Back

BackComprehensive Study Notes for IGCSE Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Accounting

Definition and Purpose

Accounting is an information system that involves recording, classifying, summarizing, reporting, analyzing, and interpreting the financial condition and performance of a business. The main objective is to communicate financial information to stakeholders for decision-making purposes.

Bookkeeping: The process of recording daily transactions in chronological order, forming part of the accounting system.

Stakeholders: Individuals or groups interested in the financial performance of the business, such as owners, managers, creditors, and investors.

Transaction Analysis

Assets and Liabilities

Assets are items of value owned by a company, while liabilities are creditors’ claims on assets, reflecting obligations to provide assets, products, or services to others.

Current Liabilities: Amounts payable within 12 months (e.g., bank overdraft, trade payables).

Non-Current Liabilities: Amounts payable after 12 months (e.g., loans).

Types of Transactions

Carriage Inwards: Shipping costs incurred when receiving goods (included in cost of purchases).

Carriage Outwards: Shipping costs incurred when sending goods to customers (recorded as an expense).

Accrual Accounting Concepts

Accruals and Prepayments

Accrual accounting recognizes income and expenses when they are earned or incurred, not when cash is received or paid.

Accrued Expense: Expenses incurred but not yet paid (current liability).

Prepaid Income: Revenues received in advance (current liability).

Prepayment: Amount paid in advance for a service not yet received.

Matching Principle

Costs incurred in an accounting period should be matched against the revenue of that period to accurately measure profit.

Merchandising Operations

Service vs. Trading Business

Service Business: Provides services, does not hold inventory (e.g., travel agency).

Trading Business: Buys and resells goods, holds inventory for resale.

Inventory

Inventory Valuation

Inventory should be valued at the lower of cost and net realizable value, applying the prudence principle to avoid overstating assets and profits.

Cost: Purchase price plus additional costs to bring inventory to its present condition.

Net Realizable Value: Estimated selling price less costs to complete and sell the goods.

Internal Controls and Reporting Cash

Bank Reconciliation Statement

A bank reconciliation statement explains differences between the cash book and bank statement balances, ensuring accuracy and detecting errors or fraud.

Adjustments include uncredited cheques, direct debits, bank charges, and errors.

Receivables and Investments

Trade Receivables and Payables

Trade Receivables: Amounts owed by customers for goods sold on credit.

Trade Payables: Amounts owed to suppliers for goods purchased on credit.

Bad Debts and Provision for Doubtful Debts

Bad Debts: Amounts that cannot be collected from trade receivables (expense).

Provision for Doubtful Debts: Estimate of receivables unlikely to be collected (applies prudence and matching principles).

Long-Lived Assets

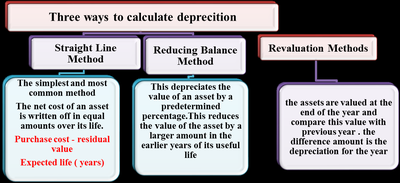

Depreciation

Depreciation is the allocation of the cost of a non-current asset over its useful life, reflecting wear and tear, obsolescence, or depletion.

Straight Line Method: Equal depreciation each year.

Reducing Balance Method: Depreciation is a fixed percentage of the asset’s book value each year.

Revaluation Method: Asset is valued at year-end; depreciation is the difference between opening and closing values.

Current Liabilities

Examples and Management

Bank overdraft, trade payables, accrued expenses.

Effective management ensures liquidity and operational continuity.

Time Value of Money

Concept

The time value of money recognizes that a sum of money has greater value now than in the future due to its earning potential. This concept is fundamental in discounting future cash flows and valuing investments.

Long Term Liabilities

Examples

Loans, debentures, mortgages payable after more than one year.

Stockholders' Equity

Share Capital

Authorized Share Capital: Maximum share capital a company can issue.

Issued Share Capital: Amount actually issued to shareholders.

Called-up Capital: Amount requested from shareholders.

Paid-up Capital: Amount actually received from shareholders.

Types of Shares

Preference Shares: Fixed dividend, priority over ordinary shares, usually no voting rights.

Ordinary Shares: Variable dividend, voting rights, residual claim on assets.

Statement of Cash Flows

Purpose

The statement of cash flows summarizes cash inflows and outflows from operating, investing, and financing activities, providing insight into a company’s liquidity and financial flexibility.

Financial Statement Analysis

Key Ratios

Current Ratio:

Quick Ratio (Acid Test):

Gross Profit Margin:

Net Profit Margin:

Return on Capital Employed (ROCE):

Applications

Assessing profitability, liquidity, and efficiency.

Comparing performance across periods and with other firms.

GAAP vs IFRS

Overview

Generally Accepted Accounting Principles (GAAP) and International Financial Reporting Standards (IFRS) are two major frameworks for preparing financial statements. Key differences include treatment of inventory, revenue recognition, and presentation of financial statements.

Additional Key Concepts

Double Entry System

Every transaction affects two accounts, ensuring the accounting equation remains balanced. This system reduces errors and facilitates the preparation of accurate financial statements.

Books of Original Entry

Purchases Journal: Records credit purchases of goods.

Sales Journal: Records credit sales of goods.

Cash Book: Records all cash and bank transactions.

General Journal: Records transactions not captured in other books (e.g., error corrections, depreciation).

Correction of Errors

Errors in accounting records can be classified as errors of omission, commission, principle, original entry, compensating errors, reversal of entries, or entries done twice. Only errors affecting the trial balance require a suspense account for correction.

Depreciation Methods Table

Method | Description | Formula/Key Point |

|---|---|---|

Straight Line | Equal depreciation each year | |

Reducing Balance | Depreciation is a fixed percentage of book value each year | Higher depreciation in early years |

Revaluation | Depreciation is the difference between opening and closing values | Used for assets like tools, small equipment |

Profit and Loss

The income statement (profit and loss account) shows the net profit or loss for a period, calculated as:

Gross Profit:

Net Profit:

Accounting Cycle

The accounting cycle is the process of recording and processing all financial transactions of a company, from when the transaction occurs to its representation in the financial statements and closing of accounts.

Steps include: Transaction analysis, journal entries, posting to ledger, trial balance, adjustments, financial statements, closing entries.

Financial Documents

Invoice: Document sent to buyer showing details of goods sold on credit.

Debit Note: Sent to supplier for unsatisfactory goods or overcharges.

Credit Note: Issued by supplier to reduce amount owed by customer.

Statement of Account: Summary of transactions with a customer over a period.

Control Accounts

Control accounts summarize transactions in the sales and purchases ledgers, providing a check on the accuracy of individual accounts and facilitating error detection.

Clubs and Societies

Receipts and Payments Account: Summary of all cash and bank transactions.

Income and Expenditure Account: Similar to profit and loss account, includes only revenue items and adjustments for accruals and prepayments.

Accumulated Fund: Equivalent to capital in trading organizations.

Ratio Analysis

Ratio analysis is used for inter-firm and intra-firm comparisons, measuring profitability, liquidity, and efficiency. Limitations include differences in accounting policies, business size, and external factors.

Limited Companies

Limited Liability: Shareholders’ liability is limited to the amount unpaid on their shares.

Debentures: Long-term loans with fixed interest, ranked above shares in liquidation.

Dividends: Distribution of profits to shareholders, may be interim or final.

Statement of Changes in Equity: Summarizes changes in share capital, retained earnings, and reserves.

Additional info: These notes are structured to cover the core topics of a financial accounting course, with expanded explanations, examples, and formulas for exam preparation.