Back

BackFundamentals of Managerial Accounting: Cost Classification and Flow

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Fundamentals of Managerial Accounting

Financial Accounting vs. Managerial Accounting

Accounting information is used by both external and internal stakeholders, but the purposes and methods differ significantly between financial accounting and managerial accounting.

Financial Accounting: Focuses on preparing financial statements for external users (investors, creditors, regulators) in accordance with GAAP. Reports are mandatory, historical, highly summarized, and prepared quarterly or annually.

Managerial Accounting: Provides detailed information for internal users (managers) to aid in planning and controlling operations. Reports are not mandatory, can be historical, current, or future-oriented, and are prepared as needed. They include job costing, budgets, and contribution margin statements.

Aspect | Financial Accounting | Managerial Accounting |

|---|---|---|

Audience | External | Internal |

Reports | Financial Statements | Job Costing, Budgets |

Rules | GAAP | No specific rules |

Frequency | Quarterly/Annually | As needed |

Detail | Summarized | Detailed |

Product Costs vs. Period Costs

Costs are classified as product costs or period costs depending on their relationship to inventory and the timing of their expense recognition.

Product Costs: Costs incurred to acquire or produce inventory. Recorded as assets on the balance sheet and expensed as Cost of Goods Sold when inventory is sold. Includes raw materials, direct labor, and manufacturing overhead.

Period Costs: Costs not directly traceable to inventory. Expensed immediately in the period incurred as Selling, General, and Administrative (SG&A) expenses. Examples: office rent, CEO salaries, insurance, depreciation on office equipment.

Balance Sheet: Product costs increase inventory assets. Income Statement: Product costs become expenses when sold; period costs are expensed when incurred.

Inventory Cost Flow for Merchandisers

Merchandisers purchase inventory and sell it without modification. The flow of inventory costs is tracked from purchase to sale:

Beginning Inventory + Purchases = Goods Available to Sell

Goods Available to Sell - Ending Inventory = Cost of Goods Sold

Direct vs. Indirect Costs

Costs assigned to a cost object (product, service, department) are classified as direct or indirect.

Direct Costs: Easily traced to a cost object. Includes Direct Materials (raw materials) and Direct Labor (hands-on labor tracked by timecards).

Indirect Costs (Overhead): Not easily traced; benefit multiple cost objects. Includes indirect materials (supplies, glue), indirect labor (maintenance, supervisors), and other overhead (depreciation, utilities).

Allocated Overhead and Predetermined Overhead Rate

Overhead costs are allocated to cost objects using a predetermined overhead rate (PDOH) to enable timely pricing and cost estimation.

PDOH Rate Formula:

Allocated Overhead Formula:

Example: If estimated overhead is $400,000 and estimated direct labor hours are 10,000, then PDOH Rate = $40 per direct labor hour.

Total Cost Calculation for Cost Objects

To estimate the total cost of a product, service, or other cost object, sum all relevant costs:

Example (Service Firm): Direct materials = $1,000; Direct labor = $15/hour × 6 hours = $90; Allocated overhead = $40/hour × 6 hours = $240; Total cost = $1,330.

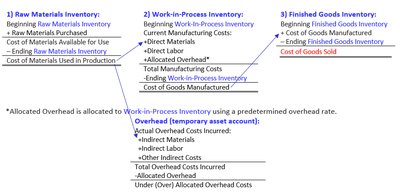

Cost Flow in Manufacturing Companies

Manufacturers track product costs through three inventory accounts: Raw Materials, Work-in-Process, and Finished Goods. Costs flow as follows:

Raw materials purchased increase Raw Materials Inventory.

Materials used decrease Raw Materials Inventory and increase Work-in-Process Inventory (direct materials only).

Direct labor and allocated overhead increase Work-in-Process Inventory.

Completed products decrease Work-in-Process and increase Finished Goods Inventory.

Sold products decrease Finished Goods Inventory and are expensed as Cost of Goods Sold.

Job-Order Costing vs. Process Costing

Manufacturers use different costing systems based on their production methods:

Job-Order Costing: Used for unique or custom products/services. Costs are accumulated by job or batch. Examples: construction, hospitals, law firms.

Process Costing: Used for mass-produced identical items. Costs are accumulated by process or department. Examples: food production, paint manufacturing, oil refining.

Summary Table: Inventory Cost Flow in Manufacturing

Inventory Account | Increase | Decrease |

|---|---|---|

Raw Materials | Purchases | Materials Used in Production |

Work-in-Process | Direct Materials, Direct Labor, Allocated Overhead | Cost of Goods Manufactured |

Finished Goods | Cost of Goods Manufactured | Cost of Goods Sold |

Additional info: The image included visually reinforces the explanation of inventory cost flow in manufacturing, showing the movement of costs through Raw Materials, Work-in-Process, and Finished Goods Inventory, and the allocation of overhead using a predetermined rate.