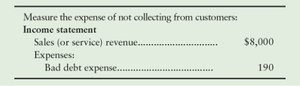

Reporting Receivables and Bad Debt Expense

Receivables: Reported at net realizable value on the balance sheet.

Bad Debt Expense: Reported on the income statement as an expense.

Estimating Uncollectibles

Percent-of-Sales Method: Uncollectible-account expense is computed as a percent of revenue (income statement approach).

Aging-of-Receivables Method: Specific accounts are analyzed based on how long they have been outstanding (balance sheet approach).

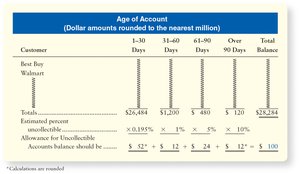

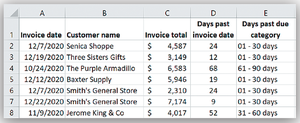

Aging Schedule Example

The aging schedule analyzes receivables by age to estimate the allowance for uncollectibles. Older receivables have a higher probability of being uncollectible.

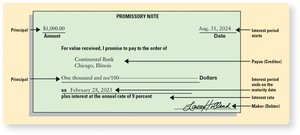

Notes Receivable and Interest Revenue

Key Terms

Creditor: Party to whom money is owed (lender)

Debtor: Party who owes money (borrower)

Interest: Cost of borrowing money, stated as an annual percentage rate

Maturity Date: Date when the note must be paid

Maturity Value: Principal plus interest

Principal: Amount borrowed

Term: Length of time from signing to payment

Interest Calculation Formula

Formula:

Liquidity Ratios

Quick (Acid-Test) Ratio

The quick ratio measures a company's ability to pay current liabilities with its most liquid assets. A ratio of 1:1 is considered a benchmark.

Formula:

Example: Apple's quick ratio is 0.4967, below the benchmark but not alarming due to its cash-generating ability.

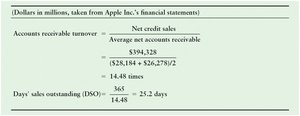

Accounts Receivable Turnover and Days' Sales Outstanding (DSO)

Accounts Receivable Turnover: Number of times per year a company collects its average accounts receivable. Formula:

Days' Sales Outstanding (DSO): Average number of days to collect receivables. Formula:

Example: Apple collected its average customer account in 25.2 days.

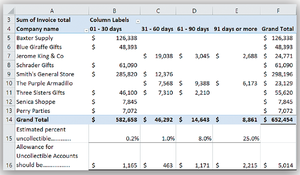

Analyzing Receivables Collectibility with Aging Schedules and Pivot Tables

Using Excel Pivot Tables

A pivot table summarizes receivables data, allowing analysis of collectibility by age and customer. This helps estimate the allowance for uncollectibles more precisely.

Key Point: Aging schedules and pivot tables help companies focus on overdue accounts and estimate uncollectible amounts.

Summary Table: Methods for Estimating Uncollectible Accounts

Method | Basis | Approach | Key Formula |

|---|---|---|---|

Percent-of-Sales | Revenue | Income Statement | |

Aging-of-Receivables | Receivable Age | Balance Sheet | Sum of (Receivable Amount × Estimated % by Age) |

Practice Formulas

Net Revenue:

Net Realizable Value:

Interest Revenue:

Quick Ratio:

Accounts Receivable Turnover:

DSO:

Conclusion

This chapter provides a comprehensive overview of accounting for receivables and revenue, including proper recognition, management of returns, discounts, and allowances, estimation of uncollectibles, and analysis of liquidity and collectibility using ratios and aging schedules. Mastery of these concepts is essential for accurate financial reporting and effective credit management.