Back

BackInventory and Cost of Goods Sold: Concepts, Methods, and Applications

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Inventory and Cost of Goods Sold

Introduction

This chapter explores the accounting for inventory and cost of goods sold (COGS), focusing on the classification, measurement, and reporting of inventory, as well as the impact of different inventory costing methods on financial statements. The content is essential for understanding how merchandising companies manage and report inventory, and how these practices affect profitability and decision-making.

Accounting for Inventory

Definition and Classification

Inventory refers to goods purchased for resale, distinct from supplies or equipment used internally.

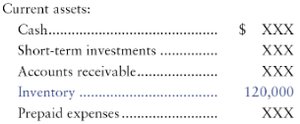

Inventory is classified as an asset on the balance sheet because it provides future economic benefit through eventual sale.

Service vs. Merchandising Companies

Merchandising companies differ from service companies by maintaining inventory and recording cost of goods sold (COGS) on the income statement.

Service companies do not report inventory or COGS.

Merchandisers track inventory as an asset and COGS as an expense.

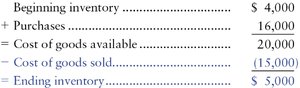

Inventory Flow and Financial Statement Impact

Inventory on hand is reported as an asset; inventory sold is reported as COGS (expense).

The basic inventory equation is:

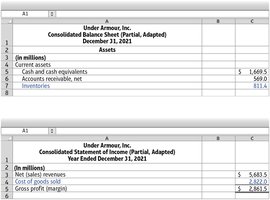

Sales Price vs. Cost of Inventory

Sales revenue is based on the sale price of inventory sold.

COGS is based on the cost of inventory sold.

Gross profit (or gross margin) is the excess of sales revenue over COGS.

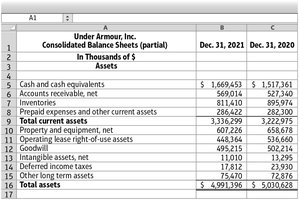

Determining Inventory Quantities

Physical count at year-end confirms inventory quantities.

Consigned goods: Inventory on consignment is included in the seller's records, not the retailer's.

Goods in transit: Ownership depends on shipping terms (FOB Shipping Point vs. FOB Destination).

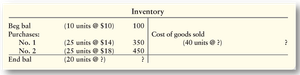

Inventory Costing Systems

Perpetual System: Continuously updates inventory records for each purchase and sale.

Periodic System: Updates inventory records at the end of the period based on physical count.

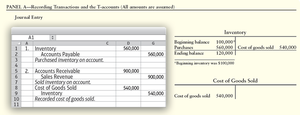

Recording Inventory Transactions (Perpetual System)

Purchases: Debit Inventory; Credit Cash/Accounts Payable.

Sales: Debit Cash/Accounts Receivable; Credit Sales Revenue. Also, Debit COGS; Credit Inventory.

Inventory Cost Components

Includes purchase price, freight-in, insurance, taxes, less returns, allowances, and discounts.

Inventory Costing Methods

Overview

The choice of inventory costing method affects reported profits, taxes, and financial ratios.

Common methods: Specific Identification, Average-Cost, FIFO, LIFO.

Specific Identification Method

Used for unique, high-value items (e.g., cars, antiques).

Assigns actual cost to each item sold and remaining in inventory.

Average-Cost (Weighted-Average) Method

Calculates average cost per unit for all inventory available during the period.

COGS and ending inventory are valued at this average cost.

FIFO (First-In, First-Out) Method

Assumes earliest goods purchased are the first to be sold.

COGS reflects older costs; ending inventory reflects recent costs.

LIFO (Last-In, First-Out) Method

Assumes latest goods purchased are the first to be sold.

COGS reflects recent costs; ending inventory reflects older costs.

Not permitted under IFRS.

Comparing Methods

When prices rise: LIFO yields lower taxable income and taxes; FIFO yields higher ending inventory values.

When prices fall: Effects are reversed.

U.S. GAAP and Inventory

Disclosure and Consistency

Companies must disclose inventory methods and apply them consistently.

Lower-of-Cost-or-Market (LCM) Rule

Inventory is reported at the lower of historical cost or market value (net realizable value).

If market value drops below cost, inventory is written down to market value.

International Perspective

IFRS does not allow LIFO; both IFRS and GAAP use net realizable value for market value, but GAAP uses replacement cost for LIFO inventories.

Under IFRS, some inventory write-downs can be reversed; under GAAP, they cannot.

ESG Factors and Inventory Valuation

Environmental, social, and governance (ESG) trends can affect inventory value (e.g., declining demand for non-sustainable products).

Inventory Analysis and Ratios

Gross Profit Percentage

Measures profitability of inventory sales.

Formula:

Gross Profit = Sales – COGS

Inventory Turnover and Days Inventory Outstanding (DIO)

Inventory Turnover:

DIO:

Indicate how efficiently inventory is managed.

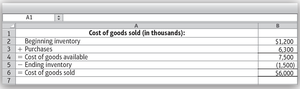

Cost-of-Goods-Sold (COGS) Model

COGS Equation

COGS is calculated as:

Used in both perpetual and periodic systems.

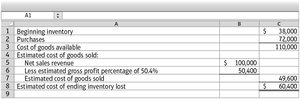

Budgeting and Estimation

Managers can rearrange the COGS model to estimate required purchases or ending inventory.

Excel Tools for Inventory Analysis

Using XLOOKUP in Excel

Inventory records often use identifiers such as SKU, UPC, or serial numbers.

The XLOOKUP function in Excel helps match transaction data with inventory details for analysis.

Summary Table: Key Inventory Equations

Equation | Description |

|---|---|

Basic inventory flow | |

COGS calculation | |

Gross profit calculation | |

Gross profit percentage | |

Inventory turnover ratio | |

Days inventory outstanding |

Conclusion

Understanding inventory accounting is crucial for accurate financial reporting, effective management, and strategic decision-making in merchandising businesses. The choice of inventory costing method, adherence to GAAP, and analysis of key ratios all play significant roles in evaluating company performance and financial health.