Back

BackCompleting the Accounting Cycle: Structured Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Completing the Accounting Cycle

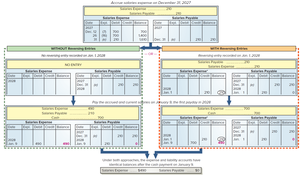

Preparing a Work Sheet and Its Usefulness

The work sheet is a tool used by accountants to organize and summarize accounting data for a period, facilitating the preparation of adjusting entries and financial statements. Although not a required report, it is highly beneficial for reducing errors and linking accounts to financial statements.

Definition: A work sheet is a multi-column document that helps accountants prepare adjusting entries, financial statements, and closing entries.

Benefits:

Reduces risk of errors by organizing information.

Links accounts and adjustments to financial statements.

Shows effects of proposed transactions.

Helps in preparing financial statements efficiently.

Steps in Preparing a Work Sheet:

Enter unadjusted trial balance.

Enter adjustments.

Prepare adjusted trial balance.

Sort adjusted trial balance amounts to financial statements.

Total statement columns, compute income or loss, and balance columns.

Example: See the annotated work sheet below for a visual breakdown of the process.

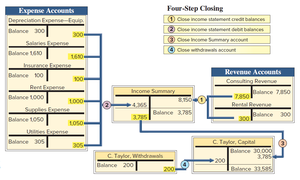

Closing Entries and Post-Closing Trial Balance

Closing entries are made at the end of the accounting period to reset temporary account balances to zero and update the owner’s capital account. The post-closing trial balance lists only permanent accounts, ensuring that debits and credits are equal and temporary accounts are cleared.

Temporary Accounts: Revenues, expenses, withdrawals, and income summary. These are closed at period end.

Permanent Accounts: Assets, liabilities, and owner’s capital. These remain open.

Closing Process:

Close credit balances in revenue accounts to Income Summary.

Close debit balances in expense accounts to Income Summary.

Close Income Summary to Owner’s Capital.

Close Withdrawals to Owner’s Capital.

Example: The diagram below illustrates the four-step closing process.

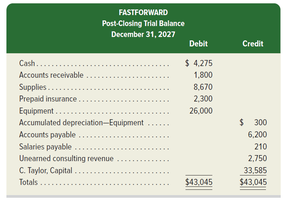

Post-Closing Trial Balance: Shows only permanent accounts with their balances after closing entries. All temporary accounts have zero balances.

Example: The table below shows a sample post-closing trial balance.

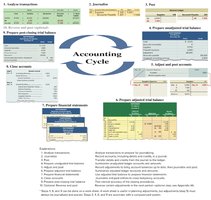

The Accounting Cycle

The accounting cycle is a series of steps performed during each accounting period to record, process, and report financial information. It ensures that all transactions are properly documented and financial statements are accurately prepared.

Steps in the Accounting Cycle:

Analyze transactions

Journalize

Post

Prepare unadjusted trial balance

Adjust and post accounts

Prepare adjusted trial balance

Prepare financial statements

Close accounts

Prepare post-closing trial balance

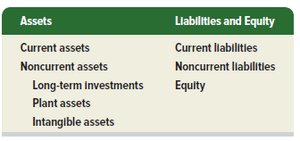

Classified Balance Sheet

Structure and Components

A classified balance sheet organizes assets and liabilities into current and noncurrent categories, providing a clearer picture of a company’s financial position. This classification helps users assess liquidity and long-term stability.

Current Items: Expected to be collected or owed within one year or the operating cycle.

Noncurrent Items: Expected to be held or owed for more than one year or the operating cycle.

Categories:

Assets: Current assets, long-term investments, plant assets, intangible assets

Liabilities: Current liabilities, long-term liabilities

Equity: Owner’s claim on assets

Example: The table below summarizes the main categories.

Assets | Liabilities and Equity |

|---|---|

Current assets | Current liabilities |

Noncurrent assets | Noncurrent liabilities |

Long-term investments | Equity |

Plant assets | |

Intangible assets |

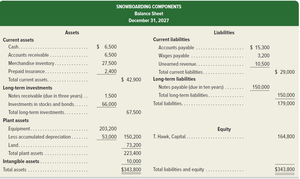

Classified Balance Sheet Example: The following balance sheet shows the arrangement of assets, liabilities, and equity.

Current Assets

Current assets are resources expected to be sold, collected, or used within one year or the operating cycle. Examples include cash, short-term investments, accounts receivable, inventory, and prepaid expenses.

Examples: Cash, accounts receivable, merchandise inventory, prepaid insurance.

Long-Term Investments

Long-term investments are assets held for more than one year or the operating cycle. Examples include notes receivable and investments in stocks and bonds.

Examples: Notes receivable, stocks and bonds held long-term.

Plant Assets

Plant assets are tangible, long-lived assets used in operations, also known as property, plant, and equipment (PP&E). Examples include equipment, machinery, buildings, and land.

Examples: Equipment, buildings, land.

Intangible Assets

Intangible assets are long-term assets that benefit business operations but lack physical form. Examples include patents, trademarks, copyrights, franchises, and goodwill.

Examples: Patents, trademarks, goodwill.

Current Liabilities

Current liabilities are obligations due within one year or the operating cycle. Examples include accounts payable, wages payable, taxes payable, interest payable, and unearned revenues.

Examples: Accounts payable, wages payable, unearned revenues.

Long-Term Liabilities

Long-term liabilities are obligations not due within one year or the operating cycle. Examples include notes payable, mortgages payable, bonds payable, and lease obligations.

Examples: Notes payable, bonds payable, mortgages payable.

Equity

Equity represents the owner’s claim on the assets. For a proprietorship, it is reported in the owner’s capital account and is not separated into current and noncurrent categories.

Example: Owner’s capital account.

Current Ratio: Computation and Analysis

Definition and Formula

The current ratio is a liquidity measure that helps assess a company’s ability to pay its short-term debts. It is calculated as the ratio of current assets to current liabilities.

Formula:

Interpretation: A higher current ratio indicates better liquidity and a greater ability to meet short-term obligations.

Example: The table below compares current ratios for Visa and Mastercard over three years.

Reversing Entries: Purpose and Application

Definition and Use

Reversing entries are optional journal entries made at the beginning of a new accounting period to reverse certain adjusting entries from the previous period. They simplify recordkeeping for accrued revenues and expenses.

Purpose: To simplify the recording of subsequent transactions related to accrued items.

Application: Typically used for accrued salaries, interest, and other similar items.

Example: The diagram below shows the accounting for payroll accrual with and without reversing entries.