Back

BackChapter 8: Inventories – Additional Valuation Issues (Intermediate Accounting)

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Inventories: Additional Valuation Issues

Lower-of-Cost-or-Net Realizable Value (LCNRV)

The LCNRV rule is applied when the future utility of inventory drops below its original cost, requiring companies to abandon the historical cost principle. This rule is used with the average cost and FIFO inventory methods.

Net Realizable Value (NRV): The estimated selling price in the ordinary course of business, less reasonably predictable costs of completion, disposal, and transportation.

Application: Inventory is usually priced on an item-by-item basis.

Example: If inventory cost is $950, sales value is $1,000, cost of completion is $50, and selling costs are $200, then NRV = $1,000 - $50 - $200 = $750. Inventory is reported at $750, and a loss of $200 ($950 - $750) is recognized.

Journal Entry Methods:

Cost-of-Goods-Sold Method: Adjusts inventory directly through cost of goods sold.

Loss Method: Recognizes a separate loss due to decline in inventory value.

Lower-of-Cost-or-Market (LCM)

The LCM rule is an exception granted by FASB for companies using LIFO or retail inventory methods. Instead of comparing cost to NRV, companies compare cost to a designated market value, which is constrained by two limits:

Ceiling: Net realizable value (NRV)

Floor: NRV less a normal profit margin

Example: If estimated selling price is $1,000, cost of completion/disposal is $300, and normal profit margin is 10% ($100), then:

NRV = $1,000 - $300 = $700

NRV less normal profit margin = $700 - $100 = $600

Inventory is valued at the lower of cost or designated market value, which must fall between the floor and ceiling.

Comparison: LCNRV vs LCM

LCNRV: Cost is compared only to NRV.

LCM: Cost is compared to market value, constrained by NRV (ceiling) and NRV less normal profit (floor).

LIFO Exception: LIFO inventory is often below NRV and replacement cost, but if LIFO value exceeds NRV, adjustments are made to ensure inventory is not overstated.

Purchase Commitments

Purchase commitments are agreements to buy inventory in advance. The seller retains title until delivery, and the buyer recognizes no asset or liability unless the contract price exceeds market price and losses are expected. Losses are recognized in the period when market price declines occur, unless the agreement is cancellable.

Example: If Starbucks signs a non-cancellable contract to buy coffee beans at $10,000,000, but market price drops to $7,000,000, a loss is recognized for the difference.

Gross Profit Method of Estimating Inventory

The Gross Profit Method is used for interim estimates or when physical counts are impractical. It is not GAAP for continuous use. The method estimates gross profit using historical rates and calculates cost of goods sold and ending inventory.

Steps:

Determine cost of goods available for sale: Beginning Inventory + Purchases

Estimate gross profit rate (GP%)

Calculate cost of goods sold: Sales × (1 - GP%)

Determine ending inventory: Cost of goods available for sale - Cost of goods sold

Formulas:

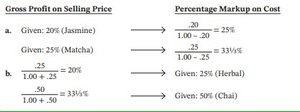

Gross Profit Percentage and Markup Calculations

Gross profit can be expressed as a percentage of selling price or as a percentage markup on cost. The conversion between these is important for inventory estimation.

Gross Profit on Selling Price: Given as a percentage of sales revenue.

Percentage Markup on Cost: Calculated as markup divided by cost.

Conversion Formula:

To convert between the two:

Example: 20% gross profit on selling price is equivalent to 25% markup on cost.

Retail Inventory Method (RIM)

The Retail Inventory Method estimates ending inventory using a cost-to-retail percentage. It requires continual records of cost and retail values and is used for interim reporting and inventory estimation.

Steps:

Compute cost and retail value of goods available for sale.

Subtract sales (at retail) from retail goods available for sale to get ending inventory at retail.

Calculate cost-to-retail percentage:

Estimate ending inventory at cost:

Types of Cost Pools:

FIFO: Uses new purchases during the period.

LIFO: Uses inventory at the start of the year.

Average: Combines beginning inventory and purchases.

Markups and Markdowns: Markup cancellations, markdowns, and markdown cancellations affect the retail value and must be considered in the calculation.

Example: If beginning inventory cost is $14,000 (retail $20,000), purchases cost $63,000 (retail $90,000), and sales are $85,000, the method estimates ending inventory at cost using the cost-to-retail percentage.

Summary of Learning Objectives

Describe and apply the lower-of-cost-or-net-realizable value rule.

Describe and apply the lower-of-cost-or-market rule.

Compute ending inventory and cost of goods sold using the gross profit method and retail inventory method (FIFO, LIFO, average cost pools).