Back

BackIntroduction to Accounting and the Business Environment

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Accounting: The Language of Business

Definition and Purpose

Accounting is an information system that measures, processes, and communicates financial information about business activities. It is often referred to as the "language of business" because it provides essential data for decision-making by various stakeholders.

Measures business financial activities

Processes information into structured reports

Communicates these reports to decision makers

Includes bookkeeping as a foundational element, but extends to analysis and interpretation

Users of Accounting Information

Accounting information is used by a wide range of decision makers, both internal and external to the organization. Each user group has distinct information needs.

Internal users: Managers, business owners, employees

External users: Investors, creditors, government agencies, regulatory bodies, not-for-profit organizations, and individuals

Types of Accounting

There are two primary branches of accounting, each serving different user groups:

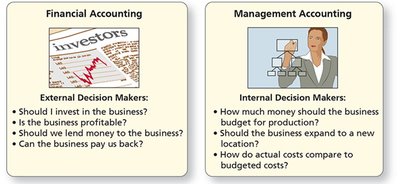

Financial Accounting: Provides information for external decision makers (e.g., investors, creditors). Focuses on historical data and compliance with standards.

Management Accounting: Provides information for internal decision makers (e.g., managers). Focuses on planning, controlling, and decision-making within the organization.

Forms of Business Organizations

Overview and Comparison

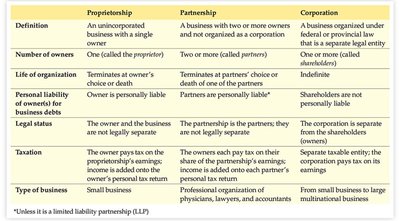

Businesses can be organized in several forms, each with unique characteristics regarding ownership, liability, taxation, and legal status.

Proprietorship | Partnership | Corporation | |

|---|---|---|---|

Definition | Unincorporated, single owner | Two or more owners, not a corporation | Organized under law as a separate legal entity |

Number of Owners | One (proprietor) | Two or more (partners) | One or more (shareholders) |

Life of Organization | Ends at owner's choice or death | Ends at partners' choice or death | Indefinite |

Personal Liability | Owner is personally liable | Partners are personally liable* | Shareholders are not personally liable |

Legal Status | Not legally separate | Not legally separate | Legally separate |

Taxation | Owner pays tax on business income | Each partner pays tax on share of income | Corporation pays tax on its income |

Type of Business | Small businesses | Professional organizations | Small to large businesses |

Additional info: In a Limited Liability Partnership (LLP), one partner's actions do not create significant liability for other partners.

Accounting Standards: GAAP vs IFRS

Purpose and Overview

Accounting standards ensure the usefulness, reliability, and comparability of financial information. The two main frameworks are:

GAAP (Generally Accepted Accounting Principles): Country-specific guidelines for measuring, processing, and communicating financial information.

IFRS (International Financial Reporting Standards): Developed by the International Accounting Standards Board (IASB) for global consistency.

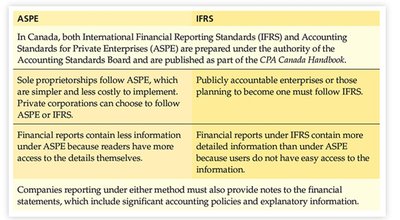

Canadian Context: IFRS and ASPE

In Canada, the Accounting Standards Board (AcSB) administers standards:

IFRS: Required for publicly accountable enterprises

ASPE (Accounting Standards for Private Enterprises): Used by small to medium-sized businesses; a simplified version of IFRS

Both are principles-based, requiring professional judgment

Framework for Financial Reporting

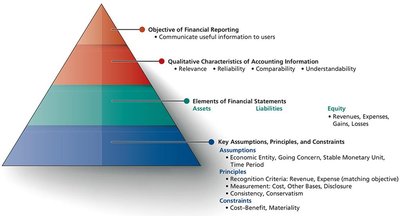

Hierarchy of the Conceptual Framework

The conceptual framework for financial reporting is structured in levels, each building on the previous to ensure the quality and consistency of financial statements.

Level 1: Objective – Communicate useful information to users

Level 2: Qualitative Characteristics – Relevance, reliability, comparability, understandability

Level 3: Elements – Assets, liabilities, equity, revenues, expenses, gains, losses

Level 4: Key Assumptions, Principles, and Constraints – Economic entity, going concern, stable monetary unit, cost principle, cost-benefit constraint

Qualitative Characteristics

Relevance: Information must be capable of making a difference in decisions

Reliability: Information must be accurate and free from bias

Comparability: Enables users to identify similarities and differences between periods or entities

Understandability: Information must be clear and concise

Key Elements of Financial Statements

Assets: Economic resources controlled by the entity, expected to provide future benefits

Liabilities: Debts or obligations owed to outsiders (creditors)

Equity: Residual interest in the assets after deducting liabilities

Revenues, Expenses, Gains, Losses: Components that affect equity

Key Assumptions, Principles, and Constraints

Economic Entity Assumption: Separate records for each entity

Going Concern Assumption: Business will continue operating

Stable Monetary Unit Assumption: Ignore inflation effects

Cost Principle: Assets recorded at historical cost

Cost-Benefit Constraint: Benefits of information should exceed the cost of providing it

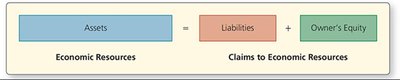

The Accounting Equation

Basic Equation

The accounting equation is the foundation of the double-entry accounting system. It shows the relationship between assets, liabilities, and owner's equity:

Formula:

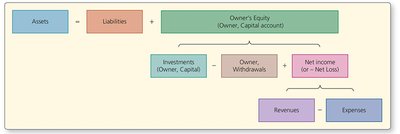

Expanded Accounting Equation

The equation can be expanded to show the components of owner's equity:

Examples of Assets, Liabilities, and Owner's Equity

Assets: Cash, accounts receivable, notes receivable, prepaid expenses, land, buildings, equipment

Liabilities: Accounts payable, accrued liabilities, notes payable, unearned revenue

Owner's Equity: Capital (investments), withdrawals, revenues, expenses

Accounting for Business Transactions

Steps in Transaction Analysis

Each business transaction affects the accounting equation. The steps for analyzing transactions are:

Identify the accounts and account types impacted

Determine if each account increases or decreases

Ensure the accounting equation remains balanced after each transaction

Example: Owner invests cash, business purchases land, earns revenue, incurs expenses, etc.

Financial Statements

Types and Order of Preparation

Financial statements are formal reports that summarize an entity's financial activities. They are prepared in a specific order:

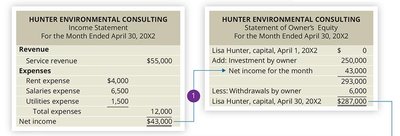

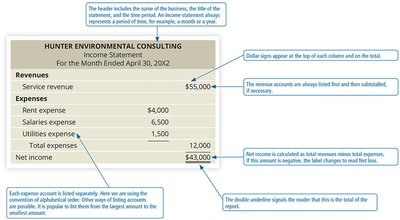

Income Statement: Summarizes revenues and expenses for a period, showing net income or loss

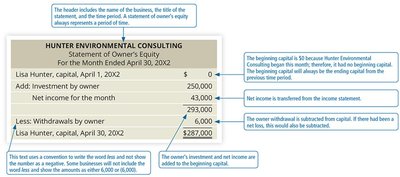

Statement of Owner's Equity: Shows changes in owner's equity during the period

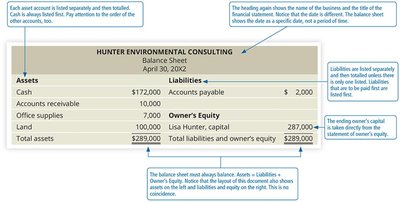

Balance Sheet: Lists assets, liabilities, and owner's equity at a specific date

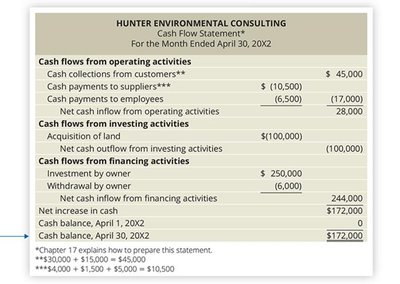

Cash Flow Statement: Reports cash inflows and outflows during the period

Relationships Among Financial Statements

The financial statements are interrelated:

Net income from the income statement is added to owner's equity in the statement of owner's equity

The ending capital balance from the statement of owner's equity appears in the balance sheet

The ending cash balance from the cash flow statement must match the cash reported on the balance sheet