Back

BackFundamental Accounting Principles and Inventory Valuation: A Blueprint for Financial Reporting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Designing the Financial Blueprint

This section introduces the foundational rules, principles, and standards that underpin the structure of financial accounting. These guidelines ensure that businesses maintain reliable and comparable financial records, forming the backbone of trustworthy financial reporting.

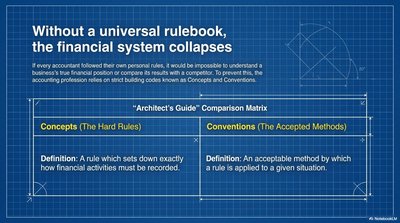

Accounting Concepts and Conventions

Concepts vs. Conventions

Accounting relies on a universal set of rules and accepted methods to ensure consistency and comparability across organizations. These are divided into Concepts (hard rules) and Conventions (accepted methods).

Concepts (The Hard Rules) | Conventions (The Accepted Methods) |

|---|---|

A rule which sets down exactly how financial activities must be recorded. | An acceptable method by which a rule is applied to a given situation. |

Key Accounting Principles

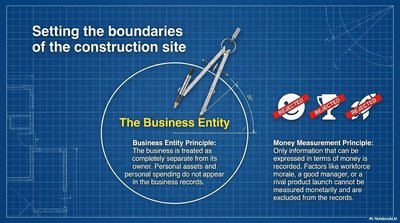

Business Entity Principle

The business is treated as a separate entity from its owner. Personal assets and spending do not appear in the business records.

Money Measurement Principle

Only information that can be expressed in monetary terms is recorded. Non-monetary factors, such as workforce morale or managerial skill, are excluded from the records.

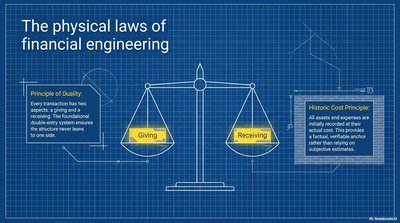

Principle of Duality (Double Entry)

Every transaction has two aspects: a giving and a receiving. This duality ensures the accounting equation remains balanced.

Accounting Equation:

Historic Cost Principle

All assets and expenses are initially recorded at their actual cost, providing a factual and verifiable anchor for financial statements.

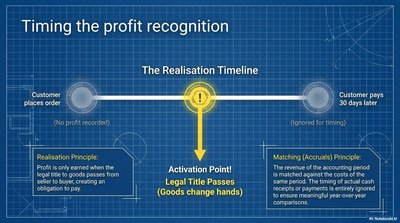

Realisation Principle

Profit is recognized only when the legal title to goods passes from seller to buyer, creating an obligation to pay. This is known as the activation point.

Matching (Accruals) Principle

Revenues are matched against the costs incurred to generate them within the same accounting period, ensuring meaningful year-over-year comparisons.

Going Concern Principle

The business is assumed to continue operating indefinitely. Non-current assets are valued at book value, not at liquidation prices.

Materiality Principle

Items of very low value are not recorded as separate assets. If the cost of tracking an asset exceeds its benefit, it is treated as an expense.

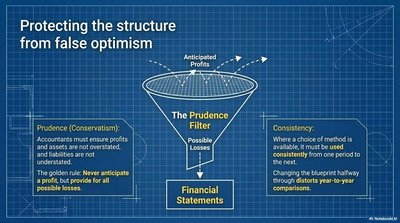

Prudence (Conservatism) Principle

Accountants must ensure profits and assets are not overstated, and liabilities are not understated. The golden rule: Never anticipate a profit, but provide for all possible losses.

Consistency Principle

Once a method is chosen, it must be used consistently from one period to the next. Changing methods distorts year-to-year comparisons.

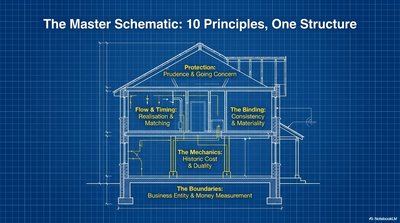

The Master Schematic: 10 Principles, One Structure

These ten principles work together to form a robust structure for financial reporting, ensuring protection, reliability, and comparability.

International Accounting Standards (IAS)

Financial statements must adhere to International Accounting Standards, ensuring global consistency and reliability.

Ensure statements use the same rules and guidelines internationally.

Protect users of financial statements.

Prevent misleading information due to inconsistent accounting.

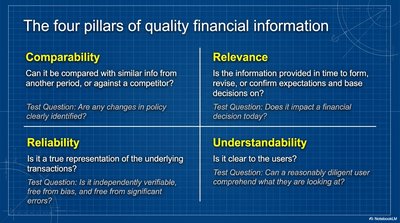

Qualities of Financial Information

High-quality financial information must possess four key attributes:

Comparability | Relevance | Reliability | Understandability |

|---|---|---|---|

Can it be compared with similar info from another period or competitor? | Is the information timely and useful for decisions? | Is it a true, verifiable representation of transactions? | Is it clear to users? |

Inventory Valuation: Application of Principles

Valuing Inventory

At the end of each financial year, inventory is valued at the lower of cost or net realisable value (NRV). This applies the Prudence principle, ensuring assets and profits are not overstated.

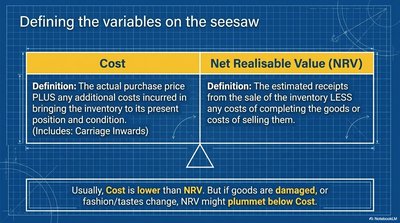

Cost vs. Net Realisable Value (NRV)

Cost | Net Realisable Value (NRV) |

|---|---|

The actual purchase price plus any additional costs incurred to bring the inventory to its present position and condition (includes carriage inwards). | The estimated receipts from the sale of inventory less any costs of completing or selling them. |

Usually, cost is lower than NRV. If goods are damaged or become obsolete, NRV may fall below cost.

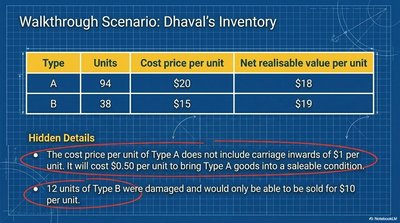

Inventory Valuation Example: Dhaval's Inventory

The following table summarizes the inventory details for two types of goods, including cost price, carriage inwards, preparation costs, and NRV. Additional details include damaged goods and their adjusted NRV.

Type | Units | Cost price per unit | Net realisable value per unit |

|---|---|---|---|

A | 94 | $20 | $18 |

B | 38 | $15 | $19 |

The cost price per unit of Type A does not include carriage inwards of $1 per unit. It will cost $0.50 per unit to bring Type A goods into a saleable condition.

12 units of Type B were damaged and would only be able to be sold for $10 per unit.

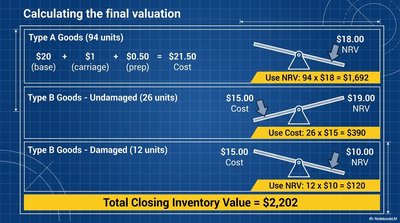

Calculating the Final Inventory Valuation

Type A Goods (94 units): Cost per unit =

Type B Goods – Undamaged (26 units): Cost per unit =

Type B Goods – Damaged (12 units): Cost per unit =

Total Closing Inventory Value = $2,202

Conclusion: Building Trust in Financial Reporting

By applying core accounting concepts such as Duality and Prudence, and adhering to International Accounting Standards, businesses ensure that their financial statements are reliable and trustworthy. Good accounting is about faithfully representing the financial position, not about presenting the most optimistic scenario.