Back

BackIntroduction to Financial Accounting and the Balance Sheet Equation

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Financial Information and Bookkeeping

Public Perception vs. Reality of Accountants

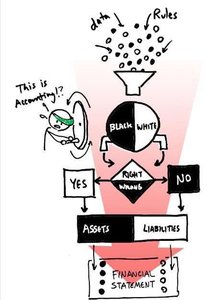

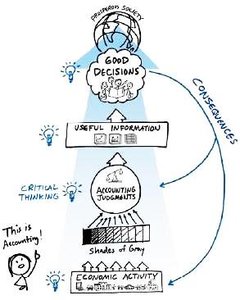

Accounting is often misunderstood by the public as a purely mechanical process, where every transaction is either right or wrong, black or white. In reality, accounting involves significant judgment and interpretation, requiring critical thinking to transform economic activity into useful information for decision-making.

Public Perception: Accounting is seen as a rigid, rule-based process.

Reality: Accountants must apply judgment to economic activities, resulting in information that supports good decisions and has real consequences.

Financial Information: Users and Purposes

External Users

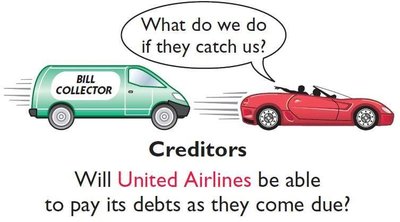

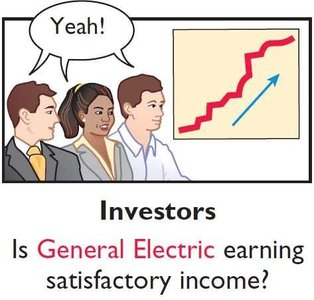

External users rely on financial information to make decisions about a company. These include creditors, investors, and regulators.

Creditors: Assess a company's ability to pay its debts as they come due.

Investors: Evaluate company size, profitability, and income to make investment decisions.

Regulators: Ensure compliance with financial reporting standards.

Internal Users

Internal users include managers and employees who use financial information for operational and strategic decisions.

Finance: Determines if cash is sufficient to pay dividends to stockholders.

Marketing: Sets product prices to maximize net income.

Human Resources: Decides on employee pay raises based on financial capacity.

Management: Evaluates profitability of product lines and makes decisions about eliminating or expanding them.

Definition of Accounting

What is Accounting?

Accounting is a system for recording information about business transactions to provide summary statements of a company's financial position and performance to users who require such information.

Three sets of books: Financial Accounting, Tax Accounting, Managerial Accounting

Financial reporting requirements vary by country and standard-setting authority

Financial Reporting Requirements

National and International Standards

Financial reporting is governed by standards such as French GAAP (PCG), International Financial Reporting Standards (IFRS), and US GAAP. Companies must file periodic financial statements, including annual, semi-annual, and ad-hoc reports.

French GAAP: Standardized chart of accounts, periodic filings

IFRS: Required for firms traded in public markets in over 150 countries

US GAAP: Required for US firms

These requirements create tension in accounting, such as determining when sales and expenses occur.

Required Financial Statements

Types of Financial Statements

Financial statements provide a comprehensive overview of a company's financial position and performance.

Balance Sheet: Lists resources (assets) and obligations (liabilities) on a specific date.

Income Statement: Shows results of operations over a period using accrual accounting.

Statement of Cash Flows: Details sources and uses of cash over a period.

Statement of Stockholders’ Equity: Explains changes in stockholders’ equity over time.

Notes: Provide additional information about operations and financial position.

Balance Sheet Equation

Fundamental Equation and Its Components

The balance sheet equation is the foundation of double-entry bookkeeping and financial reporting. It ensures that assets are always equal to the sum of liabilities and stockholders’ equity.

Equation:

Provides the framework for recording and summarizing economic events

Changes between two balance sheets are summarized in other financial statements

In liquidation, creditors' claims (liabilities) are settled before ownership claims (stockholders’ equity)

Assets

Assets are resources expected to provide future economic benefits, such as generating cash inflows or reducing cash outflows. Assets are recognized when acquired in a past transaction and their value can be measured with reasonable precision.

Examples: Cash, Supplies, Equipment

Liabilities

Liabilities are claims on assets by creditors, representing obligations to make future payments of cash, goods, or services. Liabilities are recognized when the obligation is based on benefits or services received and the payment is reasonably certain.

Examples: Accounts Payable, Notes Payable, Salaries and Wages Payable

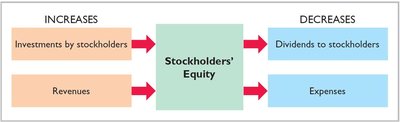

Stockholders’ Equity

Stockholders’ Equity is the residual claim on assets after settling liabilities. It is also referred to as net worth, net assets, or net book value. Stockholders’ equity arises from contributed capital and retained earnings.

Contributed Capital: Common stock, additional paid-in capital, treasury stock

Retained Earnings: Accumulation of net income (revenues minus expenses), less dividends

Dividends

Dividends are distributions of retained earnings to shareholders. They are not expenses and are recorded as a reduction of retained earnings on the declaration date, creating a liability until payment.

Summary Table: Balance Sheet Equation Components

Component | Definition | Examples |

|---|---|---|

Assets | Resources expected to provide future economic benefits | Cash, Supplies, Equipment |

Liabilities | Obligations to make future payments to creditors | Accounts Payable, Notes Payable |

Stockholders' Equity | Residual claim on assets after liabilities | Common Stock, Retained Earnings |